Julia Braun, Hans-Peter Burghof, Julius Langer, Dag Einar Sommervoll

{"title":"房价波动:不同类型的金融中介对房地产市场周期的影响是否不同?","authors":"Julia Braun, Hans-Peter Burghof, Julius Langer, Dag Einar Sommervoll","doi":"10.1007/s11146-022-09907-y","DOIUrl":null,"url":null,"abstract":"<p>Housing markets display several correlations to multiple economic sectors of an economy. Their enormous impact on economies’ health, wealth, and stability is uncontroversial. Interestingly, the forms of financing residential property vary widely between the different countries in terms of both, the available product types and the institutions offering them. This research examines the implications of different financial intermediaries on housing market cycles with special emphasis on two institutional types, conventional banks and building and loan associations. Introducing a heterogeneous agent-based model, the interactions of buyers, sellers, and the two types of credit institutions are assessed. Heterogeneous economic principles and expectations of agents create endogenous market conditions which are strongly influenced by the lending practices of financial intermediaries.</p><p>Focusing primarily on collateral values to decide about lending, conventional banks may contribute to volatile housing markets which are prone to recessions. Building and loan associations, on the other hand, rely to a greater extent on endogenously created borrower information. Thus, they are able to cushion the volatility of house prices caused by procyclical mortgage lending of conventional banks and increase the stability of the housing market. Simulations show that the most stable market conditions are attained if both types of financial intermediaries serve the mortgage lending market jointly. Furthermore, transaction and homeownership rates are the highest in this market setting. These findings advocate in favor of diversified financial markets.</p>","PeriodicalId":22891,"journal":{"name":"The Journal of Real Estate Finance and Economics","volume":"21 1","pages":""},"PeriodicalIF":0.0000,"publicationDate":"2022-06-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"The Volatility of Housing Prices: Do Different Types of Financial Intermediaries Affect Housing Market Cycles Differently?\",\"authors\":\"Julia Braun, Hans-Peter Burghof, Julius Langer, Dag Einar Sommervoll\",\"doi\":\"10.1007/s11146-022-09907-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Housing markets display several correlations to multiple economic sectors of an economy. Their enormous impact on economies’ health, wealth, and stability is uncontroversial. Interestingly, the forms of financing residential property vary widely between the different countries in terms of both, the available product types and the institutions offering them. This research examines the implications of different financial intermediaries on housing market cycles with special emphasis on two institutional types, conventional banks and building and loan associations. Introducing a heterogeneous agent-based model, the interactions of buyers, sellers, and the two types of credit institutions are assessed. Heterogeneous economic principles and expectations of agents create endogenous market conditions which are strongly influenced by the lending practices of financial intermediaries.</p><p>Focusing primarily on collateral values to decide about lending, conventional banks may contribute to volatile housing markets which are prone to recessions. Building and loan associations, on the other hand, rely to a greater extent on endogenously created borrower information. Thus, they are able to cushion the volatility of house prices caused by procyclical mortgage lending of conventional banks and increase the stability of the housing market. Simulations show that the most stable market conditions are attained if both types of financial intermediaries serve the mortgage lending market jointly. Furthermore, transaction and homeownership rates are the highest in this market setting. These findings advocate in favor of diversified financial markets.</p>\",\"PeriodicalId\":22891,\"journal\":{\"name\":\"The Journal of Real Estate Finance and Economics\",\"volume\":\"21 1\",\"pages\":\"\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2022-06-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"The Journal of Real Estate Finance and Economics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11146-022-09907-y\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"The Journal of Real Estate Finance and Economics","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11146-022-09907-y","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

The Volatility of Housing Prices: Do Different Types of Financial Intermediaries Affect Housing Market Cycles Differently?

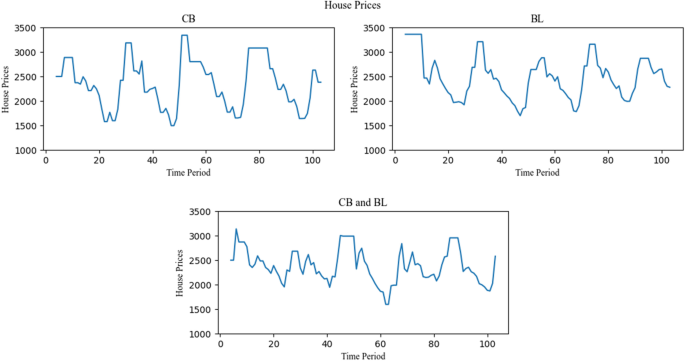

Housing markets display several correlations to multiple economic sectors of an economy. Their enormous impact on economies’ health, wealth, and stability is uncontroversial. Interestingly, the forms of financing residential property vary widely between the different countries in terms of both, the available product types and the institutions offering them. This research examines the implications of different financial intermediaries on housing market cycles with special emphasis on two institutional types, conventional banks and building and loan associations. Introducing a heterogeneous agent-based model, the interactions of buyers, sellers, and the two types of credit institutions are assessed. Heterogeneous economic principles and expectations of agents create endogenous market conditions which are strongly influenced by the lending practices of financial intermediaries.

Focusing primarily on collateral values to decide about lending, conventional banks may contribute to volatile housing markets which are prone to recessions. Building and loan associations, on the other hand, rely to a greater extent on endogenously created borrower information. Thus, they are able to cushion the volatility of house prices caused by procyclical mortgage lending of conventional banks and increase the stability of the housing market. Simulations show that the most stable market conditions are attained if both types of financial intermediaries serve the mortgage lending market jointly. Furthermore, transaction and homeownership rates are the highest in this market setting. These findings advocate in favor of diversified financial markets.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们