Christoph Huber, Parampreet C Bindra, Daniel Kleinlercher

{"title":"Design-features of bubble-prone experimental asset markets with a constant FV.","authors":"Christoph Huber, Parampreet C Bindra, Daniel Kleinlercher","doi":"10.1007/s40881-019-00061-5","DOIUrl":null,"url":null,"abstract":"<p><p>Experimental asset markets with a constant fundamental value ( <math><mstyle><mi>F</mi> <mi>V</mi></mstyle> </math> ) have grown in importance in recent years. A methodological examination of the robustness of experimental results in such a setting which has been shown to produce bubbles, however, is lacking. In a laboratory experiment with 280 subjects, we investigate whether specific design features are sufficient to influence experimental results. In detail, we (1) vary the visual representation of the price chart, and (2) provide subjects with full information about the FV process. We find overvaluation and bubble formation to be reduced when trading prices are displayed at the upper end of the price chart. Surprisingly, we do not find any effects when subjects have full information about the FV process.</p>","PeriodicalId":91563,"journal":{"name":"Journal of the Economic Science Association","volume":"5 2","pages":"197-209"},"PeriodicalIF":0.6000,"publicationDate":"2019-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1007/s40881-019-00061-5","citationCount":"2","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of the Economic Science Association","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s40881-019-00061-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2019/3/26 0:00:00","PubModel":"Epub","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 2

Abstract

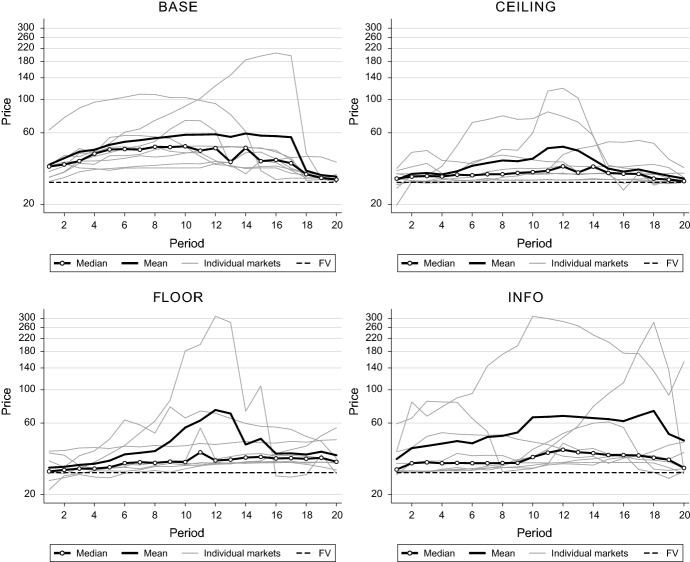

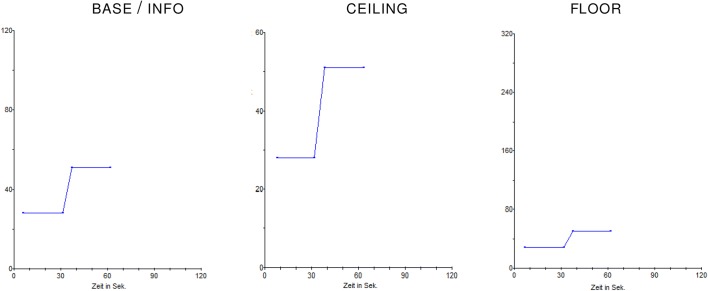

Experimental asset markets with a constant fundamental value ( ) have grown in importance in recent years. A methodological examination of the robustness of experimental results in such a setting which has been shown to produce bubbles, however, is lacking. In a laboratory experiment with 280 subjects, we investigate whether specific design features are sufficient to influence experimental results. In detail, we (1) vary the visual representation of the price chart, and (2) provide subjects with full information about the FV process. We find overvaluation and bubble formation to be reduced when trading prices are displayed at the upper end of the price chart. Surprisingly, we do not find any effects when subjects have full information about the FV process.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们