{"title":"Clustering of extreme values: estimation and application","authors":"Marta Ferreira","doi":"10.1007/s10182-023-00474-y","DOIUrl":null,"url":null,"abstract":"<div><p>The extreme value theory (EVT) encompasses a set of methods that allow inferring about the risk inherent to various phenomena in the scope of economic, financial, actuarial, environmental, hydrological, climatic sciences, as well as various areas of engineering. In many situations the clustering effect of high values may have an impact on the risk of occurrence of extreme phenomena. For example, extreme temperatures that last over time and result in drought situations, the permanence of intense rains leading to floods, stock markets in successive falls and consequent catastrophic losses. The extremal index is a measure of EVT associated with the degree of clustering of extreme values. In many situations, and under certain conditions, it corresponds to the arithmetic inverse of the average size of high-value clusters. The estimation of the extremal index generally entails two sources of uncertainty: the level at which high observations are considered and the identification of clusters. There are several contributions in the literature on the estimation of the extremal index, including methodologies to overcome the aforementioned sources of uncertainty. In this work we will revisit several existing estimators, apply automatic choice methods, both for the threshold and for the clustering parameter, and compare the performance of the methods. We will end with an application to meteorological data.</p></div>","PeriodicalId":55446,"journal":{"name":"Asta-Advances in Statistical Analysis","volume":"108 1","pages":"101 - 125"},"PeriodicalIF":1.4000,"publicationDate":"2023-03-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10064624/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asta-Advances in Statistical Analysis","FirstCategoryId":"100","ListUrlMain":"https://link.springer.com/article/10.1007/s10182-023-00474-y","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

引用次数: 0

Abstract

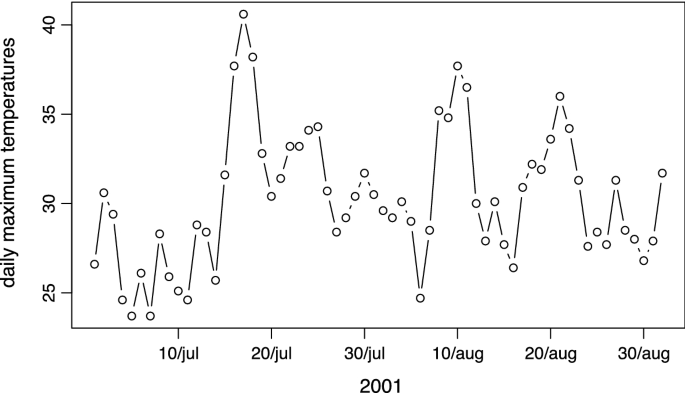

The extreme value theory (EVT) encompasses a set of methods that allow inferring about the risk inherent to various phenomena in the scope of economic, financial, actuarial, environmental, hydrological, climatic sciences, as well as various areas of engineering. In many situations the clustering effect of high values may have an impact on the risk of occurrence of extreme phenomena. For example, extreme temperatures that last over time and result in drought situations, the permanence of intense rains leading to floods, stock markets in successive falls and consequent catastrophic losses. The extremal index is a measure of EVT associated with the degree of clustering of extreme values. In many situations, and under certain conditions, it corresponds to the arithmetic inverse of the average size of high-value clusters. The estimation of the extremal index generally entails two sources of uncertainty: the level at which high observations are considered and the identification of clusters. There are several contributions in the literature on the estimation of the extremal index, including methodologies to overcome the aforementioned sources of uncertainty. In this work we will revisit several existing estimators, apply automatic choice methods, both for the threshold and for the clustering parameter, and compare the performance of the methods. We will end with an application to meteorological data.

期刊介绍:

AStA - Advances in Statistical Analysis, a journal of the German Statistical Society, is published quarterly and presents original contributions on statistical methods and applications and review articles.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们