Badryah Alhusaini, Andrew C. Call, Kimball Chapman

{"title":"Analyst information about peer firms during the IPO quiet period","authors":"Badryah Alhusaini, Andrew C. Call, Kimball Chapman","doi":"10.1007/s11142-024-09824-w","DOIUrl":null,"url":null,"abstract":"<p>The SEC limits sell-side analysts’ research activities on IPO firms both before and immediately after going public (the IPO quiet period). However, during the IPO quiet period, analysts provide regular coverage of IPO peer firms, which is potentially relevant to investors seeking to glean information about the IPO firm itself. We examine whether, despite the restrictions on analyst research of IPO firms during the quiet period, investors uncover information about the IPO firm indirectly through analyst research of peer firms. We find that, on the IPO date, institutional investors trade on the information in analysts’ recommendation revisions of peer firms that were issued earlier in the quiet period. Institutional investors also trade in the short window around analyst revisions of peer firms that are issued later in the quiet period (after the IPO date) but before analysts initiate coverage of the IPO firm. Retail investors, however, are inattentive to the information available in analyst research of peer firms. Importantly, our findings vary predictably with attributes of the issuing analyst, which helps rule out firm- and industry-level alternative explanations. Lastly, we find that recommendation revisions analysts issue for peer firms predict future IPO-firm performance, suggesting that analyst research of peer firms during the quiet period conveys meaningful information about the IPO firm that results in an information advantage for institutional investors.</p>","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"81 1","pages":""},"PeriodicalIF":5.8000,"publicationDate":"2024-04-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s11142-024-09824-w","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

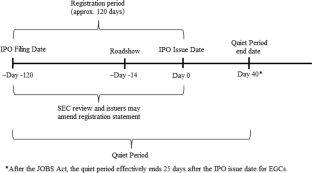

The SEC limits sell-side analysts’ research activities on IPO firms both before and immediately after going public (the IPO quiet period). However, during the IPO quiet period, analysts provide regular coverage of IPO peer firms, which is potentially relevant to investors seeking to glean information about the IPO firm itself. We examine whether, despite the restrictions on analyst research of IPO firms during the quiet period, investors uncover information about the IPO firm indirectly through analyst research of peer firms. We find that, on the IPO date, institutional investors trade on the information in analysts’ recommendation revisions of peer firms that were issued earlier in the quiet period. Institutional investors also trade in the short window around analyst revisions of peer firms that are issued later in the quiet period (after the IPO date) but before analysts initiate coverage of the IPO firm. Retail investors, however, are inattentive to the information available in analyst research of peer firms. Importantly, our findings vary predictably with attributes of the issuing analyst, which helps rule out firm- and industry-level alternative explanations. Lastly, we find that recommendation revisions analysts issue for peer firms predict future IPO-firm performance, suggesting that analyst research of peer firms during the quiet period conveys meaningful information about the IPO firm that results in an information advantage for institutional investors.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们