{"title":"Forecasting inflation with a zero lower bound or negative interest rates: Evidence from point and density forecasts","authors":"Christina Anderl, Guglielmo Maria Caporale","doi":"10.1111/manc.12434","DOIUrl":null,"url":null,"abstract":"<p>This paper investigates the predictive power of the shadow rate for the inflation rate in countries with a zero lower bound (the US, the UK and Canada) and in those with negative rates (Japan, the Euro Area and Switzerland). Using shadow rates obtained from two different models (the WX(3) and the KANSM(2) ones) and for different LB parameters we compare the out-of-sample forecasting performance of an inflation model including a shadow rate with a benchmark one excluding it. Both specifications are estimated by OLS (Ordinary Least Squares) and includes a range of macroeconomic factors computed by means of principal component analysis. Both point and density forecasts of the inflation rate are evaluated. The models including the shadow rate are found to outperform the benchmark ones according to both sets of criteria except in countries operating an official inflation targeting regime. Both types of shadow rates appear to produce equally accurate out-of-sample inflation forecasts.</p>","PeriodicalId":47546,"journal":{"name":"Manchester School","volume":"91 3","pages":"171-232"},"PeriodicalIF":1.1000,"publicationDate":"2023-03-06","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/manc.12434","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Manchester School","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/manc.12434","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

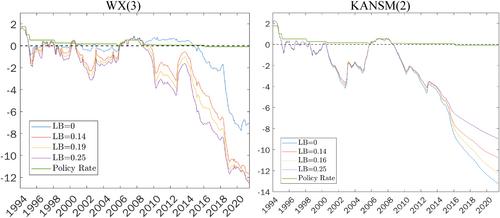

This paper investigates the predictive power of the shadow rate for the inflation rate in countries with a zero lower bound (the US, the UK and Canada) and in those with negative rates (Japan, the Euro Area and Switzerland). Using shadow rates obtained from two different models (the WX(3) and the KANSM(2) ones) and for different LB parameters we compare the out-of-sample forecasting performance of an inflation model including a shadow rate with a benchmark one excluding it. Both specifications are estimated by OLS (Ordinary Least Squares) and includes a range of macroeconomic factors computed by means of principal component analysis. Both point and density forecasts of the inflation rate are evaluated. The models including the shadow rate are found to outperform the benchmark ones according to both sets of criteria except in countries operating an official inflation targeting regime. Both types of shadow rates appear to produce equally accurate out-of-sample inflation forecasts.

期刊介绍:

The Manchester School was first published more than seventy years ago and has become a distinguished, internationally recognised, general economics journal. The Manchester School publishes high-quality research covering all areas of the economics discipline, although the editors particularly encourage original contributions, or authoritative surveys, in the fields of microeconomics (including industrial organisation and game theory), macroeconomics, econometrics (both theory and applied) and labour economics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们