{"title":"Cascade model for Australian housing","authors":"Gaurav Khemka, Yifu Tang, Geoffrey J. Warren","doi":"10.1111/1467-8454.12337","DOIUrl":null,"url":null,"abstract":"<p>We design a ‘cascade model’ that integrates projections for Australian housing with inflation, incomes and asset markets over long horizons. The model allows simulating joint ‘paths’ for inflation, wages, cash rates, mortgage rates, rents, rental yields, house prices and fund returns. The cascade model structure ensures that equilibrium relationships are maintained between the variables when projecting over very long time periods. It achieves this through linking either growth rates or levels for variables in a manner that ensures consistent trends emerge within each simulated path over the very long-term, thus avoiding excessively divergent behaviour between variables with common underlying fundamentals.</p>","PeriodicalId":46169,"journal":{"name":"Australian Economic Papers","volume":"63 3","pages":"406-426"},"PeriodicalIF":1.7000,"publicationDate":"2024-01-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8454.12337","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Economic Papers","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1467-8454.12337","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

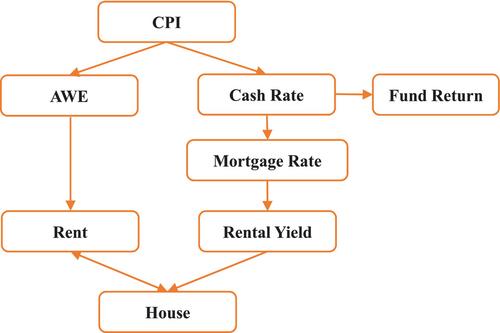

We design a ‘cascade model’ that integrates projections for Australian housing with inflation, incomes and asset markets over long horizons. The model allows simulating joint ‘paths’ for inflation, wages, cash rates, mortgage rates, rents, rental yields, house prices and fund returns. The cascade model structure ensures that equilibrium relationships are maintained between the variables when projecting over very long time periods. It achieves this through linking either growth rates or levels for variables in a manner that ensures consistent trends emerge within each simulated path over the very long-term, thus avoiding excessively divergent behaviour between variables with common underlying fundamentals.

期刊介绍:

Australian Economic Papers publishes innovative and thought provoking contributions that extend the frontiers of the subject, written by leading international economists in theoretical, empirical and policy economics. Australian Economic Papers is a forum for debate between theorists, econometricians and policy analysts and covers an exceptionally wide range of topics on all the major fields of economics as well as: theoretical and empirical industrial organisation, theoretical and empirical labour economics and, macro and micro policy analysis.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们