Kee-Hong Bae, Zhaoran (Jason) Gong, Wilson H. S. Tong

{"title":"Restricting CEO pay backfires: Evidence from China","authors":"Kee-Hong Bae, Zhaoran (Jason) Gong, Wilson H. S. Tong","doi":"10.1111/jbfa.12741","DOIUrl":null,"url":null,"abstract":"<p>Using the pay restriction imposed on CEOs of centrally administered state-owned enterprises (CSOEs) in China in 2009, we study the effects of limiting CEO pay. Compared with CEOs of firms not subject to the restriction, the CEOs of CSOEs experienced a significant pay cut. In response to the pay cut, CEOs increased the consumption of perks and siphoned off firm resources for their own benefit. Pay-performance sensitivity for these firms also significantly decreases. The performance of these firms dropped following the pay restriction. Our findings suggest that restricting CEO pay distorts CEO incentives and brings unintended consequences. Our findings caution against limiting CEO pay.</p>","PeriodicalId":48106,"journal":{"name":"Journal of Business Finance & Accounting","volume":"51 5-6","pages":"1015-1045"},"PeriodicalIF":2.4000,"publicationDate":"2023-07-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12741","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Business Finance & Accounting","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12741","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

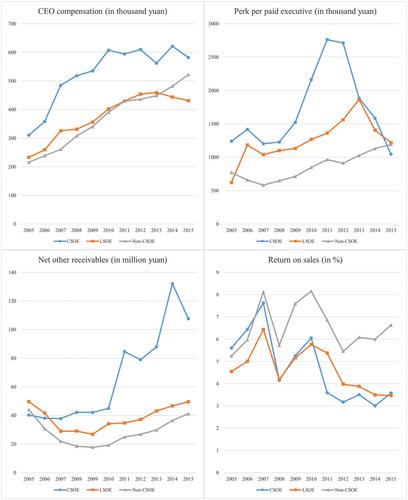

Using the pay restriction imposed on CEOs of centrally administered state-owned enterprises (CSOEs) in China in 2009, we study the effects of limiting CEO pay. Compared with CEOs of firms not subject to the restriction, the CEOs of CSOEs experienced a significant pay cut. In response to the pay cut, CEOs increased the consumption of perks and siphoned off firm resources for their own benefit. Pay-performance sensitivity for these firms also significantly decreases. The performance of these firms dropped following the pay restriction. Our findings suggest that restricting CEO pay distorts CEO incentives and brings unintended consequences. Our findings caution against limiting CEO pay.

我们利用 2009 年中国对中央管理国有企业(CSOE)CEO 实施的薪酬限制,研究了限制 CEO 薪酬的效果。与未受限薪措施影响的企业 CEO 相比,中央管理国有企业的 CEO 经历了大幅减薪。作为对减薪的回应,首席执行官们增加了福利消费,并为自身利益抽走了公司资源。这些企业的薪酬-绩效敏感度也显著下降。限薪后,这些公司的业绩下降。我们的研究结果表明,限制 CEO 薪酬会扭曲 CEO 的激励机制,带来意想不到的后果。我们的研究结果提醒我们不要限制首席执行官的薪酬。

期刊介绍:

Journal of Business Finance and Accounting exists to publish high quality research papers in accounting, corporate finance, corporate governance and their interfaces. The interfaces are relevant in many areas such as financial reporting and communication, valuation, financial performance measurement and managerial reward and control structures. A feature of JBFA is that it recognises that informational problems are pervasive in financial markets and business organisations, and that accounting plays an important role in resolving such problems. JBFA welcomes both theoretical and empirical contributions. Nonetheless, theoretical papers should yield novel testable implications, and empirical papers should be theoretically well-motivated. The Editors view accounting and finance as being closely related to economics and, as a consequence, papers submitted will often have theoretical motivations that are grounded in economics. JBFA, however, also seeks papers that complement economics-based theorising with theoretical developments originating in other social science disciplines or traditions. While many papers in JBFA use econometric or related empirical methods, the Editors also welcome contributions that use other empirical research methods. Although the scope of JBFA is broad, it is not a suitable outlet for highly abstract mathematical papers, or empirical papers with inadequate theoretical motivation. Also, papers that study asset pricing, or the operations of financial markets, should have direct implications for one or more of preparers, regulators, users of financial statements, and corporate financial decision makers, or at least should have implications for the development of future research relevant to such users.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们