{"title":"Startups’ demand for accounting expertise: evidence from a randomized field experiment","authors":"Ofir Gefen, David Reeb, Johan Sulaeman","doi":"10.1007/s11142-023-09775-8","DOIUrl":null,"url":null,"abstract":"Abstract We conduct a randomized field experiment (RFE) to assess whether startup firms perceive accounting expertise as an important investor credential. We send 13,358 unsolicited and unique emails to active startup firms across the US, showing an interest in them with a proposition to meet a bogus investor. The experiment has high response rates, with 4,535 (33.94%) opened emails and 828 (6.19%) website visits, reflecting investors’ proliferating practice of outbound origination to contact new startups. Our RFE compares startup reactions to fictitious investors with certified public accountant (CPA) designations versus two control groups: investors without credentials and those with other professional licenses. Startup firms are 48% likelier to read unsolicited emails from CPA-bearing investors and 47% likelier to visit their websites, relative to investors with a medical license. We document an analogous preference for CPA-bearing investors even when we separately analyze startups in medical-related industries. This gap persists when investors pose as angels, venture capitalists (VCs), or without professional licenses. The relatively low percentage (2.5%) of email bounces and spam reports makes it unlikely that spam algorithms drive the findings. Further tests reveal that the response rates differ by firm age, which is inconsistent with spam filter explanations but congruent with startup firms’ demand for accounting expertise. Finally, we undertake a follow-up experiment with 3,443 new startups to distinguish between accounting and general business expertise using a master’s in business administration (MBA). Startups are 13.8% likelier to read emails from a CPA-bearing investor than from an MBA-credentialed investor and 22.6% more likely to visit the CPA-bearing investor’s website.","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"176 1","pages":"0"},"PeriodicalIF":5.8000,"publicationDate":"2023-06-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11142-023-09775-8","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

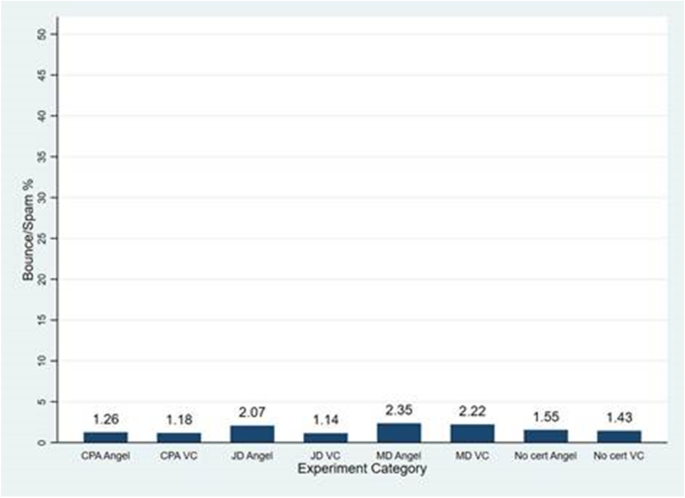

Abstract We conduct a randomized field experiment (RFE) to assess whether startup firms perceive accounting expertise as an important investor credential. We send 13,358 unsolicited and unique emails to active startup firms across the US, showing an interest in them with a proposition to meet a bogus investor. The experiment has high response rates, with 4,535 (33.94%) opened emails and 828 (6.19%) website visits, reflecting investors’ proliferating practice of outbound origination to contact new startups. Our RFE compares startup reactions to fictitious investors with certified public accountant (CPA) designations versus two control groups: investors without credentials and those with other professional licenses. Startup firms are 48% likelier to read unsolicited emails from CPA-bearing investors and 47% likelier to visit their websites, relative to investors with a medical license. We document an analogous preference for CPA-bearing investors even when we separately analyze startups in medical-related industries. This gap persists when investors pose as angels, venture capitalists (VCs), or without professional licenses. The relatively low percentage (2.5%) of email bounces and spam reports makes it unlikely that spam algorithms drive the findings. Further tests reveal that the response rates differ by firm age, which is inconsistent with spam filter explanations but congruent with startup firms’ demand for accounting expertise. Finally, we undertake a follow-up experiment with 3,443 new startups to distinguish between accounting and general business expertise using a master’s in business administration (MBA). Startups are 13.8% likelier to read emails from a CPA-bearing investor than from an MBA-credentialed investor and 22.6% more likely to visit the CPA-bearing investor’s website.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们