{"title":"通过与保险挂钩的证券减轻野火损失:建模和风险管理视角","authors":"Hong Li, Jianxi Su","doi":"10.1111/jori.12449","DOIUrl":null,"url":null,"abstract":"<p>This paper investigates the use of catastrophe (CAT) bonds as a risk management tool for wildfires. We introduce a set of Bayesian dynamic models designed to accurately represent wildfire losses, allowing a thorough examination of wildfire CAT bond pricing and hedge effectiveness. Our model captures crucial attributes of wildfire data, such as zero inflation, overdispersion, temporal fluctuations, and spatial dependence. Employing extensive quantitative analyses of US wildfire data, we highlight that CAT bonds can substantially mitigate tail risk associated with insurers' liability. Importantly, index-based CAT bonds, drawing their payouts from aggregate wildfire losses over a larger geographical scope than an insurer's operational area, also provide effective hedges. Our research underscores the potential of wildfire CAT bonds as an enhancement to traditional reinsurance strategies, offering insurers an improved means to manage and mitigate wildfire exposures amidst inherent uncertainties.</p>","PeriodicalId":51440,"journal":{"name":"Journal of Risk and Insurance","volume":"91 2","pages":"383-414"},"PeriodicalIF":1.7000,"publicationDate":"2023-09-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jori.12449","citationCount":"0","resultStr":"{\"title\":\"Mitigating wildfire losses via insurance-linked securities: Modeling and risk management perspectives\",\"authors\":\"Hong Li, Jianxi Su\",\"doi\":\"10.1111/jori.12449\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper investigates the use of catastrophe (CAT) bonds as a risk management tool for wildfires. We introduce a set of Bayesian dynamic models designed to accurately represent wildfire losses, allowing a thorough examination of wildfire CAT bond pricing and hedge effectiveness. Our model captures crucial attributes of wildfire data, such as zero inflation, overdispersion, temporal fluctuations, and spatial dependence. Employing extensive quantitative analyses of US wildfire data, we highlight that CAT bonds can substantially mitigate tail risk associated with insurers' liability. Importantly, index-based CAT bonds, drawing their payouts from aggregate wildfire losses over a larger geographical scope than an insurer's operational area, also provide effective hedges. Our research underscores the potential of wildfire CAT bonds as an enhancement to traditional reinsurance strategies, offering insurers an improved means to manage and mitigate wildfire exposures amidst inherent uncertainties.</p>\",\"PeriodicalId\":51440,\"journal\":{\"name\":\"Journal of Risk and Insurance\",\"volume\":\"91 2\",\"pages\":\"383-414\"},\"PeriodicalIF\":1.7000,\"publicationDate\":\"2023-09-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jori.12449\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Risk and Insurance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jori.12449\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Risk and Insurance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jori.12449","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Mitigating wildfire losses via insurance-linked securities: Modeling and risk management perspectives

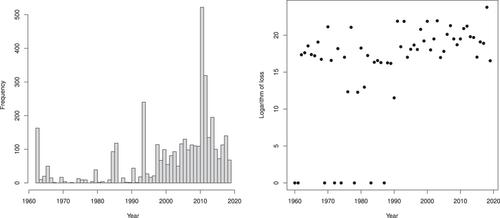

This paper investigates the use of catastrophe (CAT) bonds as a risk management tool for wildfires. We introduce a set of Bayesian dynamic models designed to accurately represent wildfire losses, allowing a thorough examination of wildfire CAT bond pricing and hedge effectiveness. Our model captures crucial attributes of wildfire data, such as zero inflation, overdispersion, temporal fluctuations, and spatial dependence. Employing extensive quantitative analyses of US wildfire data, we highlight that CAT bonds can substantially mitigate tail risk associated with insurers' liability. Importantly, index-based CAT bonds, drawing their payouts from aggregate wildfire losses over a larger geographical scope than an insurer's operational area, also provide effective hedges. Our research underscores the potential of wildfire CAT bonds as an enhancement to traditional reinsurance strategies, offering insurers an improved means to manage and mitigate wildfire exposures amidst inherent uncertainties.

期刊介绍:

The Journal of Risk and Insurance (JRI) is the premier outlet for theoretical and empirical research on the topics of insurance economics and risk management. Research in the JRI informs practice, policy-making, and regulation in insurance markets as well as corporate and household risk management. JRI is the flagship journal for the American Risk and Insurance Association, and is currently indexed by the American Economic Association’s Economic Literature Index, RePEc, the Social Sciences Citation Index, and others. Issues of the Journal of Risk and Insurance, from volume one to volume 82 (2015), are available online through JSTOR . Recent issues of JRI are available through Wiley Online Library. In addition to the research areas of traditional strength for the JRI, the editorial team highlights below specific areas for special focus in the near term, due to their current relevance for the field.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们