{"title":"在方向变化方法下测量高频数据的相对波动性","authors":"Shengnan Li, Edward P. K. Tsang, John O'Hara","doi":"10.1002/isaf.1510","DOIUrl":null,"url":null,"abstract":"<p>We introduce a new approach in measuring relative volatility between two markets based on the directional change (DC) method. DC is a data-driven approach for sampling financial market data such that the data are recorded when the price changes have reached a significant amplitude rather than recording data under a predetermined timescale. Under the DC framework, we propose a new concept of DC micro-market relative volatility to evaluate relative volatility between two markets. Unlike the time-series method, micro-market relative volatility redefines the timescale based on the frequency of the observed DC data between the two markets. We show that it is useful for measuring the relative volatility in micro-market activities (high-frequency data).</p>","PeriodicalId":53473,"journal":{"name":"Intelligent Systems in Accounting, Finance and Management","volume":"29 2","pages":"86-102"},"PeriodicalIF":3.7000,"publicationDate":"2022-06-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/isaf.1510","citationCount":"1","resultStr":"{\"title\":\"Measuring relative volatility in high-frequency data under the directional change approach\",\"authors\":\"Shengnan Li, Edward P. K. Tsang, John O'Hara\",\"doi\":\"10.1002/isaf.1510\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We introduce a new approach in measuring relative volatility between two markets based on the directional change (DC) method. DC is a data-driven approach for sampling financial market data such that the data are recorded when the price changes have reached a significant amplitude rather than recording data under a predetermined timescale. Under the DC framework, we propose a new concept of DC micro-market relative volatility to evaluate relative volatility between two markets. Unlike the time-series method, micro-market relative volatility redefines the timescale based on the frequency of the observed DC data between the two markets. We show that it is useful for measuring the relative volatility in micro-market activities (high-frequency data).</p>\",\"PeriodicalId\":53473,\"journal\":{\"name\":\"Intelligent Systems in Accounting, Finance and Management\",\"volume\":\"29 2\",\"pages\":\"86-102\"},\"PeriodicalIF\":3.7000,\"publicationDate\":\"2022-06-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/isaf.1510\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Intelligent Systems in Accounting, Finance and Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1510\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Economics, Econometrics and Finance\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Intelligent Systems in Accounting, Finance and Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/isaf.1510","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Economics, Econometrics and Finance","Score":null,"Total":0}

Measuring relative volatility in high-frequency data under the directional change approach

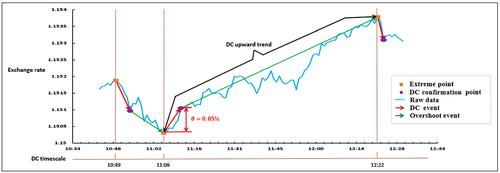

We introduce a new approach in measuring relative volatility between two markets based on the directional change (DC) method. DC is a data-driven approach for sampling financial market data such that the data are recorded when the price changes have reached a significant amplitude rather than recording data under a predetermined timescale. Under the DC framework, we propose a new concept of DC micro-market relative volatility to evaluate relative volatility between two markets. Unlike the time-series method, micro-market relative volatility redefines the timescale based on the frequency of the observed DC data between the two markets. We show that it is useful for measuring the relative volatility in micro-market activities (high-frequency data).

期刊介绍:

Intelligent Systems in Accounting, Finance and Management is a quarterly international journal which publishes original, high quality material dealing with all aspects of intelligent systems as they relate to the fields of accounting, economics, finance, marketing and management. In addition, the journal also is concerned with related emerging technologies, including big data, business intelligence, social media and other technologies. It encourages the development of novel technologies, and the embedding of new and existing technologies into applications of real, practical value. Therefore, implementation issues are of as much concern as development issues. The journal is designed to appeal to academics in the intelligent systems, emerging technologies and business fields, as well as to advanced practitioners who wish to improve the effectiveness, efficiency, or economy of their working practices. A special feature of the journal is the use of two groups of reviewers, those who specialize in intelligent systems work, and also those who specialize in applications areas. Reviewers are asked to address issues of originality and actual or potential impact on research, teaching, or practice in the accounting, finance, or management fields. Authors working on conceptual developments or on laboratory-based explorations of data sets therefore need to address the issue of potential impact at some level in submissions to the journal.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们