Mohammad Enamul Hoque, Faik Bilgili, Sourav Batabyal

{"title":"我们对气候变化期货市场和碳期货市场之间的溢出效应了解多少?","authors":"Mohammad Enamul Hoque, Faik Bilgili, Sourav Batabyal","doi":"10.1007/s10584-023-03640-y","DOIUrl":null,"url":null,"abstract":"<p>Climate action-based assumptions and tradable characteristics underpinned the development of climate change futures contracts, which are related to carbon and climate markets. Therefore, this paper examines return and volatility spillover between climate change futures and carbon allowance futures using dynamic conditional correlation (DCC) and asymmetric dynamic conditional correlation (ADCC) models with daily and weekly frequency data. Considering the emergence of US market-based carbon futures and climate futures, this study explores bivariate optimal hedging strategies and optimal portfolio strategies. Using daily data, this study discovers unidirectional and positive return and volatility spillover from the carbon futures market to the climate change futures market, implying opportunities for diversification and hedging. The weekly analysis shows bidirectional and negative return spillover between the carbon futures market and the climate change futures market, implying opportunities for risk hedging. In addition, it also reveals unidirectional and positive volatility spillovers from the carbon futures market to the climate change futures market. The carbon market dominates the climate change futures market. The study also reveals that optimal portfolio strategies will be preferred over optimal hedging strategies. Therefore, this study offers practical implications for investors and portfolio managers.</p>","PeriodicalId":10372,"journal":{"name":"Climatic Change","volume":"357 ","pages":""},"PeriodicalIF":4.8000,"publicationDate":"2023-11-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"What do we know about spillover between the climate change futures market and the carbon futures market?\",\"authors\":\"Mohammad Enamul Hoque, Faik Bilgili, Sourav Batabyal\",\"doi\":\"10.1007/s10584-023-03640-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Climate action-based assumptions and tradable characteristics underpinned the development of climate change futures contracts, which are related to carbon and climate markets. Therefore, this paper examines return and volatility spillover between climate change futures and carbon allowance futures using dynamic conditional correlation (DCC) and asymmetric dynamic conditional correlation (ADCC) models with daily and weekly frequency data. Considering the emergence of US market-based carbon futures and climate futures, this study explores bivariate optimal hedging strategies and optimal portfolio strategies. Using daily data, this study discovers unidirectional and positive return and volatility spillover from the carbon futures market to the climate change futures market, implying opportunities for diversification and hedging. The weekly analysis shows bidirectional and negative return spillover between the carbon futures market and the climate change futures market, implying opportunities for risk hedging. In addition, it also reveals unidirectional and positive volatility spillovers from the carbon futures market to the climate change futures market. The carbon market dominates the climate change futures market. The study also reveals that optimal portfolio strategies will be preferred over optimal hedging strategies. Therefore, this study offers practical implications for investors and portfolio managers.</p>\",\"PeriodicalId\":10372,\"journal\":{\"name\":\"Climatic Change\",\"volume\":\"357 \",\"pages\":\"\"},\"PeriodicalIF\":4.8000,\"publicationDate\":\"2023-11-25\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Climatic Change\",\"FirstCategoryId\":\"93\",\"ListUrlMain\":\"https://doi.org/10.1007/s10584-023-03640-y\",\"RegionNum\":2,\"RegionCategory\":\"环境科学与生态学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ENVIRONMENTAL SCIENCES\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Climatic Change","FirstCategoryId":"93","ListUrlMain":"https://doi.org/10.1007/s10584-023-03640-y","RegionNum":2,"RegionCategory":"环境科学与生态学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ENVIRONMENTAL SCIENCES","Score":null,"Total":0}

What do we know about spillover between the climate change futures market and the carbon futures market?

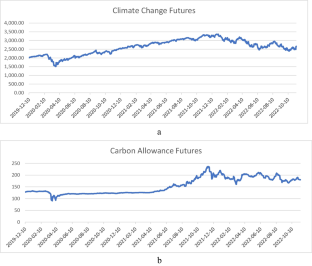

Climate action-based assumptions and tradable characteristics underpinned the development of climate change futures contracts, which are related to carbon and climate markets. Therefore, this paper examines return and volatility spillover between climate change futures and carbon allowance futures using dynamic conditional correlation (DCC) and asymmetric dynamic conditional correlation (ADCC) models with daily and weekly frequency data. Considering the emergence of US market-based carbon futures and climate futures, this study explores bivariate optimal hedging strategies and optimal portfolio strategies. Using daily data, this study discovers unidirectional and positive return and volatility spillover from the carbon futures market to the climate change futures market, implying opportunities for diversification and hedging. The weekly analysis shows bidirectional and negative return spillover between the carbon futures market and the climate change futures market, implying opportunities for risk hedging. In addition, it also reveals unidirectional and positive volatility spillovers from the carbon futures market to the climate change futures market. The carbon market dominates the climate change futures market. The study also reveals that optimal portfolio strategies will be preferred over optimal hedging strategies. Therefore, this study offers practical implications for investors and portfolio managers.

期刊介绍:

Climatic Change is dedicated to the totality of the problem of climatic variability and change - its descriptions, causes, implications and interactions among these. The purpose of the journal is to provide a means of exchange among those working in different disciplines on problems related to climatic variations. This means that authors have an opportunity to communicate the essence of their studies to people in other climate-related disciplines and to interested non-disciplinarians, as well as to report on research in which the originality is in the combinations of (not necessarily original) work from several disciplines. The journal also includes vigorous editorial and book review sections.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们