{"title":"Risk-return optimised energy asset allocation in transmission-distribution system using tangency portfolio and Black–Litterman model","authors":"Jisma M, Vivek Mohan, Mini Shaji Thomas","doi":"10.1049/esi2.12102","DOIUrl":null,"url":null,"abstract":"<p>The application of Markowitz and tangency portfolio and Black–Litterman models is extended by the authors to energy portfolio selection in transmission-distribution environments with high penetration of renewable energy. As Transmission System Operator (TSO) and Distribution System Operator (DSO) contextually take mutualistic or conflicting positions in their portfolio selection process, their risk-return interactions and behaviours depend on their subjective views on generation and operation. Here, the financial portfolio allocation tool Black–Litterman Model is adapted to incorporate subjective views of the operators to arrive at more intuitive portfolios. The best portfolios are searched within the acceptable risk-return search space of each operator defined by their Markowitz efficient frontiers (EF), for Pareto-optimising their profits. The tangency portfolio approach, which is generally used to determine the portfolio of risky and risk-free assets in finance, is used here to determine the portfolio of renewable (energy-risky) and fuel-based sources (energy-risk-free). The proposed methodology is adopted in an HV–MV interconnected test system operated by one TSO and two DSOs, having wind, solar, coal, gas and nuclear generation technologies. It is observed that completely customisable portfolios can be constructed for TSO and DSO based on their inherent financial and energy risk-return behaviours and posterior views.</p>","PeriodicalId":33288,"journal":{"name":"IET Energy Systems Integration","volume":"5 3","pages":"290-306"},"PeriodicalIF":1.7000,"publicationDate":"2023-05-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1049/esi2.12102","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"IET Energy Systems Integration","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1049/esi2.12102","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"ENERGY & FUELS","Score":null,"Total":0}

引用次数: 0

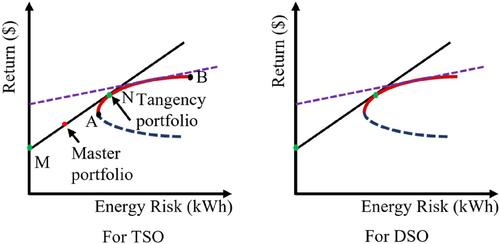

Abstract

The application of Markowitz and tangency portfolio and Black–Litterman models is extended by the authors to energy portfolio selection in transmission-distribution environments with high penetration of renewable energy. As Transmission System Operator (TSO) and Distribution System Operator (DSO) contextually take mutualistic or conflicting positions in their portfolio selection process, their risk-return interactions and behaviours depend on their subjective views on generation and operation. Here, the financial portfolio allocation tool Black–Litterman Model is adapted to incorporate subjective views of the operators to arrive at more intuitive portfolios. The best portfolios are searched within the acceptable risk-return search space of each operator defined by their Markowitz efficient frontiers (EF), for Pareto-optimising their profits. The tangency portfolio approach, which is generally used to determine the portfolio of risky and risk-free assets in finance, is used here to determine the portfolio of renewable (energy-risky) and fuel-based sources (energy-risk-free). The proposed methodology is adopted in an HV–MV interconnected test system operated by one TSO and two DSOs, having wind, solar, coal, gas and nuclear generation technologies. It is observed that completely customisable portfolios can be constructed for TSO and DSO based on their inherent financial and energy risk-return behaviours and posterior views.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们