{"title":"Attractive target for tax avoidance: trade liberalization and entry mode","authors":"Hirofumi Okoshi","doi":"10.1007/s10797-024-09830-3","DOIUrl":null,"url":null,"abstract":"<p>Growing foreign direct investments (FDIs) have been observed in parallel to the development of tax avoidance by multinational enterprises; however, empirical evidence indicates the asymmetric effects of trade costs on a firm’s entry decision. To give a new rationale and insights into the impacts of transfer pricing and trade liberalization on a firm’s global activities, this study incorporates transfer pricing and investigates a foreign firm’s entry decision: exports, greenfield FDI (GFDI), or cross-border mergers and acquisitions (CM&As). We show that CM&A is the equilibrium entry mode when transfer pricing regulation is loose, whereas the choice between exports and GFDI depends on the fixed costs of GFDI. Moreover, trade liberalization increases the likelihood of CM&A but decreases that of exports because a reduction in trade costs enhances tax-avoidance efficiency due to more intrafirm trade, implying that tax avoidance in the form of CM&A becomes crucial as globalization progresses. Our welfare analysis shows that regulating CM&A based on consumers’ benefits may result in welfare reduction because profit shifting is most effective under CM&A and a host country’s tax revenue from the foreign firm increases. The results imply the importance of considering the link between international tax and antitrust policies.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"33 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-03-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-024-09830-3","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

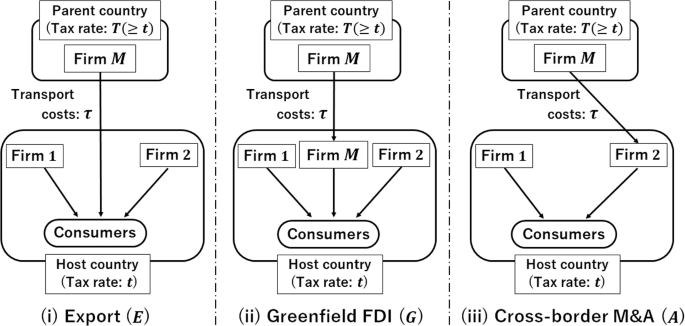

Abstract

Growing foreign direct investments (FDIs) have been observed in parallel to the development of tax avoidance by multinational enterprises; however, empirical evidence indicates the asymmetric effects of trade costs on a firm’s entry decision. To give a new rationale and insights into the impacts of transfer pricing and trade liberalization on a firm’s global activities, this study incorporates transfer pricing and investigates a foreign firm’s entry decision: exports, greenfield FDI (GFDI), or cross-border mergers and acquisitions (CM&As). We show that CM&A is the equilibrium entry mode when transfer pricing regulation is loose, whereas the choice between exports and GFDI depends on the fixed costs of GFDI. Moreover, trade liberalization increases the likelihood of CM&A but decreases that of exports because a reduction in trade costs enhances tax-avoidance efficiency due to more intrafirm trade, implying that tax avoidance in the form of CM&A becomes crucial as globalization progresses. Our welfare analysis shows that regulating CM&A based on consumers’ benefits may result in welfare reduction because profit shifting is most effective under CM&A and a host country’s tax revenue from the foreign firm increases. The results imply the importance of considering the link between international tax and antitrust policies.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们