{"title":"抵押框架:流动性溢价和多重均衡","authors":"YVAN LENGWILER, ATHANASIOS ORPHANIDES","doi":"10.1111/jmcb.13048","DOIUrl":null,"url":null,"abstract":"<p>Central banks normally accept debt of their own governments as collateral in liquidity operations without reservations. This gives rise to a valuable liquidity premium that reduces the cost of government finance. The ECB is an interesting exception in this respect. It relies on external assessments of the creditworthiness of its member states, such as credit ratings, to determine eligibility and the haircut it imposes on such debt. We show how such features in a central bank's collateral framework can give rise to cliff effects and multiple equilibria in bond yields and increase the vulnerability of governments to external shocks. This policy can potentially induce sovereign debt crises and defaults that would not otherwise occur. The success of the ECB's temporary suspension of these features of its collateral framework during the pandemic illustrates the practical relevance of this mechanism.</p>","PeriodicalId":48328,"journal":{"name":"Journal of Money Credit and Banking","volume":"56 2-3","pages":"489-516"},"PeriodicalIF":1.6000,"publicationDate":"2023-05-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jmcb.13048","citationCount":"0","resultStr":"{\"title\":\"Collateral Framework: Liquidity Premia and Multiple Equilibria\",\"authors\":\"YVAN LENGWILER, ATHANASIOS ORPHANIDES\",\"doi\":\"10.1111/jmcb.13048\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Central banks normally accept debt of their own governments as collateral in liquidity operations without reservations. This gives rise to a valuable liquidity premium that reduces the cost of government finance. The ECB is an interesting exception in this respect. It relies on external assessments of the creditworthiness of its member states, such as credit ratings, to determine eligibility and the haircut it imposes on such debt. We show how such features in a central bank's collateral framework can give rise to cliff effects and multiple equilibria in bond yields and increase the vulnerability of governments to external shocks. This policy can potentially induce sovereign debt crises and defaults that would not otherwise occur. The success of the ECB's temporary suspension of these features of its collateral framework during the pandemic illustrates the practical relevance of this mechanism.</p>\",\"PeriodicalId\":48328,\"journal\":{\"name\":\"Journal of Money Credit and Banking\",\"volume\":\"56 2-3\",\"pages\":\"489-516\"},\"PeriodicalIF\":1.6000,\"publicationDate\":\"2023-05-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jmcb.13048\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Money Credit and Banking\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jmcb.13048\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Money Credit and Banking","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jmcb.13048","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Collateral Framework: Liquidity Premia and Multiple Equilibria

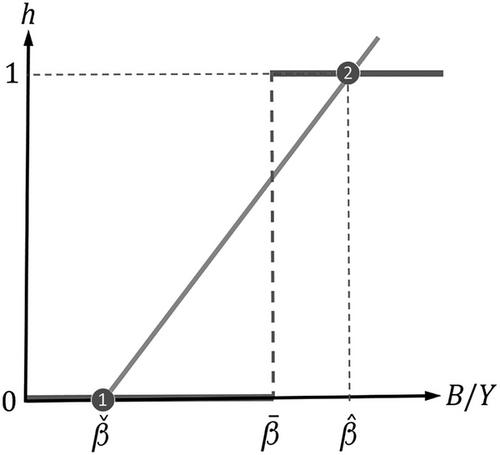

Central banks normally accept debt of their own governments as collateral in liquidity operations without reservations. This gives rise to a valuable liquidity premium that reduces the cost of government finance. The ECB is an interesting exception in this respect. It relies on external assessments of the creditworthiness of its member states, such as credit ratings, to determine eligibility and the haircut it imposes on such debt. We show how such features in a central bank's collateral framework can give rise to cliff effects and multiple equilibria in bond yields and increase the vulnerability of governments to external shocks. This policy can potentially induce sovereign debt crises and defaults that would not otherwise occur. The success of the ECB's temporary suspension of these features of its collateral framework during the pandemic illustrates the practical relevance of this mechanism.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们