{"title":"Quantile network connectedness between oil, clean energy markets, and green equity with portfolio implications","authors":"Mohamed Yousfi, Houssam Bouzgarrou","doi":"10.1007/s10018-024-00393-5","DOIUrl":null,"url":null,"abstract":"<p>This study aims to explore the dynamic return and volatility spillover among oil, sectoral clean energy markets, and green equity across different tails spanning from January 2014 to May 2023. The investigation utilizes a spillover approach based on the QVAR model. The empirical results highlight the time-varying nature of return and volatility spillover indices, influenced by significant events. Notably, the interconnection intensified during pivotal periods, including the oil shale revolution, the COVID-19 pandemic, and the Russia–Ukraine conflict, observed across the median, lower, and upper tails. The quantile spillover analysis reveals asymmetric behavior at both the left and right tails, emphasizing the increased impact of large shocks compared to smaller ones. Additionally, the directional spillover exhibits variability across quantiles. In conclusion, we present several diversification benefits for environmentally conscious investors to reduce portfolio risk without compromising sustainability goals. This is achieved by strategically investing in eco-friendly assets to maintain portfolios with low carbon. Indeed, policymakers should consider the impact of global events, such as economic crises and geopolitical conflicts, on financial market dynamics, recognizing the need for measures that enhance stability and facilitate a smooth transition to green finance.</p>","PeriodicalId":46150,"journal":{"name":"Environmental Economics and Policy Studies","volume":"66 1","pages":""},"PeriodicalIF":2.3000,"publicationDate":"2024-02-27","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Environmental Economics and Policy Studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s10018-024-00393-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

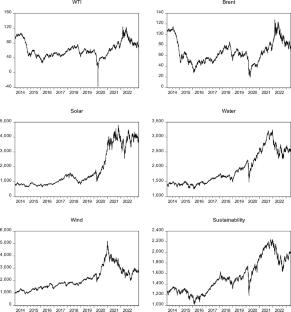

This study aims to explore the dynamic return and volatility spillover among oil, sectoral clean energy markets, and green equity across different tails spanning from January 2014 to May 2023. The investigation utilizes a spillover approach based on the QVAR model. The empirical results highlight the time-varying nature of return and volatility spillover indices, influenced by significant events. Notably, the interconnection intensified during pivotal periods, including the oil shale revolution, the COVID-19 pandemic, and the Russia–Ukraine conflict, observed across the median, lower, and upper tails. The quantile spillover analysis reveals asymmetric behavior at both the left and right tails, emphasizing the increased impact of large shocks compared to smaller ones. Additionally, the directional spillover exhibits variability across quantiles. In conclusion, we present several diversification benefits for environmentally conscious investors to reduce portfolio risk without compromising sustainability goals. This is achieved by strategically investing in eco-friendly assets to maintain portfolios with low carbon. Indeed, policymakers should consider the impact of global events, such as economic crises and geopolitical conflicts, on financial market dynamics, recognizing the need for measures that enhance stability and facilitate a smooth transition to green finance.

期刊介绍:

As the official journal of the Society for Environmental Economics and Policy Studies and the official journal of the Asian Association of Environmental and Resource Economics, it provides an international forum for debates among diverse disciplines such as environmental economics, environmental policy studies, and related fields. The main purpose of the journal is twofold: to encourage (1) integration of theoretical studies and policy studies on environmental issues and (2) interdisciplinary works of environmental economics, environmental policy studies, and related fields on environmental issues. The journal also welcomes contributions from any discipline as long as they are consistent with the above stated aims and purposes, and encourages interaction beyond the traditional schools of thought.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们