{"title":"Social informedness and investor sentiment in the GameStop short squeeze.","authors":"Kwansoo Kim, Sang-Yong Tom Lee, Robert J Kauffman","doi":"10.1007/s12525-023-00632-9","DOIUrl":null,"url":null,"abstract":"<p><p>We examine investor behavior on social media platforms related to the GameStop (GME) short squeeze in early 2021. Individual investors stimulated the stock market via Reddit social posts in the presence of institutional investors who bet against GME's success as short sellers. We analyzed r/WallStreetBets subreddit posts related to GME's trading patterns. We performed text-based sentiment analysis and compared the social informedness of posting users for GME trading on two social media platforms. The short squeeze occurred due to coordinated trading by individual investors, who discussed trading strategies on the platforms and drove collective social informedness-based trading behavior. Our findings suggest that the valence and number of submissions influenced GME's intraday transaction volumes and precursors for irrational trading behavior patterns to have emerged. We provide a theoretical interpretation of what occurred and call for tighter monitoring of social news platforms. We also encourage effort to create an in-depth understanding of the observed patterns and the linkages between them and the larger equity markets.</p>","PeriodicalId":47719,"journal":{"name":"Electronic Markets","volume":"33 1","pages":"23"},"PeriodicalIF":6.8000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10203679/pdf/","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Electronic Markets","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s12525-023-00632-9","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/5/23 0:00:00","PubModel":"Epub","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 1

Abstract

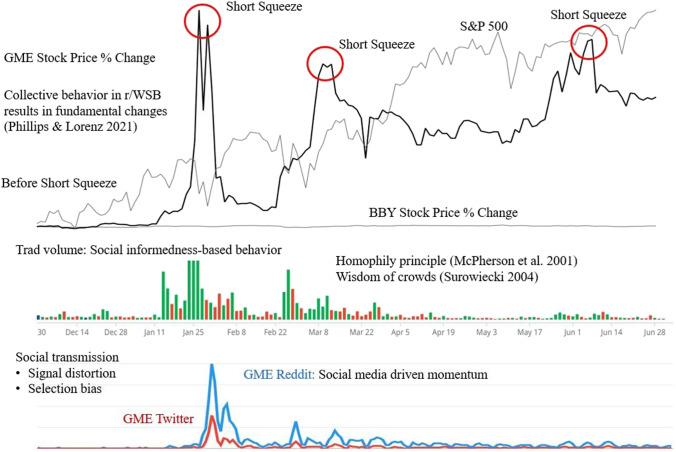

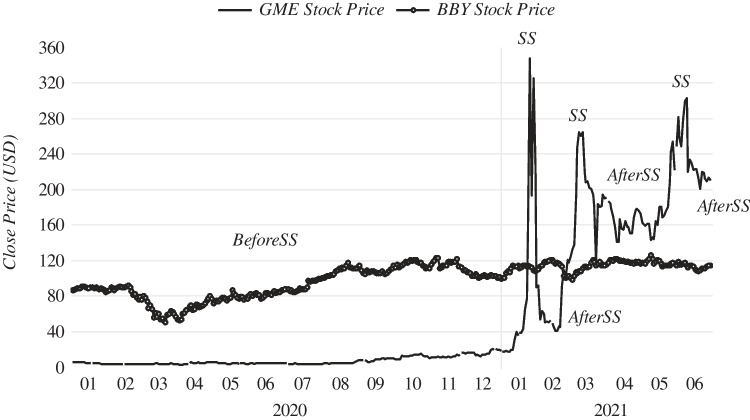

We examine investor behavior on social media platforms related to the GameStop (GME) short squeeze in early 2021. Individual investors stimulated the stock market via Reddit social posts in the presence of institutional investors who bet against GME's success as short sellers. We analyzed r/WallStreetBets subreddit posts related to GME's trading patterns. We performed text-based sentiment analysis and compared the social informedness of posting users for GME trading on two social media platforms. The short squeeze occurred due to coordinated trading by individual investors, who discussed trading strategies on the platforms and drove collective social informedness-based trading behavior. Our findings suggest that the valence and number of submissions influenced GME's intraday transaction volumes and precursors for irrational trading behavior patterns to have emerged. We provide a theoretical interpretation of what occurred and call for tighter monitoring of social news platforms. We also encourage effort to create an in-depth understanding of the observed patterns and the linkages between them and the larger equity markets.

期刊介绍:

Electronic Markets (EM) stands as a premier academic journal providing a dynamic platform for research into various forms of networked business. Recognizing the pivotal role of information and communication technology (ICT), EM delves into how ICT transforms the interactions between organizations and customers across diverse domains such as social networks, electronic commerce, supply chain management, and customer relationship management.

Electronic markets, in essence, encompass the realms of networked business where multiple suppliers and customers engage in economic transactions within single or multiple tiers of economic value chains. This broad concept encompasses various forms, including allocation platforms with dynamic price discovery mechanisms, fostering atomistic relationships. Notable examples originate from financial markets (e.g., CBOT, XETRA) and energy markets (e.g., EEX, ICE). Join us in exploring the multifaceted landscape of electronic markets and their transformative impact on business interactions and dynamics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们