{"title":"在预测未来现金流方面,盈余比现金流更好吗?来自苹果与苹果比较的证据","authors":"Ryan J. Casey, George W. Ruch","doi":"10.1007/s11142-023-09805-5","DOIUrl":null,"url":null,"abstract":"We compare the abilities of earnings and cash flows to predict future cash flows. We take a novel approach in that we perform apples-to-apples comparisons of five earnings components measured on an accrual basis with their equivalents measured on a cash basis. On the one hand, we find that the operating profit component (sales net of cost of goods sold and SG&A expense) outperforms its cash-basis equivalent in predicting future cash flows. On the other hand, we find that the depreciation expense and non-operating income components underperform their cash-basis equivalents in predicting future cash flows. Additionally, we fail to find significant differences between the predictive abilities of the interest expense and income tax expense components and their cash-basis equivalents. The inconsistent findings across earnings components suggest that unequivocal all-or-nothing conclusions on the relative predictive abilities of earnings and cash flows are unwarranted.","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"13 1","pages":"0"},"PeriodicalIF":5.8000,"publicationDate":"2023-10-09","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"1","resultStr":"{\"title\":\"Are earnings better than cash flows at predicting future cash flows? Evidence from apples-to-apples comparisons\",\"authors\":\"Ryan J. Casey, George W. Ruch\",\"doi\":\"10.1007/s11142-023-09805-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"We compare the abilities of earnings and cash flows to predict future cash flows. We take a novel approach in that we perform apples-to-apples comparisons of five earnings components measured on an accrual basis with their equivalents measured on a cash basis. On the one hand, we find that the operating profit component (sales net of cost of goods sold and SG&A expense) outperforms its cash-basis equivalent in predicting future cash flows. On the other hand, we find that the depreciation expense and non-operating income components underperform their cash-basis equivalents in predicting future cash flows. Additionally, we fail to find significant differences between the predictive abilities of the interest expense and income tax expense components and their cash-basis equivalents. The inconsistent findings across earnings components suggest that unequivocal all-or-nothing conclusions on the relative predictive abilities of earnings and cash flows are unwarranted.\",\"PeriodicalId\":48120,\"journal\":{\"name\":\"Review of Accounting Studies\",\"volume\":\"13 1\",\"pages\":\"0\"},\"PeriodicalIF\":5.8000,\"publicationDate\":\"2023-10-09\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Accounting Studies\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11142-023-09805-5\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11142-023-09805-5","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Are earnings better than cash flows at predicting future cash flows? Evidence from apples-to-apples comparisons

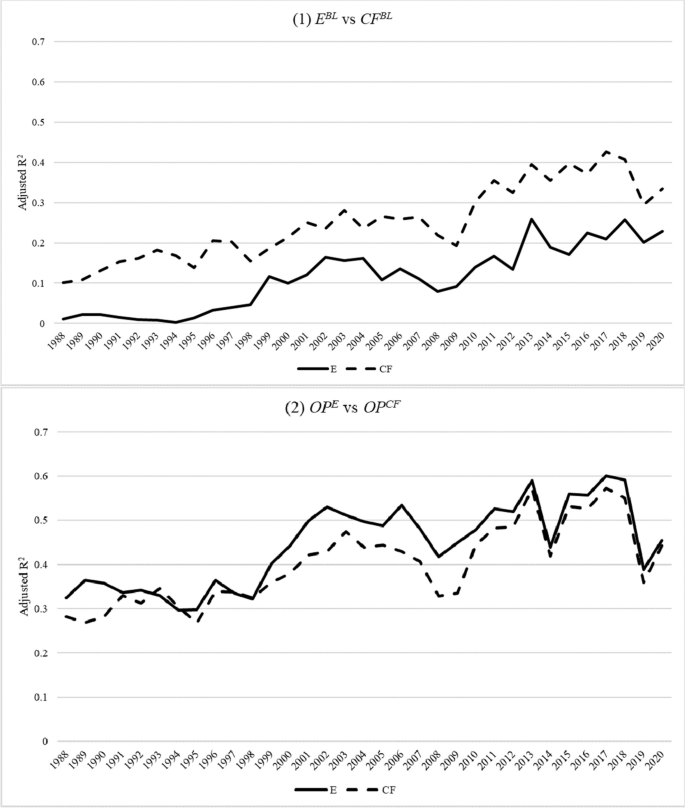

We compare the abilities of earnings and cash flows to predict future cash flows. We take a novel approach in that we perform apples-to-apples comparisons of five earnings components measured on an accrual basis with their equivalents measured on a cash basis. On the one hand, we find that the operating profit component (sales net of cost of goods sold and SG&A expense) outperforms its cash-basis equivalent in predicting future cash flows. On the other hand, we find that the depreciation expense and non-operating income components underperform their cash-basis equivalents in predicting future cash flows. Additionally, we fail to find significant differences between the predictive abilities of the interest expense and income tax expense components and their cash-basis equivalents. The inconsistent findings across earnings components suggest that unequivocal all-or-nothing conclusions on the relative predictive abilities of earnings and cash flows are unwarranted.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们