{"title":"流数据存在下预测随机规划的无分布算法","authors":"Shuotao Diao, Suvrajeet Sen","doi":"10.1007/s10589-023-00529-5","DOIUrl":null,"url":null,"abstract":"Abstract This paper studies a fusion of concepts from stochastic programming and non-parametric statistical learning in which data is available in the form of covariates interpreted as predictors and responses. Such models are designed to impart greater agility, allowing decisions under uncertainty to adapt to the knowledge of predictors (leading indicators). This paper studies two classes of methods for such joint prediction-optimization models. One of the methods may be classified as a first-order method, whereas the other studies piecewise linear approximations. Both of these methods are based on coupling non-parametric estimation for predictive purposes, and optimization for decision-making within one unified framework. In addition, our study incorporates several non-parametric estimation schemes, including k nearest neighbors ( k NN) and other standard kernel estimators. Our computational results demonstrate that the new algorithms proposed in this paper outperform traditional approaches which were not designed for streaming data applications requiring simultaneous estimation and optimization as important design features for such algorithms. For instance, coupling k NN with Stochastic Decomposition (SD) turns out to be over 40 times faster than an online version of Benders Decomposition while finding decisions of similar quality. Such computational results motivate a paradigm shift in optimization algorithms that are intended for modern streaming applications.","PeriodicalId":55227,"journal":{"name":"Computational Optimization and Applications","volume":"2015 1","pages":"0"},"PeriodicalIF":2.0000,"publicationDate":"2023-09-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Distribution-free algorithms for predictive stochastic programming in the presence of streaming data\",\"authors\":\"Shuotao Diao, Suvrajeet Sen\",\"doi\":\"10.1007/s10589-023-00529-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract This paper studies a fusion of concepts from stochastic programming and non-parametric statistical learning in which data is available in the form of covariates interpreted as predictors and responses. Such models are designed to impart greater agility, allowing decisions under uncertainty to adapt to the knowledge of predictors (leading indicators). This paper studies two classes of methods for such joint prediction-optimization models. One of the methods may be classified as a first-order method, whereas the other studies piecewise linear approximations. Both of these methods are based on coupling non-parametric estimation for predictive purposes, and optimization for decision-making within one unified framework. In addition, our study incorporates several non-parametric estimation schemes, including k nearest neighbors ( k NN) and other standard kernel estimators. Our computational results demonstrate that the new algorithms proposed in this paper outperform traditional approaches which were not designed for streaming data applications requiring simultaneous estimation and optimization as important design features for such algorithms. For instance, coupling k NN with Stochastic Decomposition (SD) turns out to be over 40 times faster than an online version of Benders Decomposition while finding decisions of similar quality. Such computational results motivate a paradigm shift in optimization algorithms that are intended for modern streaming applications.\",\"PeriodicalId\":55227,\"journal\":{\"name\":\"Computational Optimization and Applications\",\"volume\":\"2015 1\",\"pages\":\"0\"},\"PeriodicalIF\":2.0000,\"publicationDate\":\"2023-09-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Computational Optimization and Applications\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s10589-023-00529-5\",\"RegionNum\":2,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"MATHEMATICS, APPLIED\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Optimization and Applications","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s10589-023-00529-5","RegionNum":2,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"MATHEMATICS, APPLIED","Score":null,"Total":0}

Distribution-free algorithms for predictive stochastic programming in the presence of streaming data

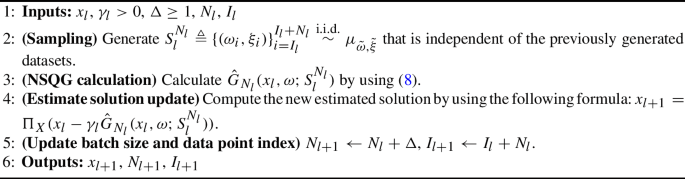

Abstract This paper studies a fusion of concepts from stochastic programming and non-parametric statistical learning in which data is available in the form of covariates interpreted as predictors and responses. Such models are designed to impart greater agility, allowing decisions under uncertainty to adapt to the knowledge of predictors (leading indicators). This paper studies two classes of methods for such joint prediction-optimization models. One of the methods may be classified as a first-order method, whereas the other studies piecewise linear approximations. Both of these methods are based on coupling non-parametric estimation for predictive purposes, and optimization for decision-making within one unified framework. In addition, our study incorporates several non-parametric estimation schemes, including k nearest neighbors ( k NN) and other standard kernel estimators. Our computational results demonstrate that the new algorithms proposed in this paper outperform traditional approaches which were not designed for streaming data applications requiring simultaneous estimation and optimization as important design features for such algorithms. For instance, coupling k NN with Stochastic Decomposition (SD) turns out to be over 40 times faster than an online version of Benders Decomposition while finding decisions of similar quality. Such computational results motivate a paradigm shift in optimization algorithms that are intended for modern streaming applications.

期刊介绍:

Computational Optimization and Applications is a peer reviewed journal that is committed to timely publication of research and tutorial papers on the analysis and development of computational algorithms and modeling technology for optimization. Algorithms either for general classes of optimization problems or for more specific applied problems are of interest. Stochastic algorithms as well as deterministic algorithms will be considered. Papers that can provide both theoretical analysis, along with carefully designed computational experiments, are particularly welcome.

Topics of interest include, but are not limited to the following:

Large Scale Optimization,

Unconstrained Optimization,

Linear Programming,

Quadratic Programming Complementarity Problems, and Variational Inequalities,

Constrained Optimization,

Nondifferentiable Optimization,

Integer Programming,

Combinatorial Optimization,

Stochastic Optimization,

Multiobjective Optimization,

Network Optimization,

Complexity Theory,

Approximations and Error Analysis,

Parametric Programming and Sensitivity Analysis,

Parallel Computing, Distributed Computing, and Vector Processing,

Software, Benchmarks, Numerical Experimentation and Comparisons,

Modelling Languages and Systems for Optimization,

Automatic Differentiation,

Applications in Engineering, Finance, Optimal Control, Optimal Design, Operations Research,

Transportation, Economics, Communications, Manufacturing, and Management Science.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们