{"title":"Introducing shrinkage in heavy-tailed state space models to predict equity excess returns.","authors":"Florian Huber, Gregor Kastner, Michael Pfarrhofer","doi":"10.1007/s00181-023-02437-3","DOIUrl":null,"url":null,"abstract":"<p><p>We forecast excess returns of the S &P 500 index using a flexible Bayesian econometric state space model with non-Gaussian features at several levels. More precisely, we control for overparameterization via global-local shrinkage priors on the state innovation variances as well as the time-invariant part of the state space model. The shrinkage priors are complemented by heavy tailed state innovations that cater for potential large breaks in the latent states, even if the degree of shrinkage introduced is high. Moreover, we allow for leptokurtic stochastic volatility in the observation equation. The empirical findings indicate that several variants of the proposed approach outperform typical competitors frequently used in the literature, both in terms of point and density forecasts.</p>","PeriodicalId":11642,"journal":{"name":"Empirical Economics","volume":"1 1","pages":"535-553"},"PeriodicalIF":1.9000,"publicationDate":"2025-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC11794411/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Empirical Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00181-023-02437-3","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/5/29 0:00:00","PubModel":"Epub","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

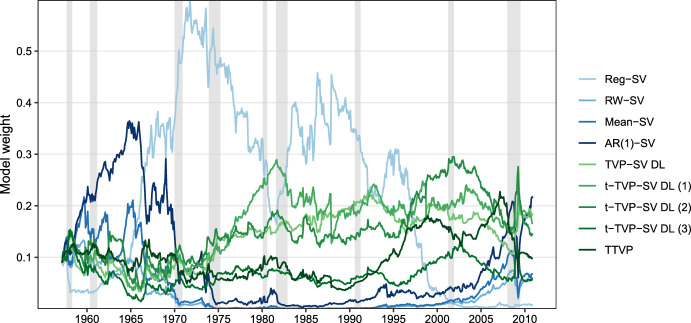

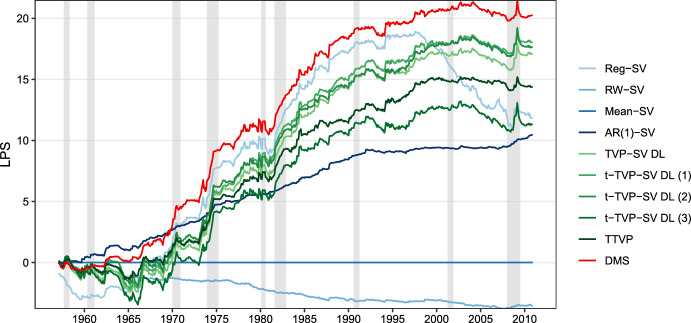

We forecast excess returns of the S &P 500 index using a flexible Bayesian econometric state space model with non-Gaussian features at several levels. More precisely, we control for overparameterization via global-local shrinkage priors on the state innovation variances as well as the time-invariant part of the state space model. The shrinkage priors are complemented by heavy tailed state innovations that cater for potential large breaks in the latent states, even if the degree of shrinkage introduced is high. Moreover, we allow for leptokurtic stochastic volatility in the observation equation. The empirical findings indicate that several variants of the proposed approach outperform typical competitors frequently used in the literature, both in terms of point and density forecasts.

期刊介绍:

Empirical Economics publishes high quality papers using econometric or statistical methods to fill the gap between economic theory and observed data. Papers explore such topics as estimation of established relationships between economic variables, testing of hypotheses derived from economic theory, treatment effect estimation, policy evaluation, simulation, forecasting, as well as econometric methods and measurement. Empirical Economics emphasizes the replicability of empirical results. Replication studies of important results in the literature - both positive and negative results - may be published as short papers in Empirical Economics. Authors of all accepted papers and replications are required to submit all data and codes prior to publication (for more details, see: Instructions for Authors).The journal follows a single blind review procedure. In order to ensure the high quality of the journal and an efficient editorial process, a substantial number of submissions that have very poor chances of receiving positive reviews are routinely rejected without sending the papers for review.Officially cited as: Empir Econ

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们