{"title":"Innovative domestic financing mechanisms for health in Africa: An evidence review.","authors":"Nouria Brikci","doi":"10.1177/13558196231181081","DOIUrl":null,"url":null,"abstract":"<p><strong>Objectives: </strong>This article synthesizes the evidence on what have been called innovative domestic financing mechanisms for health (i.e. any domestic revenue-raising mechanism allowing governments to diversify away from traditional approaches such as general taxation, value-added tax, user fees or any type of health insurance) aimed at increasing fiscal space for health in African countries. The article seeks to answer the following questions: What types of domestic innovative financial mechanisms have been used to finance health care across Africa? How much additional revenue have these innovative financing mechanisms raised? Has the revenue raised through these mechanisms been, or was it meant to be, earmarked for health? What is known about the policy process associated with their design and implementation?</p><p><strong>Methods: </strong>A systematic review of the published and grey literature was conducted. The review focused on identifying articles providing quantitative information about the additional financial resources generated through innovative domestic financing mechanisms for health care in Africa, and/or qualitative information about the policy process associated with the design or effective implementation of these financing mechanisms.</p><p><strong>Results: </strong>The search led to an initial list of 4035 articles. Ultimately, 15 studies were selected for narrative analysis. A wide range of study methods were identified, from literature reviews to qualitative and quantitative analysis and case studies. The financing mechanisms implemented or planned for were varied, the most common being taxes on mobile phones, alcohol and money transfers. Few articles documented the revenue that could be raised through these mechanisms. For those that did, the revenue projected to be raised was relatively low, ranging from 0.01% of GDP for alcohol tax alone to 0.49% of GDP if multiple levies were applied. In any case, virtually none of the mechanisms have apparently been implemented. The articles revealed that, prior to implementation, the political acceptability, the readiness of institutions to adapt to the proposed reform and the potential distortionary impact these reforms may have on the targeted industry all require careful consideration. From a design perspective, the fundamental question of earmarking proved complex both politically and administratively, with very few mechanisms actually earmarked, thus questioning whether they could effectively fill part of the health-financing gap. Finally, ensuring that these mechanisms supported the underlying equity objectives of universal health coverage was recognized as important.</p><p><strong>Conclusions: </strong>Additional research is needed to understand better the potential of innovative domestic revenue generating mechanisms to fill the financing gap for health in Africa and diversify away from more traditional financing approaches. Whilst their revenue potential in absolute terms seems limited, they could represent an avenue for broader tax reforms in support of health. This will require sustained dialogue between Ministries of Health and Ministries of Finance.</p>","PeriodicalId":15953,"journal":{"name":"Journal of Health Services Research & Policy","volume":" ","pages":"132-140"},"PeriodicalIF":2.7000,"publicationDate":"2024-04-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10910821/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Health Services Research & Policy","FirstCategoryId":"3","ListUrlMain":"https://doi.org/10.1177/13558196231181081","RegionNum":4,"RegionCategory":"医学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/6/16 0:00:00","PubModel":"Epub","JCR":"Q3","JCRName":"HEALTH POLICY & SERVICES","Score":null,"Total":0}

引用次数: 0

Abstract

Objectives: This article synthesizes the evidence on what have been called innovative domestic financing mechanisms for health (i.e. any domestic revenue-raising mechanism allowing governments to diversify away from traditional approaches such as general taxation, value-added tax, user fees or any type of health insurance) aimed at increasing fiscal space for health in African countries. The article seeks to answer the following questions: What types of domestic innovative financial mechanisms have been used to finance health care across Africa? How much additional revenue have these innovative financing mechanisms raised? Has the revenue raised through these mechanisms been, or was it meant to be, earmarked for health? What is known about the policy process associated with their design and implementation?

