{"title":"首席审计师的指示如何影响组成部分审计师的证据收集决策?解释性说明和责任的共同影响","authors":"Skye Zhu, Soon-Yeow Phang","doi":"10.1111/1911-3846.12911","DOIUrl":null,"url":null,"abstract":"<p>Regulators have raised concerns about the quality of component auditors' work. Of particular concern is that component auditors often do not adequately perform procedures and gather enough quality evidence. This failure is likely caused by component auditors' different interpretations of lead auditor instructions and by their lack of responsibility. Our interview findings suggest that component auditors tend to interpret lead auditor instructions concretely because they often receive detailed instructions from lead auditors. We propose that a responsibility prompt reminding component auditors to be aware of their obligations to the group audit engagement can improve their evidence collection. In two experiments, we find that our proposed responsibility prompt can effectively improve component auditors' evidence collection decisions and that this finding holds across different cultural settings. Our third experiment provides evidence that a responsibility prompt improves component auditors' evidence collection when provided to auditors who receive instructions that prime low-level (but not high-level) construals. Overall, our findings suggest that prompting component auditors to internalize the responsibility of a group audit engagement is a viable way to improve the quality of group audits.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"41 1","pages":"591-619"},"PeriodicalIF":3.8000,"publicationDate":"2023-10-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12911","citationCount":"0","resultStr":"{\"title\":\"How do lead auditor instructions influence component auditors' evidence collection decisions? The joint influence of construal interpretations and responsibility\",\"authors\":\"Skye Zhu, Soon-Yeow Phang\",\"doi\":\"10.1111/1911-3846.12911\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Regulators have raised concerns about the quality of component auditors' work. Of particular concern is that component auditors often do not adequately perform procedures and gather enough quality evidence. This failure is likely caused by component auditors' different interpretations of lead auditor instructions and by their lack of responsibility. Our interview findings suggest that component auditors tend to interpret lead auditor instructions concretely because they often receive detailed instructions from lead auditors. We propose that a responsibility prompt reminding component auditors to be aware of their obligations to the group audit engagement can improve their evidence collection. In two experiments, we find that our proposed responsibility prompt can effectively improve component auditors' evidence collection decisions and that this finding holds across different cultural settings. Our third experiment provides evidence that a responsibility prompt improves component auditors' evidence collection when provided to auditors who receive instructions that prime low-level (but not high-level) construals. Overall, our findings suggest that prompting component auditors to internalize the responsibility of a group audit engagement is a viable way to improve the quality of group audits.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"41 1\",\"pages\":\"591-619\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2023-10-14\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12911\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12911\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12911","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

How do lead auditor instructions influence component auditors' evidence collection decisions? The joint influence of construal interpretations and responsibility

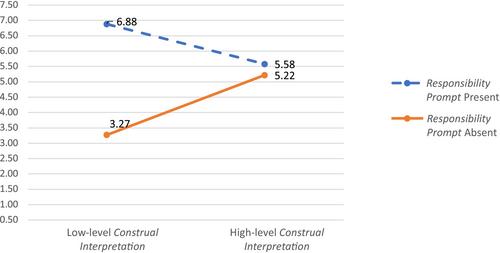

Regulators have raised concerns about the quality of component auditors' work. Of particular concern is that component auditors often do not adequately perform procedures and gather enough quality evidence. This failure is likely caused by component auditors' different interpretations of lead auditor instructions and by their lack of responsibility. Our interview findings suggest that component auditors tend to interpret lead auditor instructions concretely because they often receive detailed instructions from lead auditors. We propose that a responsibility prompt reminding component auditors to be aware of their obligations to the group audit engagement can improve their evidence collection. In two experiments, we find that our proposed responsibility prompt can effectively improve component auditors' evidence collection decisions and that this finding holds across different cultural settings. Our third experiment provides evidence that a responsibility prompt improves component auditors' evidence collection when provided to auditors who receive instructions that prime low-level (but not high-level) construals. Overall, our findings suggest that prompting component auditors to internalize the responsibility of a group audit engagement is a viable way to improve the quality of group audits.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们