RACHEL M. HAYES, FENG JIANG, YIHUI PAN, HUAYI TANG

{"title":"Racial Disparities in Financial Complaints and the Role of Corporate Social Attitudes","authors":"RACHEL M. HAYES, FENG JIANG, YIHUI PAN, HUAYI TANG","doi":"10.1111/1475-679X.12612","DOIUrl":null,"url":null,"abstract":"<p>Using consumer complaints filed with the Consumer Financial Protection Bureau as a measure for the quality of financial products and services, we present evidence of racial disparities in the service quality received by consumers. Consumers in high-minority communities file more complaints than those in low-minority communities, and the racial gap in financial complaints increased by more than 60% during the COVID-19 pandemic. Using a triple-difference approach, we establish the role of corporate social attitudes, reflected in, for example, inclusive promotion practices and diversity in leadership, in mitigating the complaint racial gap and its pandemic-period increase. Our results shed light on how inclusive corporate culture filters through an organization to benefit minority communities and underscore the effect of corporate social attitudes on important stakeholder outcomes.</p>","PeriodicalId":48414,"journal":{"name":"Journal of Accounting Research","volume":"63 4","pages":"1289-1333"},"PeriodicalIF":6.3000,"publicationDate":"2025-03-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12612","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12612","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

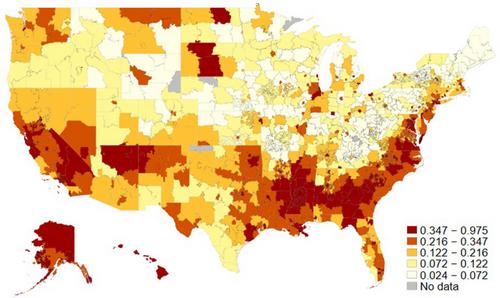

Using consumer complaints filed with the Consumer Financial Protection Bureau as a measure for the quality of financial products and services, we present evidence of racial disparities in the service quality received by consumers. Consumers in high-minority communities file more complaints than those in low-minority communities, and the racial gap in financial complaints increased by more than 60% during the COVID-19 pandemic. Using a triple-difference approach, we establish the role of corporate social attitudes, reflected in, for example, inclusive promotion practices and diversity in leadership, in mitigating the complaint racial gap and its pandemic-period increase. Our results shed light on how inclusive corporate culture filters through an organization to benefit minority communities and underscore the effect of corporate social attitudes on important stakeholder outcomes.

期刊介绍:

The Journal of Accounting Research is a general-interest accounting journal. It publishes original research in all areas of accounting and related fields that utilizes tools from basic disciplines such as economics, statistics, psychology, and sociology. This research typically uses analytical, empirical archival, experimental, and field study methods and addresses economic questions, external and internal, in accounting, auditing, disclosure, financial reporting, taxation, and information as well as related fields such as corporate finance, investments, capital markets, law, contracting, and information economics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们