{"title":"经财务顾问筛选的客户披露的信息更少","authors":"Doron Samuell, Demetris Christodoulou","doi":"10.1111/jori.12453","DOIUrl":null,"url":null,"abstract":"<p>We find that there are fewer disclosures of risk factors when customers for life insurance are screened by financial advisors, compared with when similar profile customers are screened directly by the insurer's telephone operators. The lower rate of disclosure is systematic across all medical and lifestyle risks and has a sizeable economic impact on customer premiums. As a result, customers screened by advisors enjoy unfairly cheaper and more favorable policies. We identify the key drivers of lower customer disclosures to be conflicted incentives and lower scrutiny. We assert that the fewer disclosures from customers screened by advisors may translate into noncaptured risk that could be cross-subsidized by customers who provide more complete disclosures through the insurer's telephone operators. On reviewing our findings, the participating insurer in the study calculated that removing advisors from the screening process could allow certain insurance products to be heavily discounted while maintaining profitability.</p>","PeriodicalId":51440,"journal":{"name":"Journal of Risk and Insurance","volume":"91 1","pages":"93-120"},"PeriodicalIF":1.7000,"publicationDate":"2023-11-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jori.12453","citationCount":"0","resultStr":"{\"title\":\"Lower disclosures from customers screened by financial advisors\",\"authors\":\"Doron Samuell, Demetris Christodoulou\",\"doi\":\"10.1111/jori.12453\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We find that there are fewer disclosures of risk factors when customers for life insurance are screened by financial advisors, compared with when similar profile customers are screened directly by the insurer's telephone operators. The lower rate of disclosure is systematic across all medical and lifestyle risks and has a sizeable economic impact on customer premiums. As a result, customers screened by advisors enjoy unfairly cheaper and more favorable policies. We identify the key drivers of lower customer disclosures to be conflicted incentives and lower scrutiny. We assert that the fewer disclosures from customers screened by advisors may translate into noncaptured risk that could be cross-subsidized by customers who provide more complete disclosures through the insurer's telephone operators. On reviewing our findings, the participating insurer in the study calculated that removing advisors from the screening process could allow certain insurance products to be heavily discounted while maintaining profitability.</p>\",\"PeriodicalId\":51440,\"journal\":{\"name\":\"Journal of Risk and Insurance\",\"volume\":\"91 1\",\"pages\":\"93-120\"},\"PeriodicalIF\":1.7000,\"publicationDate\":\"2023-11-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jori.12453\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Risk and Insurance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jori.12453\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Risk and Insurance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jori.12453","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Lower disclosures from customers screened by financial advisors

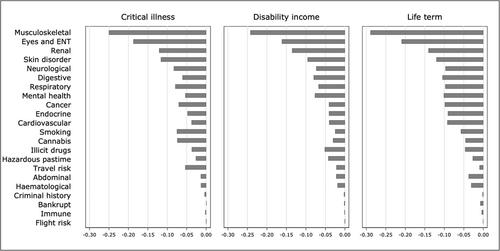

We find that there are fewer disclosures of risk factors when customers for life insurance are screened by financial advisors, compared with when similar profile customers are screened directly by the insurer's telephone operators. The lower rate of disclosure is systematic across all medical and lifestyle risks and has a sizeable economic impact on customer premiums. As a result, customers screened by advisors enjoy unfairly cheaper and more favorable policies. We identify the key drivers of lower customer disclosures to be conflicted incentives and lower scrutiny. We assert that the fewer disclosures from customers screened by advisors may translate into noncaptured risk that could be cross-subsidized by customers who provide more complete disclosures through the insurer's telephone operators. On reviewing our findings, the participating insurer in the study calculated that removing advisors from the screening process could allow certain insurance products to be heavily discounted while maintaining profitability.

期刊介绍:

The Journal of Risk and Insurance (JRI) is the premier outlet for theoretical and empirical research on the topics of insurance economics and risk management. Research in the JRI informs practice, policy-making, and regulation in insurance markets as well as corporate and household risk management. JRI is the flagship journal for the American Risk and Insurance Association, and is currently indexed by the American Economic Association’s Economic Literature Index, RePEc, the Social Sciences Citation Index, and others. Issues of the Journal of Risk and Insurance, from volume one to volume 82 (2015), are available online through JSTOR . Recent issues of JRI are available through Wiley Online Library. In addition to the research areas of traditional strength for the JRI, the editorial team highlights below specific areas for special focus in the near term, due to their current relevance for the field.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们