{"title":"第一波COVID-19大流行对隐含股市波动的影响:使用谷歌趋势指标的国际证据","authors":"Stephanos Papadamou , Athanasios P. Fassas , Dimitris Kenourgios , Dimitrios Dimitriou","doi":"10.1016/j.jeca.2023.e00317","DOIUrl":null,"url":null,"abstract":"<div><p>This paper investigates the relationship between investors' attention, as measured by Google search queries, and equity implied volatility during the COVID-19 outbreak. Recent studies show that search investors' behavior data is an extremely abundant repository of predictive data, and investor-limited attention increases when the uncertainty level is high. Our study using data from thirteen countries across the globe during the first wave of the COVID-19 pandemic (January–April 2020) examines whether the search “topic and terms” for the pandemic affect market participants’ expectations about future realized volatility. With the panic and uncertainty about COVID-19, our empirical findings show that increased internet searches during the pandemic caused the information to flow into the financial markets at a faster rate and thus resulting in higher implied volatility directly and via the stock return-risk relation. More specifically for the latter, the leverage effect in the VIX becomes stronger as Google search queries intensify. Both the direct and indirect effects on implied volatility, highlight a risk-aversion channel that operates during the pandemic. We also find that these effects are stronger in Europe than in the rest of the world. Moreover, in a panel vector autoregression framework, we show that a positive shock on stock returns may soothe COVID-related Google searches in Europe. Our findings suggest that Google-based attention to COVID-19 leads to elevated risk aversion in stock markets.</p></div>","PeriodicalId":38259,"journal":{"name":"Journal of Economic Asymmetries","volume":"28 ","pages":"Article e00317"},"PeriodicalIF":0.0000,"publicationDate":"2023-06-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10258586/pdf/","citationCount":"1","resultStr":"{\"title\":\"Effects of the first wave of COVID-19 pandemic on implied stock market volatility: International evidence using a google trend measure\",\"authors\":\"Stephanos Papadamou , Athanasios P. Fassas , Dimitris Kenourgios , Dimitrios Dimitriou\",\"doi\":\"10.1016/j.jeca.2023.e00317\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This paper investigates the relationship between investors' attention, as measured by Google search queries, and equity implied volatility during the COVID-19 outbreak. Recent studies show that search investors' behavior data is an extremely abundant repository of predictive data, and investor-limited attention increases when the uncertainty level is high. Our study using data from thirteen countries across the globe during the first wave of the COVID-19 pandemic (January–April 2020) examines whether the search “topic and terms” for the pandemic affect market participants’ expectations about future realized volatility. With the panic and uncertainty about COVID-19, our empirical findings show that increased internet searches during the pandemic caused the information to flow into the financial markets at a faster rate and thus resulting in higher implied volatility directly and via the stock return-risk relation. More specifically for the latter, the leverage effect in the VIX becomes stronger as Google search queries intensify. Both the direct and indirect effects on implied volatility, highlight a risk-aversion channel that operates during the pandemic. We also find that these effects are stronger in Europe than in the rest of the world. Moreover, in a panel vector autoregression framework, we show that a positive shock on stock returns may soothe COVID-related Google searches in Europe. Our findings suggest that Google-based attention to COVID-19 leads to elevated risk aversion in stock markets.</p></div>\",\"PeriodicalId\":38259,\"journal\":{\"name\":\"Journal of Economic Asymmetries\",\"volume\":\"28 \",\"pages\":\"Article e00317\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-06-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10258586/pdf/\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Economic Asymmetries\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://www.sciencedirect.com/science/article/pii/S1703494923000294\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Economics, Econometrics and Finance\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Economic Asymmetries","FirstCategoryId":"1085","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S1703494923000294","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

Effects of the first wave of COVID-19 pandemic on implied stock market volatility: International evidence using a google trend measure

