Pierdomenico Duttilo, Stefano Antonio Gattone, Barbara Iannone

{"title":"混合广义正态分布和EGARCH模型来分析ESG和传统投资的回报和波动性","authors":"Pierdomenico Duttilo, Stefano Antonio Gattone, Barbara Iannone","doi":"10.1007/s10182-023-00487-7","DOIUrl":null,"url":null,"abstract":"<div><p>Environmental, social and governance (ESG) criteria are increasingly integrated into investment process to contribute to overcoming global sustainability challenges. Focusing on the reaction to turmoil periods, this work analyses returns and volatility of several ESG indices and makes a comparison with their traditional counterparts from 2016 to 2022. These indices comprise the following markets: Global, the US, Europe and emerging markets. Firstly, the two-component mixture of generalized normal distribution was exploited to objectively detect financial market turmoil periods with the Naïve Bayes’ classifier. Secondly, the EGARCH-in-mean model with exogenous dummy variables was applied to capture the turmoil period impact. Results show that returns and volatility are both affected by turmoil periods. The return–risk performance differs by index type and market: the European ESG index is less volatile than its traditional market benchmark, while in the other markets, the estimated volatility is approximately the same. Moreover, ESG and non-ESG indices differ in terms of turmoil periods impact, risk premium and leverage effect.</p></div>","PeriodicalId":55446,"journal":{"name":"Asta-Advances in Statistical Analysis","volume":"108 4","pages":"755 - 775"},"PeriodicalIF":1.4000,"publicationDate":"2023-11-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://link.springer.com/content/pdf/10.1007/s10182-023-00487-7.pdf","citationCount":"0","resultStr":"{\"title\":\"Mixtures of generalized normal distributions and EGARCH models to analyse returns and volatility of ESG and traditional investments\",\"authors\":\"Pierdomenico Duttilo, Stefano Antonio Gattone, Barbara Iannone\",\"doi\":\"10.1007/s10182-023-00487-7\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Environmental, social and governance (ESG) criteria are increasingly integrated into investment process to contribute to overcoming global sustainability challenges. Focusing on the reaction to turmoil periods, this work analyses returns and volatility of several ESG indices and makes a comparison with their traditional counterparts from 2016 to 2022. These indices comprise the following markets: Global, the US, Europe and emerging markets. Firstly, the two-component mixture of generalized normal distribution was exploited to objectively detect financial market turmoil periods with the Naïve Bayes’ classifier. Secondly, the EGARCH-in-mean model with exogenous dummy variables was applied to capture the turmoil period impact. Results show that returns and volatility are both affected by turmoil periods. The return–risk performance differs by index type and market: the European ESG index is less volatile than its traditional market benchmark, while in the other markets, the estimated volatility is approximately the same. Moreover, ESG and non-ESG indices differ in terms of turmoil periods impact, risk premium and leverage effect.</p></div>\",\"PeriodicalId\":55446,\"journal\":{\"name\":\"Asta-Advances in Statistical Analysis\",\"volume\":\"108 4\",\"pages\":\"755 - 775\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-11-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://link.springer.com/content/pdf/10.1007/s10182-023-00487-7.pdf\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asta-Advances in Statistical Analysis\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10182-023-00487-7\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asta-Advances in Statistical Analysis","FirstCategoryId":"100","ListUrlMain":"https://link.springer.com/article/10.1007/s10182-023-00487-7","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

Mixtures of generalized normal distributions and EGARCH models to analyse returns and volatility of ESG and traditional investments

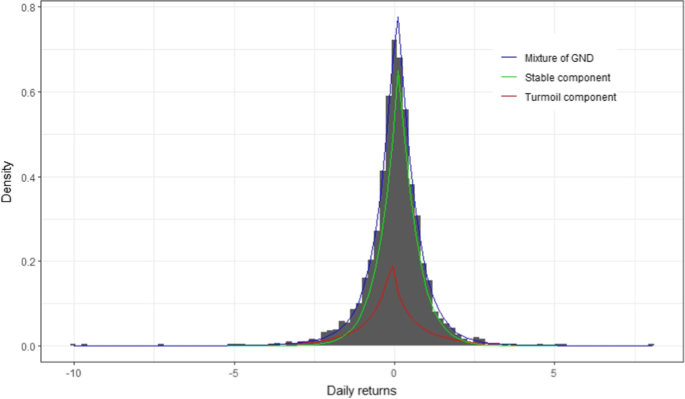

Environmental, social and governance (ESG) criteria are increasingly integrated into investment process to contribute to overcoming global sustainability challenges. Focusing on the reaction to turmoil periods, this work analyses returns and volatility of several ESG indices and makes a comparison with their traditional counterparts from 2016 to 2022. These indices comprise the following markets: Global, the US, Europe and emerging markets. Firstly, the two-component mixture of generalized normal distribution was exploited to objectively detect financial market turmoil periods with the Naïve Bayes’ classifier. Secondly, the EGARCH-in-mean model with exogenous dummy variables was applied to capture the turmoil period impact. Results show that returns and volatility are both affected by turmoil periods. The return–risk performance differs by index type and market: the European ESG index is less volatile than its traditional market benchmark, while in the other markets, the estimated volatility is approximately the same. Moreover, ESG and non-ESG indices differ in terms of turmoil periods impact, risk premium and leverage effect.

期刊介绍:

AStA - Advances in Statistical Analysis, a journal of the German Statistical Society, is published quarterly and presents original contributions on statistical methods and applications and review articles.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们