Zachary King, Thomas J. Linsmeier, Daniel D. Wangerin

{"title":"可辨认无形资产的价值相关性差异","authors":"Zachary King, Thomas J. Linsmeier, Daniel D. Wangerin","doi":"10.1007/s11142-023-09810-8","DOIUrl":null,"url":null,"abstract":"<p>Motivated by investor criticisms of current accounting standards, this study investigates whether differences exist in how acquired identifiable intangible assets relate to investors’ expectations about the entity’s cash flow prospects. Some investors assert that all acquired intangibles should be subsumed within goodwill, while others prefer separate recognition of identifiable intangibles only when they are strategically important sources of future cash flows. Still other investors call for separate recognition from goodwill only when identifiable intangibles are separable from the business, have defined useful lives, and have identifiable revenue streams (i.e., “wasting” intangibles). Consistent with some investor views, we find cross-sectional variation in the value relevance of identifiable intangibles based on differences in underlying asset characteristics. Our primary findings suggest that strategically important and wasting intangibles provide information different from that provided by goodwill. These findings inform standard setters as they evaluate recognition and disclosure alternatives for identifiable intangible assets.</p>","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"19 1","pages":""},"PeriodicalIF":5.8000,"publicationDate":"2023-11-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Differences in the value relevance of identifiable intangible assets\",\"authors\":\"Zachary King, Thomas J. Linsmeier, Daniel D. Wangerin\",\"doi\":\"10.1007/s11142-023-09810-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Motivated by investor criticisms of current accounting standards, this study investigates whether differences exist in how acquired identifiable intangible assets relate to investors’ expectations about the entity’s cash flow prospects. Some investors assert that all acquired intangibles should be subsumed within goodwill, while others prefer separate recognition of identifiable intangibles only when they are strategically important sources of future cash flows. Still other investors call for separate recognition from goodwill only when identifiable intangibles are separable from the business, have defined useful lives, and have identifiable revenue streams (i.e., “wasting” intangibles). Consistent with some investor views, we find cross-sectional variation in the value relevance of identifiable intangibles based on differences in underlying asset characteristics. Our primary findings suggest that strategically important and wasting intangibles provide information different from that provided by goodwill. These findings inform standard setters as they evaluate recognition and disclosure alternatives for identifiable intangible assets.</p>\",\"PeriodicalId\":48120,\"journal\":{\"name\":\"Review of Accounting Studies\",\"volume\":\"19 1\",\"pages\":\"\"},\"PeriodicalIF\":5.8000,\"publicationDate\":\"2023-11-23\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Accounting Studies\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://doi.org/10.1007/s11142-023-09810-8\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s11142-023-09810-8","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Differences in the value relevance of identifiable intangible assets

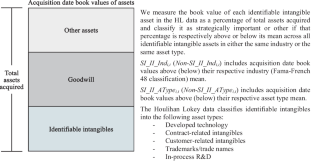

Motivated by investor criticisms of current accounting standards, this study investigates whether differences exist in how acquired identifiable intangible assets relate to investors’ expectations about the entity’s cash flow prospects. Some investors assert that all acquired intangibles should be subsumed within goodwill, while others prefer separate recognition of identifiable intangibles only when they are strategically important sources of future cash flows. Still other investors call for separate recognition from goodwill only when identifiable intangibles are separable from the business, have defined useful lives, and have identifiable revenue streams (i.e., “wasting” intangibles). Consistent with some investor views, we find cross-sectional variation in the value relevance of identifiable intangibles based on differences in underlying asset characteristics. Our primary findings suggest that strategically important and wasting intangibles provide information different from that provided by goodwill. These findings inform standard setters as they evaluate recognition and disclosure alternatives for identifiable intangible assets.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们