{"title":"昨天已成为历史,明天还是个谜:董事和首席执行官之前的破产经历及其当前公司的财务风险","authors":"Mariya N. Ivanova, Henrik Nilsson, Milda Tylaite","doi":"10.1111/jbfa.12736","DOIUrl":null,"url":null,"abstract":"<p>Using a large sample of Swedish private firms, we investigate the link between the prior corporate bankruptcy experiences (BEs) of directors and CEOs and the financial risk of their current firms. We find that firms with directors and CEOs previously involved in bankruptcies exhibit more aggressive corporate financial policies, have a higher corporate bankruptcy risk and are subject to a higher cost of debt. Our findings align with an innate characteristics explanation: corporate BEs and current corporate risk-taking reflect personal risk preferences. Furthermore, while we find evidence of income losses for CEOs and directors involved in bankruptcies, such losses are transient, potentially explaining the risk-taking behavior after experiencing bankruptcy. Overall, our results suggest that the presence of individuals with prior BE can be considered a signal of higher financial risk for their firms. This insight is relevant to regulators, lenders and corporate decision-makers.</p>","PeriodicalId":48106,"journal":{"name":"Journal of Business Finance & Accounting","volume":"51 1-2","pages":"595-630"},"PeriodicalIF":2.4000,"publicationDate":"2023-06-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12736","citationCount":"0","resultStr":"{\"title\":\"Yesterday is history, tomorrow is a mystery: Directors’ and CEOs’ prior bankruptcy experiences and the financial risk of their current firms\",\"authors\":\"Mariya N. Ivanova, Henrik Nilsson, Milda Tylaite\",\"doi\":\"10.1111/jbfa.12736\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Using a large sample of Swedish private firms, we investigate the link between the prior corporate bankruptcy experiences (BEs) of directors and CEOs and the financial risk of their current firms. We find that firms with directors and CEOs previously involved in bankruptcies exhibit more aggressive corporate financial policies, have a higher corporate bankruptcy risk and are subject to a higher cost of debt. Our findings align with an innate characteristics explanation: corporate BEs and current corporate risk-taking reflect personal risk preferences. Furthermore, while we find evidence of income losses for CEOs and directors involved in bankruptcies, such losses are transient, potentially explaining the risk-taking behavior after experiencing bankruptcy. Overall, our results suggest that the presence of individuals with prior BE can be considered a signal of higher financial risk for their firms. This insight is relevant to regulators, lenders and corporate decision-makers.</p>\",\"PeriodicalId\":48106,\"journal\":{\"name\":\"Journal of Business Finance & Accounting\",\"volume\":\"51 1-2\",\"pages\":\"595-630\"},\"PeriodicalIF\":2.4000,\"publicationDate\":\"2023-06-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12736\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Business Finance & Accounting\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12736\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Business Finance & Accounting","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12736","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Yesterday is history, tomorrow is a mystery: Directors’ and CEOs’ prior bankruptcy experiences and the financial risk of their current firms

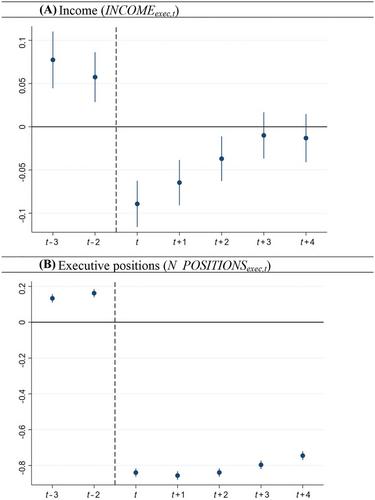

Using a large sample of Swedish private firms, we investigate the link between the prior corporate bankruptcy experiences (BEs) of directors and CEOs and the financial risk of their current firms. We find that firms with directors and CEOs previously involved in bankruptcies exhibit more aggressive corporate financial policies, have a higher corporate bankruptcy risk and are subject to a higher cost of debt. Our findings align with an innate characteristics explanation: corporate BEs and current corporate risk-taking reflect personal risk preferences. Furthermore, while we find evidence of income losses for CEOs and directors involved in bankruptcies, such losses are transient, potentially explaining the risk-taking behavior after experiencing bankruptcy. Overall, our results suggest that the presence of individuals with prior BE can be considered a signal of higher financial risk for their firms. This insight is relevant to regulators, lenders and corporate decision-makers.

期刊介绍:

Journal of Business Finance and Accounting exists to publish high quality research papers in accounting, corporate finance, corporate governance and their interfaces. The interfaces are relevant in many areas such as financial reporting and communication, valuation, financial performance measurement and managerial reward and control structures. A feature of JBFA is that it recognises that informational problems are pervasive in financial markets and business organisations, and that accounting plays an important role in resolving such problems. JBFA welcomes both theoretical and empirical contributions. Nonetheless, theoretical papers should yield novel testable implications, and empirical papers should be theoretically well-motivated. The Editors view accounting and finance as being closely related to economics and, as a consequence, papers submitted will often have theoretical motivations that are grounded in economics. JBFA, however, also seeks papers that complement economics-based theorising with theoretical developments originating in other social science disciplines or traditions. While many papers in JBFA use econometric or related empirical methods, the Editors also welcome contributions that use other empirical research methods. Although the scope of JBFA is broad, it is not a suitable outlet for highly abstract mathematical papers, or empirical papers with inadequate theoretical motivation. Also, papers that study asset pricing, or the operations of financial markets, should have direct implications for one or more of preparers, regulators, users of financial statements, and corporate financial decision makers, or at least should have implications for the development of future research relevant to such users.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们