{"title":"对同等的酒征收同等的税?饮料种类与反社会和非法行为*","authors":"Preety Srivastava, Ou Yang, Xueyan Zhao","doi":"10.1111/1475-4932.12704","DOIUrl":null,"url":null,"abstract":"<p>Alcohol taxation is an important policy instrument for correcting for market failures associated with excessive alcohol consumption. This paper examines the beverage-specific negative externalities by providing empirical evidence linking ten alcoholic beverage types to drink-driving and hazardous, disturbing or abusive behaviours when intoxicated, using data from six waves of an Australian recreational drug survey. We find that regular-strength beer and pre-mixed spirits in a can rank the highest in their links to negative behaviours, followed by mid-strength beer, cask wine, and bottled spirits. Conversely, drinking low-strength beer or fortified wine reduces the probability of these risky and unlawful behaviours. Bottled wine is shown to be associated with an elevated chance of drink-driving but a reduced chance of other negative behaviours. In contrast to the existing volumetric tax rates for per litre of alcohol, of all harmful beverage types, cask wine appears to be significantly undertaxed relative to its external costs to society. We also note that regular- and mid-strength beer are comparable to pre-mixed drinks in terms of external costs, and yet there is a significant disparity across their tax rates.</p>","PeriodicalId":47484,"journal":{"name":"Economic Record","volume":"98 323","pages":"354-372"},"PeriodicalIF":1.2000,"publicationDate":"2022-11-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-4932.12704","citationCount":"0","resultStr":"{\"title\":\"Equal Tax for Equal Alcohol? Beverage Types and Antisocial and Unlawful Behaviours*\",\"authors\":\"Preety Srivastava, Ou Yang, Xueyan Zhao\",\"doi\":\"10.1111/1475-4932.12704\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Alcohol taxation is an important policy instrument for correcting for market failures associated with excessive alcohol consumption. This paper examines the beverage-specific negative externalities by providing empirical evidence linking ten alcoholic beverage types to drink-driving and hazardous, disturbing or abusive behaviours when intoxicated, using data from six waves of an Australian recreational drug survey. We find that regular-strength beer and pre-mixed spirits in a can rank the highest in their links to negative behaviours, followed by mid-strength beer, cask wine, and bottled spirits. Conversely, drinking low-strength beer or fortified wine reduces the probability of these risky and unlawful behaviours. Bottled wine is shown to be associated with an elevated chance of drink-driving but a reduced chance of other negative behaviours. In contrast to the existing volumetric tax rates for per litre of alcohol, of all harmful beverage types, cask wine appears to be significantly undertaxed relative to its external costs to society. We also note that regular- and mid-strength beer are comparable to pre-mixed drinks in terms of external costs, and yet there is a significant disparity across their tax rates.</p>\",\"PeriodicalId\":47484,\"journal\":{\"name\":\"Economic Record\",\"volume\":\"98 323\",\"pages\":\"354-372\"},\"PeriodicalIF\":1.2000,\"publicationDate\":\"2022-11-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-4932.12704\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Economic Record\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1475-4932.12704\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Economic Record","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1475-4932.12704","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Equal Tax for Equal Alcohol? Beverage Types and Antisocial and Unlawful Behaviours*

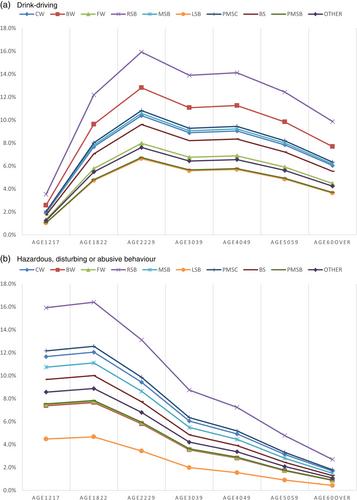

Alcohol taxation is an important policy instrument for correcting for market failures associated with excessive alcohol consumption. This paper examines the beverage-specific negative externalities by providing empirical evidence linking ten alcoholic beverage types to drink-driving and hazardous, disturbing or abusive behaviours when intoxicated, using data from six waves of an Australian recreational drug survey. We find that regular-strength beer and pre-mixed spirits in a can rank the highest in their links to negative behaviours, followed by mid-strength beer, cask wine, and bottled spirits. Conversely, drinking low-strength beer or fortified wine reduces the probability of these risky and unlawful behaviours. Bottled wine is shown to be associated with an elevated chance of drink-driving but a reduced chance of other negative behaviours. In contrast to the existing volumetric tax rates for per litre of alcohol, of all harmful beverage types, cask wine appears to be significantly undertaxed relative to its external costs to society. We also note that regular- and mid-strength beer are comparable to pre-mixed drinks in terms of external costs, and yet there is a significant disparity across their tax rates.

期刊介绍:

Published on behalf of the Economic Society of Australia, the Economic Record is intended to act as a vehicle for the communication of advances in knowledge and understanding in economics. It publishes papers in the theoretical, applied and policy areas of economics and provides a forum for research on the Australian economy. It also publishes surveys in economics and book reviews to facilitate the dissemination of knowledge.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们