{"title":"Expected inflation and interest-rate dynamics in the COVID era: evidence from the time–frequency domain","authors":"Mihai Ioan Mutascu, Scott W. Hegerty","doi":"10.1007/s10663-024-09610-6","DOIUrl":null,"url":null,"abstract":"<p>The onset of the COVID-19 pandemic in the United States may have led investors or other individuals to expect sharp drops in output and rising prices, as well as drastic changes in fiscal and/or monetary to deal with the crisis. This paper analyses the co-movement between expected inflation and interest in the U.S. by using a battery of wavelet tools over the period from January 21, 2020 to March 28, 2022. Wavelet methods are used to examine the linkages between expected inflation and nominal interest rates of varying terms, focusing on the direction of co-movement and their sub-time horizons. Both bivariate wavelet and partial wavelet models that incorporate daily COVID-19 case counts or a financial stress variable find that the relationship holds primarily in the longer short-run (more than 6 months), with connections stronger for maturities of 5 years than for 1 year or less. The expectation related to the ‘inflation–interest rate’ nexus and type of bond maturity seem to be significantly shaped by the pandemic peak and anticipated duration of the disease. More precisely, the longer the anticipated duration of the pandemic is, the higher the expected inflation rate, bond yield rate, and maturity are. The interaction between expected inflation and interest seems to be very sensitive to pandemic and financial stress in terms of lead-lag status, in the very short to short-run, for 5 and 10 years bond maturity. This seems to be explained by investor hazard to a new particular unknown stimulus caused by the pandemic and its socio-economic consequences.</p>","PeriodicalId":46526,"journal":{"name":"Empirica","volume":"47 1","pages":""},"PeriodicalIF":1.8000,"publicationDate":"2024-04-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Empirica","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10663-024-09610-6","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

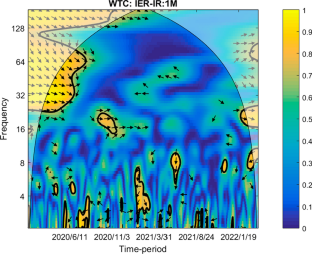

Abstract

The onset of the COVID-19 pandemic in the United States may have led investors or other individuals to expect sharp drops in output and rising prices, as well as drastic changes in fiscal and/or monetary to deal with the crisis. This paper analyses the co-movement between expected inflation and interest in the U.S. by using a battery of wavelet tools over the period from January 21, 2020 to March 28, 2022. Wavelet methods are used to examine the linkages between expected inflation and nominal interest rates of varying terms, focusing on the direction of co-movement and their sub-time horizons. Both bivariate wavelet and partial wavelet models that incorporate daily COVID-19 case counts or a financial stress variable find that the relationship holds primarily in the longer short-run (more than 6 months), with connections stronger for maturities of 5 years than for 1 year or less. The expectation related to the ‘inflation–interest rate’ nexus and type of bond maturity seem to be significantly shaped by the pandemic peak and anticipated duration of the disease. More precisely, the longer the anticipated duration of the pandemic is, the higher the expected inflation rate, bond yield rate, and maturity are. The interaction between expected inflation and interest seems to be very sensitive to pandemic and financial stress in terms of lead-lag status, in the very short to short-run, for 5 and 10 years bond maturity. This seems to be explained by investor hazard to a new particular unknown stimulus caused by the pandemic and its socio-economic consequences.

期刊介绍:

Empirica is a peer-reviewed journal, which publishes original research of general interest to an international audience. Authors are invited to submit empirical papers in all areas of economics with a particular focus on European economies. Per January 2021, the editors also solicit descriptive papers on current or unexplored topics.

Founded in 1974, Empirica is the official journal of the Nationalökonomische Gesellschaft (Austrian Economic Association) and is published in cooperation with Austrian Institute of Economic Research (WIFO). The journal aims at a wide international audience and invites submissions from economists around the world.

Officially cited as: Empirica

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们