{"title":"(A)Synchronous Housing Markets of Global Cities","authors":"Vipul Bhatt, N. Kundan Kishor","doi":"10.1007/s11146-022-09903-2","DOIUrl":null,"url":null,"abstract":"<p>In this paper we examine house price synchronization in 15 global cities using real house price data from 1995:Q1-2020:Q2. We find that although there is evidence for bilateral positive phase synchronization, there is no evidence for an integrated global housing market for our sample of cities. Using a hierarchical clustering approach, we identify three clusters of cities with similar housing price cycles that are not solely determined by geographic proximity. We interpret this finding as suggestive of a rather segmented housing market for the global cities in our sample. Using a dynamic factor model with time-varying stochastic volatility, we decompose a city’s real housing price growth into a global component, a cluster-based component, and an idiosyncratic component. For most cities in our sample, the global component plays a minor role, whereas the cluster-based factor explains a large fraction of the observed variation in real house price growth, with its contribution peaking during the Great Recession of 2007-09.</p>","PeriodicalId":22891,"journal":{"name":"The Journal of Real Estate Finance and Economics","volume":"56 18","pages":""},"PeriodicalIF":0.0000,"publicationDate":"2022-04-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"The Journal of Real Estate Finance and Economics","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11146-022-09903-2","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

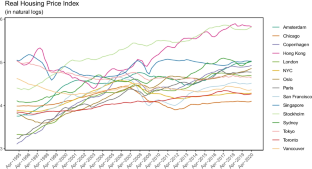

Abstract

In this paper we examine house price synchronization in 15 global cities using real house price data from 1995:Q1-2020:Q2. We find that although there is evidence for bilateral positive phase synchronization, there is no evidence for an integrated global housing market for our sample of cities. Using a hierarchical clustering approach, we identify three clusters of cities with similar housing price cycles that are not solely determined by geographic proximity. We interpret this finding as suggestive of a rather segmented housing market for the global cities in our sample. Using a dynamic factor model with time-varying stochastic volatility, we decompose a city’s real housing price growth into a global component, a cluster-based component, and an idiosyncratic component. For most cities in our sample, the global component plays a minor role, whereas the cluster-based factor explains a large fraction of the observed variation in real house price growth, with its contribution peaking during the Great Recession of 2007-09.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们