Michiel Bijlsma, Carin van der Cruijsen, Nicole Jonker, Jelmer Reijerink

{"title":"是什么促使消费者采用央行数字货币?","authors":"Michiel Bijlsma, Carin van der Cruijsen, Nicole Jonker, Jelmer Reijerink","doi":"10.1007/s10693-023-00420-8","DOIUrl":null,"url":null,"abstract":"<p>Central banks around the world are examining the possibility of introducing Central Bank Digital Currency (CBDC). The public’s preferences concerning the usage of CBDC for paying and saving are important determinants of the success of CBDC. However, little is known yet about consumers’ attitudes towards CBDC. Using data from a representative panel of Dutch consumers we find that roughly half of the public says it would open a CBDC current account. The same holds for a CBDC savings account. Thus, we find clear potential for CBDC in the Netherlands. This suggests that consumers perceive CBDC as distinct from current and savings accounts offered by traditional banks. Intended CBDC usage is positively related to respondents’ knowledge of CBDC and trust in the central bank. Price incentives matter as well. The amount respondents say they would want to deposit in the CBDC savings account depends on the interest rate offered. Furthermore, intended usage of the CBDC current account is highest among people who find privacy and security important and among consumers with low trust in banks in general. These results suggest that central banks can steer consumers’ adoption of CBDC via the interest rate, by a design of CBDC that takes into account the public’s need for security and privacy, and by clear communication about what CBDC entails.</p>","PeriodicalId":51503,"journal":{"name":"Journal of Financial Services Research","volume":"221 3-4","pages":""},"PeriodicalIF":2.0000,"publicationDate":"2023-11-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"What Triggers Consumer Adoption of Central Bank Digital Currency?\",\"authors\":\"Michiel Bijlsma, Carin van der Cruijsen, Nicole Jonker, Jelmer Reijerink\",\"doi\":\"10.1007/s10693-023-00420-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Central banks around the world are examining the possibility of introducing Central Bank Digital Currency (CBDC). The public’s preferences concerning the usage of CBDC for paying and saving are important determinants of the success of CBDC. However, little is known yet about consumers’ attitudes towards CBDC. Using data from a representative panel of Dutch consumers we find that roughly half of the public says it would open a CBDC current account. The same holds for a CBDC savings account. Thus, we find clear potential for CBDC in the Netherlands. This suggests that consumers perceive CBDC as distinct from current and savings accounts offered by traditional banks. Intended CBDC usage is positively related to respondents’ knowledge of CBDC and trust in the central bank. Price incentives matter as well. The amount respondents say they would want to deposit in the CBDC savings account depends on the interest rate offered. Furthermore, intended usage of the CBDC current account is highest among people who find privacy and security important and among consumers with low trust in banks in general. These results suggest that central banks can steer consumers’ adoption of CBDC via the interest rate, by a design of CBDC that takes into account the public’s need for security and privacy, and by clear communication about what CBDC entails.</p>\",\"PeriodicalId\":51503,\"journal\":{\"name\":\"Journal of Financial Services Research\",\"volume\":\"221 3-4\",\"pages\":\"\"},\"PeriodicalIF\":2.0000,\"publicationDate\":\"2023-11-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Financial Services Research\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10693-023-00420-8\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Financial Services Research","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10693-023-00420-8","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

What Triggers Consumer Adoption of Central Bank Digital Currency?

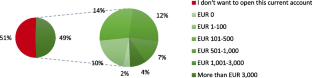

Central banks around the world are examining the possibility of introducing Central Bank Digital Currency (CBDC). The public’s preferences concerning the usage of CBDC for paying and saving are important determinants of the success of CBDC. However, little is known yet about consumers’ attitudes towards CBDC. Using data from a representative panel of Dutch consumers we find that roughly half of the public says it would open a CBDC current account. The same holds for a CBDC savings account. Thus, we find clear potential for CBDC in the Netherlands. This suggests that consumers perceive CBDC as distinct from current and savings accounts offered by traditional banks. Intended CBDC usage is positively related to respondents’ knowledge of CBDC and trust in the central bank. Price incentives matter as well. The amount respondents say they would want to deposit in the CBDC savings account depends on the interest rate offered. Furthermore, intended usage of the CBDC current account is highest among people who find privacy and security important and among consumers with low trust in banks in general. These results suggest that central banks can steer consumers’ adoption of CBDC via the interest rate, by a design of CBDC that takes into account the public’s need for security and privacy, and by clear communication about what CBDC entails.

期刊介绍:

The Journal of Financial Services Research publishes high quality empirical and theoretical research on the demand, supply, regulation, and pricing of financial services. Financial services are broadly defined to include banking, risk management, capital markets, mutual funds, insurance, venture capital, consumer and corporate finance, and the technologies used to produce, distribute, and regulate these services. Macro-financial policy issues, including comparative financial systems, the globalization of financial services, and the impact of these phenomena on economic growth and financial stability, are also within the JFSR’s scope of interest. The Journal seeks to promote research that enriches the profession’s understanding of financial services industries, to elevate industry and product efficiencies, as well as to inform the debate and promote the formulation of sound public policies. Officially cited as: J Financ Serv Res

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们