{"title":"Economic effects of litigation risk on corporate disclosure and innovation","authors":"Stefan F. Schantl, Alfred Wagenhofer","doi":"10.1007/s11142-023-09778-5","DOIUrl":null,"url":null,"abstract":"<p>Empirical studies on the relationship between shareholder litigation and corporate disclosure obtain mixed results. We develop an economic model to capture the endogeneity between disclosure and litigation. Equilibrium disclosure is determined by two countervailing effects of litigation, a deterrence effect and an insurance effect. We derive four key results. (i) Decreasing litigation risk leads to less disclosure of very bad news, due to a weakening of the deterrence effect, but to more disclosure of weakly bad news, due to a weakening of the insurance effect. (ii) Given a sufficiently large information asymmetry, litigation risk dampens (boosts) overall disclosure of bad news for low (high) litigation risk firms. (iii) Capital markets respond more to the disclosure of bad news than of good news if the deterrence effect is strong, which arises if both insiders’ penalties and litigation risk are high. (iv) In an extension, we highlight real effects of litigation on corporate innovation and establish that innovation first decreases and then increases (strictly decreases) with litigation risk if insiders’ penalties are small (large). We reconcile our findings with results from a large set of U.S.-based empirical studies and make several novel predictions.</p>","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"28 13","pages":""},"PeriodicalIF":5.8000,"publicationDate":"2023-07-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s11142-023-09778-5","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

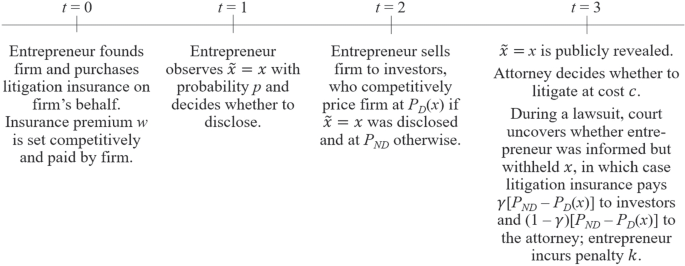

Empirical studies on the relationship between shareholder litigation and corporate disclosure obtain mixed results. We develop an economic model to capture the endogeneity between disclosure and litigation. Equilibrium disclosure is determined by two countervailing effects of litigation, a deterrence effect and an insurance effect. We derive four key results. (i) Decreasing litigation risk leads to less disclosure of very bad news, due to a weakening of the deterrence effect, but to more disclosure of weakly bad news, due to a weakening of the insurance effect. (ii) Given a sufficiently large information asymmetry, litigation risk dampens (boosts) overall disclosure of bad news for low (high) litigation risk firms. (iii) Capital markets respond more to the disclosure of bad news than of good news if the deterrence effect is strong, which arises if both insiders’ penalties and litigation risk are high. (iv) In an extension, we highlight real effects of litigation on corporate innovation and establish that innovation first decreases and then increases (strictly decreases) with litigation risk if insiders’ penalties are small (large). We reconcile our findings with results from a large set of U.S.-based empirical studies and make several novel predictions.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们