{"title":"Peer effects in subjective performance evaluation","authors":"Gavin Cassar, Taeho Ko","doi":"10.1111/1911-3846.12876","DOIUrl":null,"url":null,"abstract":"<p>We investigate the influence of peer quality on subjective performance evaluation using 75,413 ratings of 130 employees from 6,908 raters in a business school setting. We find that subjective performance ratings are lower for employees with higher quality peer groups in both randomized and nonrandomized settings. Using a novel long-window setting, we observe peer effects persisting, but slowly decaying, for several months even when priming raters with the employees' previous performance information. We find that the strength of the peer effects is greater for focal employees with weaker performance, for the peers with higher attribute similarity, and when the performance of peers is more extreme. Overall, we find strong and persistent peer effects in subjective performance evaluation.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"40 3","pages":"1704-1732"},"PeriodicalIF":3.8000,"publicationDate":"2023-05-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12876","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12876","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

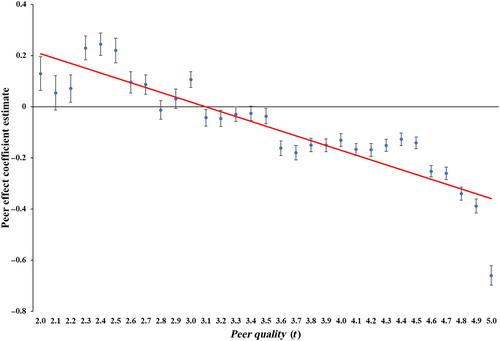

Abstract

We investigate the influence of peer quality on subjective performance evaluation using 75,413 ratings of 130 employees from 6,908 raters in a business school setting. We find that subjective performance ratings are lower for employees with higher quality peer groups in both randomized and nonrandomized settings. Using a novel long-window setting, we observe peer effects persisting, but slowly decaying, for several months even when priming raters with the employees' previous performance information. We find that the strength of the peer effects is greater for focal employees with weaker performance, for the peers with higher attribute similarity, and when the performance of peers is more extreme. Overall, we find strong and persistent peer effects in subjective performance evaluation.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们