{"title":"太复杂难以消化?联邦税单及其在美国金融市场的处理","authors":"Hamza Bennani, Matthias Neuenkirch","doi":"10.1007/s10797-023-09795-9","DOIUrl":null,"url":null,"abstract":"Abstract In this paper, we analyze whether the textual complexity of tax bills affects financial markets. Based on the Flesch-Kincaid grade level of the 32 tax bills identified by Romer (Am Econ Rev 100(3):763–801, 2010)in the period 1962–2003, we assess the relationship between tax bills’ textual complexity and financial markets in various windows around the signing of a bill. Our results show a negative (positive) and significant relationship between the present value of tax bills and changes in the 10-year government bond yields (S &P 500 returns). The magnitude of this relationship increases over time, suggesting that market participants underreact at first and need a couple of days to digest the information contained in the tax bills. This delay can be explained by the textual characteristics of the bills in the case of the 10-year yields as a lower readability partly counteracts the negative relationship for up to three days after the signing of a tax bill. In the case of the stock market, we find similar evidence, but only for a part of the readability measures employed in this paper.","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"13 1","pages":"0"},"PeriodicalIF":1.0000,"publicationDate":"2023-08-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Too complex to digest? Federal tax bills and their processing in US financial markets\",\"authors\":\"Hamza Bennani, Matthias Neuenkirch\",\"doi\":\"10.1007/s10797-023-09795-9\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract In this paper, we analyze whether the textual complexity of tax bills affects financial markets. Based on the Flesch-Kincaid grade level of the 32 tax bills identified by Romer (Am Econ Rev 100(3):763–801, 2010)in the period 1962–2003, we assess the relationship between tax bills’ textual complexity and financial markets in various windows around the signing of a bill. Our results show a negative (positive) and significant relationship between the present value of tax bills and changes in the 10-year government bond yields (S &P 500 returns). The magnitude of this relationship increases over time, suggesting that market participants underreact at first and need a couple of days to digest the information contained in the tax bills. This delay can be explained by the textual characteristics of the bills in the case of the 10-year yields as a lower readability partly counteracts the negative relationship for up to three days after the signing of a tax bill. In the case of the stock market, we find similar evidence, but only for a part of the readability measures employed in this paper.\",\"PeriodicalId\":47518,\"journal\":{\"name\":\"International Tax and Public Finance\",\"volume\":\"13 1\",\"pages\":\"0\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-08-15\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Tax and Public Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s10797-023-09795-9\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s10797-023-09795-9","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Too complex to digest? Federal tax bills and their processing in US financial markets

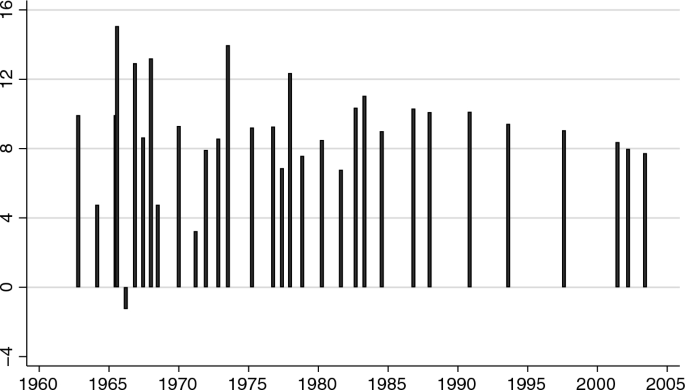

Abstract In this paper, we analyze whether the textual complexity of tax bills affects financial markets. Based on the Flesch-Kincaid grade level of the 32 tax bills identified by Romer (Am Econ Rev 100(3):763–801, 2010)in the period 1962–2003, we assess the relationship between tax bills’ textual complexity and financial markets in various windows around the signing of a bill. Our results show a negative (positive) and significant relationship between the present value of tax bills and changes in the 10-year government bond yields (S &P 500 returns). The magnitude of this relationship increases over time, suggesting that market participants underreact at first and need a couple of days to digest the information contained in the tax bills. This delay can be explained by the textual characteristics of the bills in the case of the 10-year yields as a lower readability partly counteracts the negative relationship for up to three days after the signing of a tax bill. In the case of the stock market, we find similar evidence, but only for a part of the readability measures employed in this paper.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们