{"title":"鼓励利用数字税收工具应对 Covid:来自埃斯瓦提尼的证据","authors":"Fabrizio Santoro, Razan Amine, Tanele Magongo","doi":"10.1007/s10797-023-09810-z","DOIUrl":null,"url":null,"abstract":"<p>Many tax authorities changed the mode of interacting with taxpayers from physical to online as a response to the Covid-19 pandemic. We study the effect of the e-tax-filing in Eswatini, using a difference-in-difference and propensity score methods that exploit the limited take-up of e-tax filing. We present three sets of results. First, larger and more IT-sophisticated firms are more likely to adopt e-Tax. Second, after adoption, e-Tax has mixed results on filing behavior and reporting accuracy. Third, companies remit less tax after adoption e-tax-filing.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"100 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2023-12-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Encouraging digital tax tools as a response to Covid: evidence from Eswatini\",\"authors\":\"Fabrizio Santoro, Razan Amine, Tanele Magongo\",\"doi\":\"10.1007/s10797-023-09810-z\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Many tax authorities changed the mode of interacting with taxpayers from physical to online as a response to the Covid-19 pandemic. We study the effect of the e-tax-filing in Eswatini, using a difference-in-difference and propensity score methods that exploit the limited take-up of e-tax filing. We present three sets of results. First, larger and more IT-sophisticated firms are more likely to adopt e-Tax. Second, after adoption, e-Tax has mixed results on filing behavior and reporting accuracy. Third, companies remit less tax after adoption e-tax-filing.</p>\",\"PeriodicalId\":47518,\"journal\":{\"name\":\"International Tax and Public Finance\",\"volume\":\"100 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2023-12-15\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Tax and Public Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10797-023-09810-z\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-023-09810-z","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Encouraging digital tax tools as a response to Covid: evidence from Eswatini

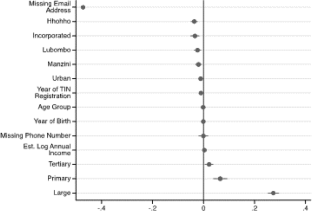

Many tax authorities changed the mode of interacting with taxpayers from physical to online as a response to the Covid-19 pandemic. We study the effect of the e-tax-filing in Eswatini, using a difference-in-difference and propensity score methods that exploit the limited take-up of e-tax filing. We present three sets of results. First, larger and more IT-sophisticated firms are more likely to adopt e-Tax. Second, after adoption, e-Tax has mixed results on filing behavior and reporting accuracy. Third, companies remit less tax after adoption e-tax-filing.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们