{"title":"Relationality in transaction cost economics and stakeholder theory: A new conceptual framework","authors":"Vladislav Valentinov, Steffen Roth","doi":"10.1111/beer.12652","DOIUrl":null,"url":null,"abstract":"<p>Stakeholder scholars have long explored how stakeholder relationships differ from economic transactions. We contribute to this ongoing inquiry by developing a conceptual framework of relationality in stakeholder theory that encompasses a stakeholder-theoretic extension of Williamson's contracting schema and a new typology of stakeholder relationships. Premised on understanding relationality as the need for informal human relationships beyond formal governance, our framework locates the key difference between transaction cost economics and stakeholder theory in their treatment of informal relationships. While transaction cost economics perceives informal relationships to be shaped by formal governance structures and enforced by contractual safeguards, stakeholder theory is open to the possibility that some informal relationships between stakeholders may be genuinely moral and thus irreducible to formal governance and contractual safeguards. These stakeholder relationships may lead to unique economic effects described by instrumental stakeholder theory. The difference that we identified between the two literatures shows how stakeholder theory's embrace of relationality surpasses that of transaction cost economics.</p>","PeriodicalId":29886,"journal":{"name":"Business Ethics the Environment & Responsibility","volume":"33 3","pages":"535-546"},"PeriodicalIF":4.2000,"publicationDate":"2024-01-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/beer.12652","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Business Ethics the Environment & Responsibility","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/beer.12652","RegionNum":2,"RegionCategory":"哲学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 0

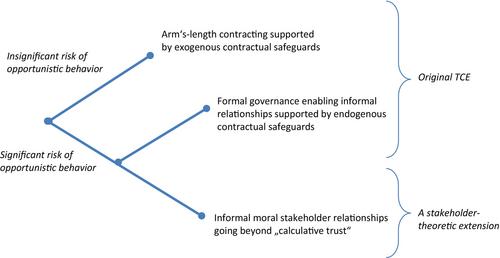

Abstract

Stakeholder scholars have long explored how stakeholder relationships differ from economic transactions. We contribute to this ongoing inquiry by developing a conceptual framework of relationality in stakeholder theory that encompasses a stakeholder-theoretic extension of Williamson's contracting schema and a new typology of stakeholder relationships. Premised on understanding relationality as the need for informal human relationships beyond formal governance, our framework locates the key difference between transaction cost economics and stakeholder theory in their treatment of informal relationships. While transaction cost economics perceives informal relationships to be shaped by formal governance structures and enforced by contractual safeguards, stakeholder theory is open to the possibility that some informal relationships between stakeholders may be genuinely moral and thus irreducible to formal governance and contractual safeguards. These stakeholder relationships may lead to unique economic effects described by instrumental stakeholder theory. The difference that we identified between the two literatures shows how stakeholder theory's embrace of relationality surpasses that of transaction cost economics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们