{"title":"在并购中,哪些倍数很重要?概述","authors":"Matthew Shaffer","doi":"10.1007/s11142-023-09768-7","DOIUrl":null,"url":null,"abstract":"Abstract This paper provides an overview of valuation multiples in mergers and acquisitions advisory. I review the literature and legal controversies and the theoretical basis for their role. I then standardize all the advisor multiples available in SDC Platinum along four dimensions and report rich descriptive statistics on each dimension over time and across industries. I highlight eight findings that are notable in light of current knowledge and debates. This paper answers the call from Gow et al. (Journal of Accounting Research 54(2):477–523, 2016) for thorough descriptive research, to provide a foundation and prompts for future hypothesis development. It includes an explicit guide for using this data, an overview of the key institutional details, and a discussion of tractable and open research questions.","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"59 1","pages":"0"},"PeriodicalIF":5.8000,"publicationDate":"2023-06-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"1","resultStr":"{\"title\":\"Which multiples matter in M &A? An overview\",\"authors\":\"Matthew Shaffer\",\"doi\":\"10.1007/s11142-023-09768-7\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract This paper provides an overview of valuation multiples in mergers and acquisitions advisory. I review the literature and legal controversies and the theoretical basis for their role. I then standardize all the advisor multiples available in SDC Platinum along four dimensions and report rich descriptive statistics on each dimension over time and across industries. I highlight eight findings that are notable in light of current knowledge and debates. This paper answers the call from Gow et al. (Journal of Accounting Research 54(2):477–523, 2016) for thorough descriptive research, to provide a foundation and prompts for future hypothesis development. It includes an explicit guide for using this data, an overview of the key institutional details, and a discussion of tractable and open research questions.\",\"PeriodicalId\":48120,\"journal\":{\"name\":\"Review of Accounting Studies\",\"volume\":\"59 1\",\"pages\":\"0\"},\"PeriodicalIF\":5.8000,\"publicationDate\":\"2023-06-21\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Accounting Studies\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11142-023-09768-7\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11142-023-09768-7","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 1

摘要

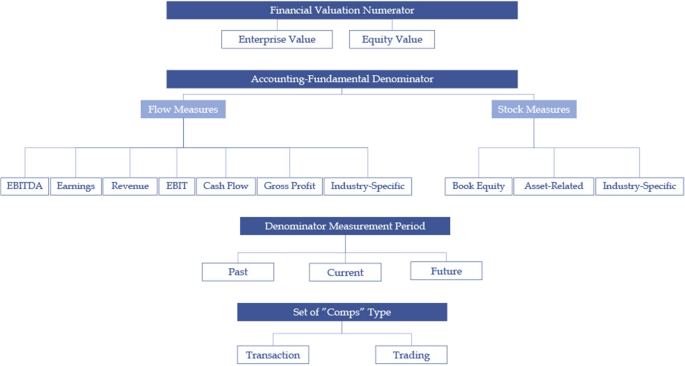

摘要本文对并购咨询中的估值倍数进行了概述。我回顾了文献和法律争议及其作用的理论基础。然后,我将SDC Platinum中可用的所有顾问倍数沿着四个维度进行标准化,并报告每个维度随时间和跨行业的丰富描述性统计数据。根据目前的知识和辩论,我强调了八个值得注意的发现。本文响应Gow等人(Journal of Accounting Research 54(2): 477-523, 2016)的呼吁,进行深入的描述性研究,为未来的假设发展提供基础和提示。它包括使用这些数据的明确指南,对关键机构细节的概述,以及对可处理和开放的研究问题的讨论。

Abstract This paper provides an overview of valuation multiples in mergers and acquisitions advisory. I review the literature and legal controversies and the theoretical basis for their role. I then standardize all the advisor multiples available in SDC Platinum along four dimensions and report rich descriptive statistics on each dimension over time and across industries. I highlight eight findings that are notable in light of current knowledge and debates. This paper answers the call from Gow et al. (Journal of Accounting Research 54(2):477–523, 2016) for thorough descriptive research, to provide a foundation and prompts for future hypothesis development. It includes an explicit guide for using this data, an overview of the key institutional details, and a discussion of tractable and open research questions.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们