{"title":"基于期望值框架的点对点贷款组合数据驱动优化","authors":"Ajay Byanjankar, József Mezei, Markku Heikkilä","doi":"10.1002/isaf.1490","DOIUrl":null,"url":null,"abstract":"<p>In recent years, peer-to-peer (P2P) lending has been gaining popularity amongst borrowers and individual investors. This can mainly be attributed to the easy and quick access to loans and the higher possible returns. However, the risk involved in these investments is considerable, and for most investors, being nonprofessionals, this increases the complexity and the importance of investment decisions. In this study, we focus on generating optimal investment decisions to lenders for selecting loans. We treat the loan selection process in P2P lending as a portfolio optimization problem, with the aim being to select a set of loans that provide a required return while minimizing risk. In the process, we use internal rate of return as the measure of return. As the starting point of the model, we use machine-learning algorithms to predict the default probabilities and calculate expected values for the loans based on historical data. Afterwards, we calculate the distance between loans using (i) default probabilities and, as a novel step, (ii) expected value. In the calculations, we utilize kernel functions to obtain similarity weights of loans as the input of the optimization models. Two optimization models are tested and compared on data from the popular P2P platform Lending Club. The results show that using the expected-value framework yields higher return.</p>","PeriodicalId":53473,"journal":{"name":"Intelligent Systems in Accounting, Finance and Management","volume":"28 2","pages":"119-129"},"PeriodicalIF":3.7000,"publicationDate":"2021-03-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/isaf.1490","citationCount":"4","resultStr":"{\"title\":\"Data-driven optimization of peer-to-peer lending portfolios based on the expected value framework\",\"authors\":\"Ajay Byanjankar, József Mezei, Markku Heikkilä\",\"doi\":\"10.1002/isaf.1490\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In recent years, peer-to-peer (P2P) lending has been gaining popularity amongst borrowers and individual investors. This can mainly be attributed to the easy and quick access to loans and the higher possible returns. However, the risk involved in these investments is considerable, and for most investors, being nonprofessionals, this increases the complexity and the importance of investment decisions. In this study, we focus on generating optimal investment decisions to lenders for selecting loans. We treat the loan selection process in P2P lending as a portfolio optimization problem, with the aim being to select a set of loans that provide a required return while minimizing risk. In the process, we use internal rate of return as the measure of return. As the starting point of the model, we use machine-learning algorithms to predict the default probabilities and calculate expected values for the loans based on historical data. Afterwards, we calculate the distance between loans using (i) default probabilities and, as a novel step, (ii) expected value. In the calculations, we utilize kernel functions to obtain similarity weights of loans as the input of the optimization models. Two optimization models are tested and compared on data from the popular P2P platform Lending Club. The results show that using the expected-value framework yields higher return.</p>\",\"PeriodicalId\":53473,\"journal\":{\"name\":\"Intelligent Systems in Accounting, Finance and Management\",\"volume\":\"28 2\",\"pages\":\"119-129\"},\"PeriodicalIF\":3.7000,\"publicationDate\":\"2021-03-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1002/isaf.1490\",\"citationCount\":\"4\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Intelligent Systems in Accounting, Finance and Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1490\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Economics, Econometrics and Finance\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems in Accounting, Finance and Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1490","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

Data-driven optimization of peer-to-peer lending portfolios based on the expected value framework

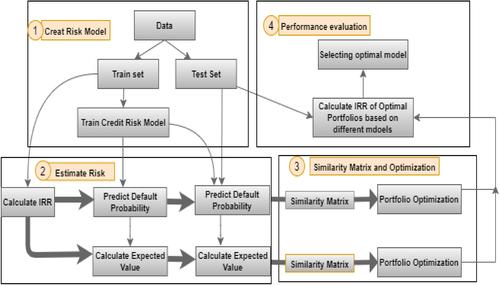

In recent years, peer-to-peer (P2P) lending has been gaining popularity amongst borrowers and individual investors. This can mainly be attributed to the easy and quick access to loans and the higher possible returns. However, the risk involved in these investments is considerable, and for most investors, being nonprofessionals, this increases the complexity and the importance of investment decisions. In this study, we focus on generating optimal investment decisions to lenders for selecting loans. We treat the loan selection process in P2P lending as a portfolio optimization problem, with the aim being to select a set of loans that provide a required return while minimizing risk. In the process, we use internal rate of return as the measure of return. As the starting point of the model, we use machine-learning algorithms to predict the default probabilities and calculate expected values for the loans based on historical data. Afterwards, we calculate the distance between loans using (i) default probabilities and, as a novel step, (ii) expected value. In the calculations, we utilize kernel functions to obtain similarity weights of loans as the input of the optimization models. Two optimization models are tested and compared on data from the popular P2P platform Lending Club. The results show that using the expected-value framework yields higher return.

期刊介绍:

Intelligent Systems in Accounting, Finance and Management is a quarterly international journal which publishes original, high quality material dealing with all aspects of intelligent systems as they relate to the fields of accounting, economics, finance, marketing and management. In addition, the journal also is concerned with related emerging technologies, including big data, business intelligence, social media and other technologies. It encourages the development of novel technologies, and the embedding of new and existing technologies into applications of real, practical value. Therefore, implementation issues are of as much concern as development issues. The journal is designed to appeal to academics in the intelligent systems, emerging technologies and business fields, as well as to advanced practitioners who wish to improve the effectiveness, efficiency, or economy of their working practices. A special feature of the journal is the use of two groups of reviewers, those who specialize in intelligent systems work, and also those who specialize in applications areas. Reviewers are asked to address issues of originality and actual or potential impact on research, teaching, or practice in the accounting, finance, or management fields. Authors working on conceptual developments or on laboratory-based explorations of data sets therefore need to address the issue of potential impact at some level in submissions to the journal.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们