{"title":"Modeling flight delays by an intensity-based Hawkes process","authors":"Philip Hans Franses, Carlijn Smeets","doi":"10.1002/asmb.2846","DOIUrl":null,"url":null,"abstract":"<p>Two key features of airline departure delays are that they cascade and that there can be exceptional peaks. We model these features using an intensity-based Hawkes process. Our application to all KLM departure delays at Amsterdam Schiphol airport in January 2015 shows that volatility in departure delays is endogenous. We correlate the key parameters of the estimated Hawkes process with daily weather conditions and find that these conditions amplify the self-exciting feature of departure delays.</p>","PeriodicalId":55495,"journal":{"name":"Applied Stochastic Models in Business and Industry","volume":"40 4","pages":"863-874"},"PeriodicalIF":1.5000,"publicationDate":"2024-02-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2846","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Applied Stochastic Models in Business and Industry","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2846","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

引用次数: 0

Abstract

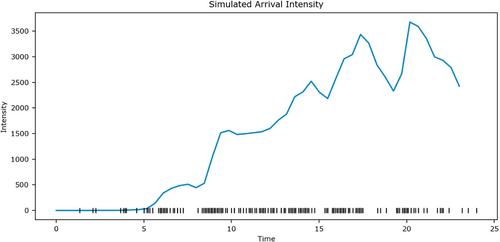

Two key features of airline departure delays are that they cascade and that there can be exceptional peaks. We model these features using an intensity-based Hawkes process. Our application to all KLM departure delays at Amsterdam Schiphol airport in January 2015 shows that volatility in departure delays is endogenous. We correlate the key parameters of the estimated Hawkes process with daily weather conditions and find that these conditions amplify the self-exciting feature of departure delays.

期刊介绍:

ASMBI - Applied Stochastic Models in Business and Industry (formerly Applied Stochastic Models and Data Analysis) was first published in 1985, publishing contributions in the interface between stochastic modelling, data analysis and their applications in business, finance, insurance, management and production. In 2007 ASMBI became the official journal of the International Society for Business and Industrial Statistics (www.isbis.org). The main objective is to publish papers, both technical and practical, presenting new results which solve real-life problems or have great potential in doing so. Mathematical rigour, innovative stochastic modelling and sound applications are the key ingredients of papers to be published, after a very selective review process.

The journal is very open to new ideas, like Data Science and Big Data stemming from problems in business and industry or uncertainty quantification in engineering, as well as more traditional ones, like reliability, quality control, design of experiments, managerial processes, supply chains and inventories, insurance, econometrics, financial modelling (provided the papers are related to real problems). The journal is interested also in papers addressing the effects of business and industrial decisions on the environment, healthcare, social life. State-of-the art computational methods are very welcome as well, when combined with sound applications and innovative models.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们