{"title":"Neural networks for estimating Macro Asset Pricing model in football clubs","authors":"David Alaminos, Ignacio Esteban, M. Belén Salas","doi":"10.1002/isaf.1532","DOIUrl":null,"url":null,"abstract":"<p>The recent crisis caused by COVID-19 directly affected consumption habits and the stability sof financial markets. In particular, the football industry has been hit hard by this pandemic and therefore has more volatile stock prices. Given this new scenario, further research is needed to accurately estimate the value of the shares of football clubs. In this paper, we estimate an asset pricing model in football clubs with different compositions of risk nature using non-linear techniques of artificial neural networks. Usually, asset pricing models have been estimated with linear methods such as ordinary least squares. Our results show a precision higher than 90% for all the estimated models, which far exceeds those shown by linear methods in the previous literature. We find that the residual represents about 40% of the variance of the price-dividend ratio. Long-term risks follow in importance, and above all, the habit component and its behaviour in the face of changes. The importance of the residual component exists due to a low correlation between the asset price and consumer behaviour, but to a much lesser extent than that shown in previous studies. The estimation carried out with artificial neural networks, both the Deep Learning methods and especially the Quantum Neural Network, opens up new possibilities to estimate more efficiently the pricing of financial assets in the football industry.</p>","PeriodicalId":53473,"journal":{"name":"Intelligent Systems in Accounting, Finance and Management","volume":"30 2","pages":"57-75"},"PeriodicalIF":3.7000,"publicationDate":"2023-05-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/isaf.1532","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems in Accounting, Finance and Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1532","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

引用次数: 0

Abstract

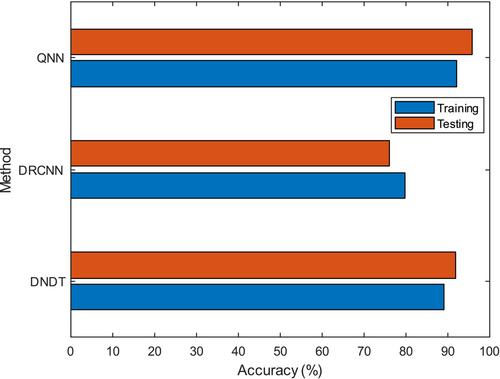

The recent crisis caused by COVID-19 directly affected consumption habits and the stability sof financial markets. In particular, the football industry has been hit hard by this pandemic and therefore has more volatile stock prices. Given this new scenario, further research is needed to accurately estimate the value of the shares of football clubs. In this paper, we estimate an asset pricing model in football clubs with different compositions of risk nature using non-linear techniques of artificial neural networks. Usually, asset pricing models have been estimated with linear methods such as ordinary least squares. Our results show a precision higher than 90% for all the estimated models, which far exceeds those shown by linear methods in the previous literature. We find that the residual represents about 40% of the variance of the price-dividend ratio. Long-term risks follow in importance, and above all, the habit component and its behaviour in the face of changes. The importance of the residual component exists due to a low correlation between the asset price and consumer behaviour, but to a much lesser extent than that shown in previous studies. The estimation carried out with artificial neural networks, both the Deep Learning methods and especially the Quantum Neural Network, opens up new possibilities to estimate more efficiently the pricing of financial assets in the football industry.

期刊介绍:

Intelligent Systems in Accounting, Finance and Management is a quarterly international journal which publishes original, high quality material dealing with all aspects of intelligent systems as they relate to the fields of accounting, economics, finance, marketing and management. In addition, the journal also is concerned with related emerging technologies, including big data, business intelligence, social media and other technologies. It encourages the development of novel technologies, and the embedding of new and existing technologies into applications of real, practical value. Therefore, implementation issues are of as much concern as development issues. The journal is designed to appeal to academics in the intelligent systems, emerging technologies and business fields, as well as to advanced practitioners who wish to improve the effectiveness, efficiency, or economy of their working practices. A special feature of the journal is the use of two groups of reviewers, those who specialize in intelligent systems work, and also those who specialize in applications areas. Reviewers are asked to address issues of originality and actual or potential impact on research, teaching, or practice in the accounting, finance, or management fields. Authors working on conceptual developments or on laboratory-based explorations of data sets therefore need to address the issue of potential impact at some level in submissions to the journal.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们