{"title":"Nelson and Plosser revisited: macroeconomic and financial stability of Turkey","authors":"Saban Nazlioglu, Dogukan Tarakci, Emre Kilic","doi":"10.1007/s00181-023-02536-1","DOIUrl":null,"url":null,"abstract":"<p>Since the seminal paper of Nelson and Plosser (J Monet Econ 10(2):139–162, 1982), analyzing the nature of shocks to macroeconomic and financial data has attracted great attention and it continues to be up-to-date, especially, in conjunction with the advances in unit root literature. This paper examines the persistence in macroeconomic and financial variables for Turkey by means of the recent developments in the quantile autoregression models to account for non-normal distributions, structural changes, and asymmetric dynamics. The results show that while the conventional unit root approaches fail to reject the null hypothesis of unit root for most the of 30 macroeconomic and financial time series, the nonlinear quantile unit root test with smooth structural changes supports evidence on a stable long-run equilibrium for 23 variables. It further reveals asymmetric persistence in most of the Turkey’s macroeconomic and financial data, implying that the effect of an economic shock in inflationary state is different than that in recessionary state.</p>","PeriodicalId":11642,"journal":{"name":"Empirical Economics","volume":"91 1","pages":""},"PeriodicalIF":1.9000,"publicationDate":"2024-02-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Empirical Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00181-023-02536-1","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

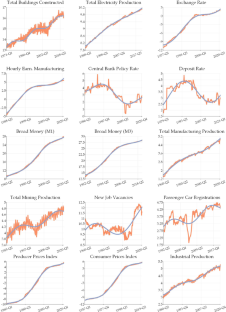

Abstract

Since the seminal paper of Nelson and Plosser (J Monet Econ 10(2):139–162, 1982), analyzing the nature of shocks to macroeconomic and financial data has attracted great attention and it continues to be up-to-date, especially, in conjunction with the advances in unit root literature. This paper examines the persistence in macroeconomic and financial variables for Turkey by means of the recent developments in the quantile autoregression models to account for non-normal distributions, structural changes, and asymmetric dynamics. The results show that while the conventional unit root approaches fail to reject the null hypothesis of unit root for most the of 30 macroeconomic and financial time series, the nonlinear quantile unit root test with smooth structural changes supports evidence on a stable long-run equilibrium for 23 variables. It further reveals asymmetric persistence in most of the Turkey’s macroeconomic and financial data, implying that the effect of an economic shock in inflationary state is different than that in recessionary state.

期刊介绍:

Empirical Economics publishes high quality papers using econometric or statistical methods to fill the gap between economic theory and observed data. Papers explore such topics as estimation of established relationships between economic variables, testing of hypotheses derived from economic theory, treatment effect estimation, policy evaluation, simulation, forecasting, as well as econometric methods and measurement. Empirical Economics emphasizes the replicability of empirical results. Replication studies of important results in the literature - both positive and negative results - may be published as short papers in Empirical Economics. Authors of all accepted papers and replications are required to submit all data and codes prior to publication (for more details, see: Instructions for Authors).The journal follows a single blind review procedure. In order to ensure the high quality of the journal and an efficient editorial process, a substantial number of submissions that have very poor chances of receiving positive reviews are routinely rejected without sending the papers for review.Officially cited as: Empir Econ

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们