{"title":"报告毛利率的整数参考点和不规则模式","authors":"Matthew Cedergren, Valerie Li","doi":"10.1007/s11142-023-09780-x","DOIUrl":null,"url":null,"abstract":"Abstract We find irregular patterns in the distribution of firms’ reported quarterly gross margin percentages. Specifically, there is significant bunching around percentage integers that are highly round (e.g., multiples of 10, such as 30%, 40%, etc.) or are neatly divisible (e.g., 25%, 75%), compared to what is predicted by counterfactual distributions. Further investigation reveals that highly round gross margin firms are smaller, exert higher effort, achieve higher productivity, have more difficult goals, and pay their CEOs with a higher portion of fixed income. We also find that highly round gross margins are associated with superior performance. Additionally, we do not find consistent evidence that highly round gross margin reference points are linked to external rewards. Collectively, our evidence is consistent with reference-dependent preferences for highly round gross margins likely being driven by intrinsic (rather than extrinsic) motivations.","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"44 1","pages":"0"},"PeriodicalIF":5.8000,"publicationDate":"2023-06-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Round number reference points and irregular patterns in reported gross margins\",\"authors\":\"Matthew Cedergren, Valerie Li\",\"doi\":\"10.1007/s11142-023-09780-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract We find irregular patterns in the distribution of firms’ reported quarterly gross margin percentages. Specifically, there is significant bunching around percentage integers that are highly round (e.g., multiples of 10, such as 30%, 40%, etc.) or are neatly divisible (e.g., 25%, 75%), compared to what is predicted by counterfactual distributions. Further investigation reveals that highly round gross margin firms are smaller, exert higher effort, achieve higher productivity, have more difficult goals, and pay their CEOs with a higher portion of fixed income. We also find that highly round gross margins are associated with superior performance. Additionally, we do not find consistent evidence that highly round gross margin reference points are linked to external rewards. Collectively, our evidence is consistent with reference-dependent preferences for highly round gross margins likely being driven by intrinsic (rather than extrinsic) motivations.\",\"PeriodicalId\":48120,\"journal\":{\"name\":\"Review of Accounting Studies\",\"volume\":\"44 1\",\"pages\":\"0\"},\"PeriodicalIF\":5.8000,\"publicationDate\":\"2023-06-21\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Accounting Studies\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11142-023-09780-x\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11142-023-09780-x","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Round number reference points and irregular patterns in reported gross margins

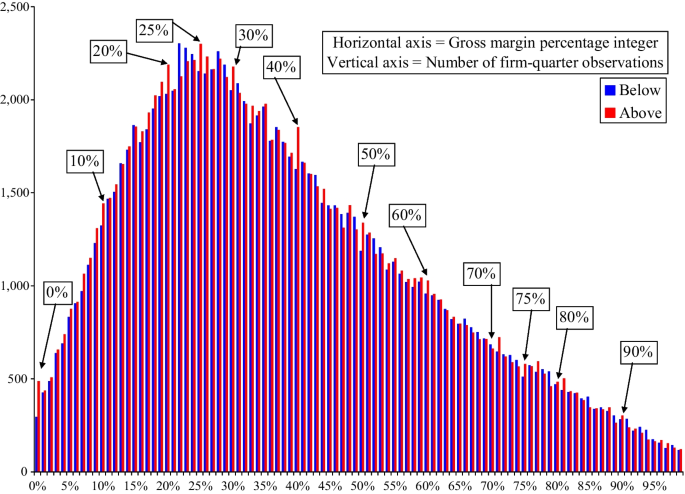

Abstract We find irregular patterns in the distribution of firms’ reported quarterly gross margin percentages. Specifically, there is significant bunching around percentage integers that are highly round (e.g., multiples of 10, such as 30%, 40%, etc.) or are neatly divisible (e.g., 25%, 75%), compared to what is predicted by counterfactual distributions. Further investigation reveals that highly round gross margin firms are smaller, exert higher effort, achieve higher productivity, have more difficult goals, and pay their CEOs with a higher portion of fixed income. We also find that highly round gross margins are associated with superior performance. Additionally, we do not find consistent evidence that highly round gross margin reference points are linked to external rewards. Collectively, our evidence is consistent with reference-dependent preferences for highly round gross margins likely being driven by intrinsic (rather than extrinsic) motivations.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们