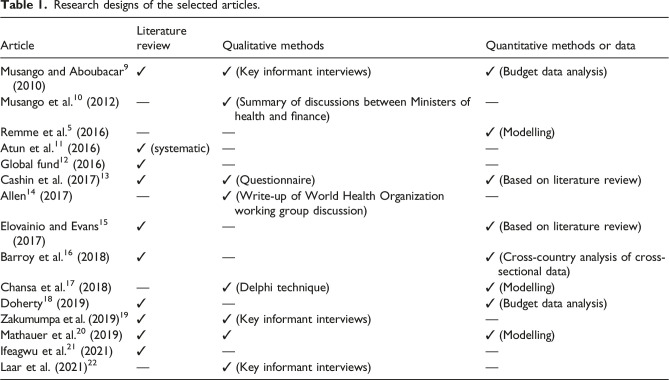

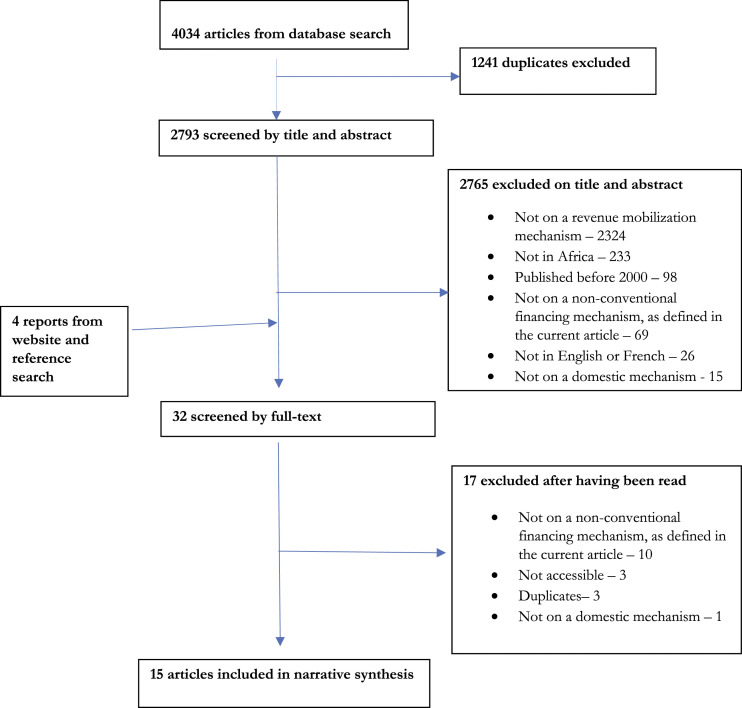

Methods: A systematic review of the published and grey literature was conducted. The review focused on identifying articles providing quantitative information about the additional financial resources generated through innovative domestic financing mechanisms for health care in Africa, and/or qualitative information about the policy process associated with the design or effective implementation of these financing mechanisms.

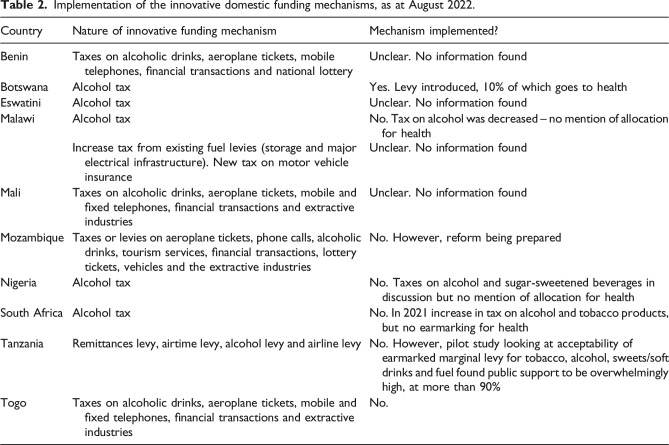

Results: The search led to an initial list of 4035 articles. Ultimately, 15 studies were selected for narrative analysis. A wide range of study methods were identified, from literature reviews to qualitative and quantitative analysis and case studies. The financing mechanisms implemented or planned for were varied, the most common being taxes on mobile phones, alcohol and money transfers. Few articles documented the revenue that could be raised through these mechanisms. For those that did, the revenue projected to be raised was relatively low, ranging from 0.01% of GDP for alcohol tax alone to 0.49% of GDP if multiple levies were applied. In any case, virtually none of the mechanisms have apparently been implemented. The articles revealed that, prior to implementation, the political acceptability, the readiness of institutions to adapt to the proposed reform and the potential distortionary impact these reforms may have on the targeted industry all require careful consideration. From a design perspective, the fundamental question of earmarking proved complex both politically and administratively, with very few mechanisms actually earmarked, thus questioning whether they could effectively fill part of the health-financing gap. Finally, ensuring that these mechanisms supported the underlying equity objectives of universal health coverage was recognized as important.

Conclusions: Additional research is needed to understand better the potential of innovative domestic revenue generating mechanisms to fill the financing gap for health in Africa and diversify away from more traditional financing approaches. Whilst their revenue potential in absolute terms seems limited, they could represent an avenue for broader tax reforms in support of health. This will require sustained dialogue between Ministries of Health and Ministries of Finance.

期刊介绍:

Journal of Health Services Research & Policy provides a unique opportunity to explore the ideas, policies and decisions shaping health services throughout the world. Edited and peer-reviewed by experts in the field and with a high academic standard and multidisciplinary approach, readers will gain a greater understanding of the current issues in healthcare policy and research. The journal"s strong international editorial advisory board also ensures that readers obtain a truly global and insightful perspective.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们