Katharine D. Drake, Nathan C. Goldman, Stephen J. Lusch, Jaime J. Schmidt

{"title":"披露与税务有关的重要审计事项和与税务有关的结果","authors":"Katharine D. Drake, Nathan C. Goldman, Stephen J. Lusch, Jaime J. Schmidt","doi":"10.1111/1911-3846.12920","DOIUrl":null,"url":null,"abstract":"<p>Given that tax-related critical audit matters (tax CAMs) were prevalent among accelerated filers (18.5% of observations) during the initial year of CAM disclosures, we examine whether an auditor's disclosure of tax CAMs is associated with variation in tax-related financial reporting quality, tax avoidance, and tax-related earnings management. Finding an association between tax CAMs and one of these tax outcomes would indicate that the new auditor reporting standard has indirectly affected investors. Examining the first year of CAM disclosures, we do not find that tax CAMs are associated with broad proxies of tax-related audit or financial reporting quality (e.g., restatements, internal control weaknesses, comment letters) or tax avoidance (e.g., effective tax rates or book-to-tax differences). We do find that tax CAMs are associated with a modest increase in tax accrual quality, an increase in the reserve for unrecognized tax benefits, and a reduction in the likelihood of tax-related earnings management. However, we do not find these tax CAM effects persist into the second year of CAM reporting. Our evidence is consistent with tax CAM disclosures having a modest but short-lived effect on companies' reporting of tax accounts. Our findings should inform the PCAOB as they conduct their post-implementation review of the new audit reporting standard.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"41 2","pages":"719-747"},"PeriodicalIF":3.8000,"publicationDate":"2023-11-20","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12920","citationCount":"0","resultStr":"{\"title\":\"Disclosure of tax-related critical audit matters and tax-related outcomes\",\"authors\":\"Katharine D. Drake, Nathan C. Goldman, Stephen J. Lusch, Jaime J. Schmidt\",\"doi\":\"10.1111/1911-3846.12920\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Given that tax-related critical audit matters (tax CAMs) were prevalent among accelerated filers (18.5% of observations) during the initial year of CAM disclosures, we examine whether an auditor's disclosure of tax CAMs is associated with variation in tax-related financial reporting quality, tax avoidance, and tax-related earnings management. Finding an association between tax CAMs and one of these tax outcomes would indicate that the new auditor reporting standard has indirectly affected investors. Examining the first year of CAM disclosures, we do not find that tax CAMs are associated with broad proxies of tax-related audit or financial reporting quality (e.g., restatements, internal control weaknesses, comment letters) or tax avoidance (e.g., effective tax rates or book-to-tax differences). We do find that tax CAMs are associated with a modest increase in tax accrual quality, an increase in the reserve for unrecognized tax benefits, and a reduction in the likelihood of tax-related earnings management. However, we do not find these tax CAM effects persist into the second year of CAM reporting. Our evidence is consistent with tax CAM disclosures having a modest but short-lived effect on companies' reporting of tax accounts. Our findings should inform the PCAOB as they conduct their post-implementation review of the new audit reporting standard.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"41 2\",\"pages\":\"719-747\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2023-11-20\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12920\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12920\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12920","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Disclosure of tax-related critical audit matters and tax-related outcomes

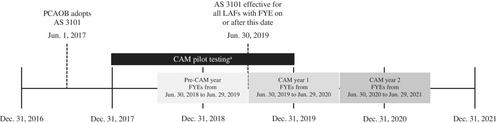

Given that tax-related critical audit matters (tax CAMs) were prevalent among accelerated filers (18.5% of observations) during the initial year of CAM disclosures, we examine whether an auditor's disclosure of tax CAMs is associated with variation in tax-related financial reporting quality, tax avoidance, and tax-related earnings management. Finding an association between tax CAMs and one of these tax outcomes would indicate that the new auditor reporting standard has indirectly affected investors. Examining the first year of CAM disclosures, we do not find that tax CAMs are associated with broad proxies of tax-related audit or financial reporting quality (e.g., restatements, internal control weaknesses, comment letters) or tax avoidance (e.g., effective tax rates or book-to-tax differences). We do find that tax CAMs are associated with a modest increase in tax accrual quality, an increase in the reserve for unrecognized tax benefits, and a reduction in the likelihood of tax-related earnings management. However, we do not find these tax CAM effects persist into the second year of CAM reporting. Our evidence is consistent with tax CAM disclosures having a modest but short-lived effect on companies' reporting of tax accounts. Our findings should inform the PCAOB as they conduct their post-implementation review of the new audit reporting standard.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们