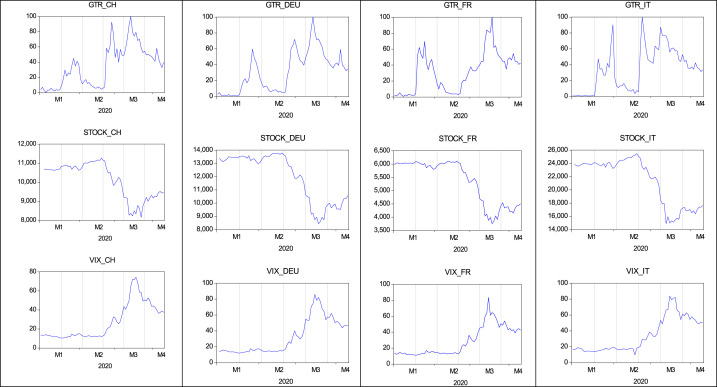

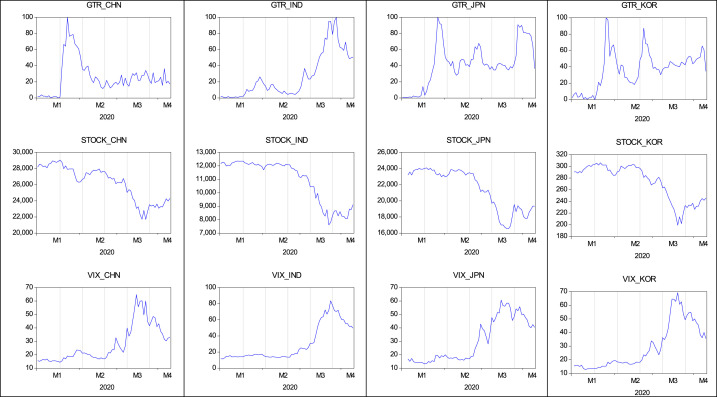

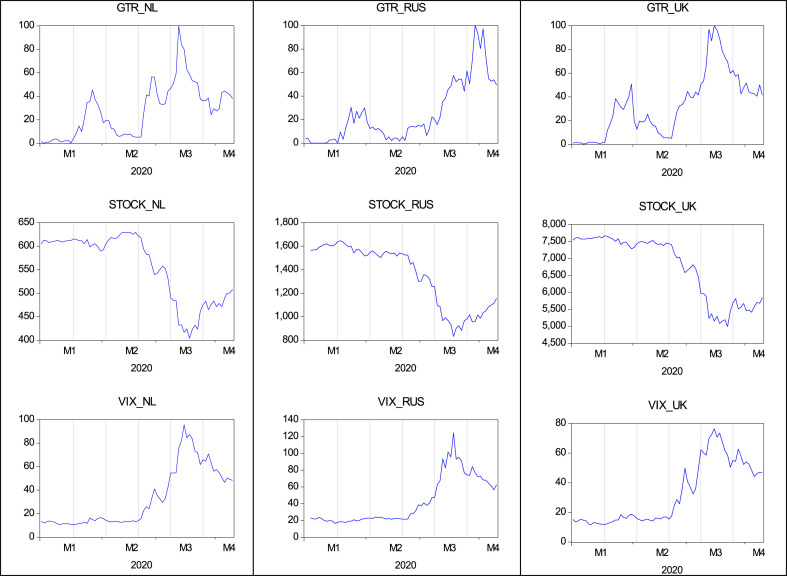

This paper investigates the relationship between investors' attention, as measured by Google search queries, and equity implied volatility during the COVID-19 outbreak. Recent studies show that search investors' behavior data is an extremely abundant repository of predictive data, and investor-limited attention increases when the uncertainty level is high. Our study using data from thirteen countries across the globe during the first wave of the COVID-19 pandemic (January–April 2020) examines whether the search “topic and terms” for the pandemic affect market participants’ expectations about future realized volatility. With the panic and uncertainty about COVID-19, our empirical findings show that increased internet searches during the pandemic caused the information to flow into the financial markets at a faster rate and thus resulting in higher implied volatility directly and via the stock return-risk relation. More specifically for the latter, the leverage effect in the VIX becomes stronger as Google search queries intensify. Both the direct and indirect effects on implied volatility, highlight a risk-aversion channel that operates during the pandemic. We also find that these effects are stronger in Europe than in the rest of the world. Moreover, in a panel vector autoregression framework, we show that a positive shock on stock returns may soothe COVID-related Google searches in Europe. Our findings suggest that Google-based attention to COVID-19 leads to elevated risk aversion in stock markets.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们