{"title":"政府会计准则对公共部门养老基金的影响","authors":"Divya Anantharaman, Elizabeth Chuk","doi":"10.1007/s11142-022-09746-5","DOIUrl":null,"url":null,"abstract":"The funding policy for defined benefit pension plans covering government employees represents an important decision for governments sponsoring those plans. Many state and local government plans have become severely underfunded (e.g., New Jersey, Illinois, and Detroit), raising concerns about whether governments are contributing enough to their pensions. Governmental Accounting Standards Board Statements 67/68 (GASB 67/68) fundamentally alter the financial reporting of pension liabilities, by (i) requiring pension liabilities to be estimated using a potentially lower discount rate (increasing estimated liabilities and any funding deficits), and (ii) mandating balance sheet recognition of funding deficits/surpluses. Although GASB 67/68 only change financial reporting and acknowledge specifically that funding is outside their scope, we find, for 100 large state-administered plans, that governments increase pension contributions significantly upon applying GASB 67/68. This funding response is stronger from governments likely to face greater political consequences once pension deficits are made prominent by GASB 67/68. Benefit cuts are also more likely post GASB 67/68, but plans that increase funding are less likely to cut benefits—suggesting that these responses substitute for each other and that pension funding is more of a fiscal priority in some states than others. Overall, our findings suggest that purely accounting changes can have “real” effects on governmental pension policy.","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"3 1","pages":"0"},"PeriodicalIF":5.8000,"publicationDate":"2023-03-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"1","resultStr":"{\"title\":\"The impact of governmental accounting standards on public-sector pension funding\",\"authors\":\"Divya Anantharaman, Elizabeth Chuk\",\"doi\":\"10.1007/s11142-022-09746-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"The funding policy for defined benefit pension plans covering government employees represents an important decision for governments sponsoring those plans. Many state and local government plans have become severely underfunded (e.g., New Jersey, Illinois, and Detroit), raising concerns about whether governments are contributing enough to their pensions. Governmental Accounting Standards Board Statements 67/68 (GASB 67/68) fundamentally alter the financial reporting of pension liabilities, by (i) requiring pension liabilities to be estimated using a potentially lower discount rate (increasing estimated liabilities and any funding deficits), and (ii) mandating balance sheet recognition of funding deficits/surpluses. Although GASB 67/68 only change financial reporting and acknowledge specifically that funding is outside their scope, we find, for 100 large state-administered plans, that governments increase pension contributions significantly upon applying GASB 67/68. This funding response is stronger from governments likely to face greater political consequences once pension deficits are made prominent by GASB 67/68. Benefit cuts are also more likely post GASB 67/68, but plans that increase funding are less likely to cut benefits—suggesting that these responses substitute for each other and that pension funding is more of a fiscal priority in some states than others. Overall, our findings suggest that purely accounting changes can have “real” effects on governmental pension policy.\",\"PeriodicalId\":48120,\"journal\":{\"name\":\"Review of Accounting Studies\",\"volume\":\"3 1\",\"pages\":\"0\"},\"PeriodicalIF\":5.8000,\"publicationDate\":\"2023-03-23\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Accounting Studies\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11142-022-09746-5\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11142-022-09746-5","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

The impact of governmental accounting standards on public-sector pension funding

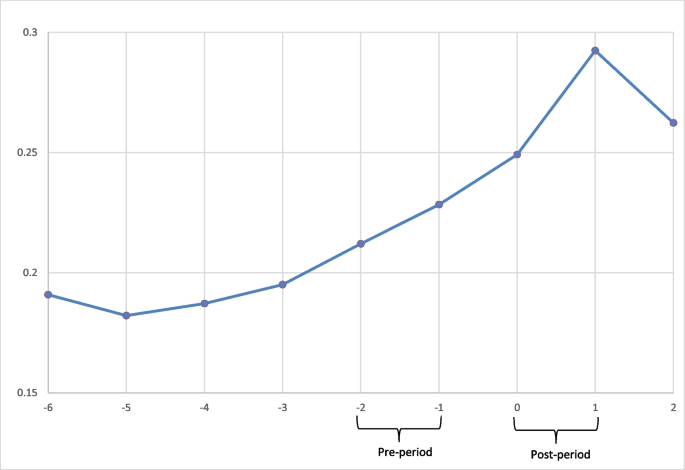

The funding policy for defined benefit pension plans covering government employees represents an important decision for governments sponsoring those plans. Many state and local government plans have become severely underfunded (e.g., New Jersey, Illinois, and Detroit), raising concerns about whether governments are contributing enough to their pensions. Governmental Accounting Standards Board Statements 67/68 (GASB 67/68) fundamentally alter the financial reporting of pension liabilities, by (i) requiring pension liabilities to be estimated using a potentially lower discount rate (increasing estimated liabilities and any funding deficits), and (ii) mandating balance sheet recognition of funding deficits/surpluses. Although GASB 67/68 only change financial reporting and acknowledge specifically that funding is outside their scope, we find, for 100 large state-administered plans, that governments increase pension contributions significantly upon applying GASB 67/68. This funding response is stronger from governments likely to face greater political consequences once pension deficits are made prominent by GASB 67/68. Benefit cuts are also more likely post GASB 67/68, but plans that increase funding are less likely to cut benefits—suggesting that these responses substitute for each other and that pension funding is more of a fiscal priority in some states than others. Overall, our findings suggest that purely accounting changes can have “real” effects on governmental pension policy.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们