{"title":"优化在美外国直接投资税收的混合实体结构","authors":"Thomas Kollruss","doi":"10.1002/jcaf.22675","DOIUrl":null,"url":null,"abstract":"<p>This article develops a new strategy for the (tax) optimization of foreign direct investments in the U.S. This strategy is particularly favorable for natural persons. By using a foreign upstream hybrid partnership, a substantial tax optimization of the current taxation of profits as well as the taxation of capital gains can be achieved. In addition, current and final losses may also be offset cross-border to a certain extent in the case of an exemption under treaty law. This tax structuring idea is presented by way of example and explained on the basis of the country constellation U.S./Germany.</p>","PeriodicalId":44561,"journal":{"name":"Journal of Corporate Accounting and Finance","volume":"35 2","pages":"147-156"},"PeriodicalIF":1.3000,"publicationDate":"2023-11-27","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jcaf.22675","citationCount":"0","resultStr":"{\"title\":\"A hybrid entity structure for tax optimization of foreign direct investment in the U.S.\",\"authors\":\"Thomas Kollruss\",\"doi\":\"10.1002/jcaf.22675\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This article develops a new strategy for the (tax) optimization of foreign direct investments in the U.S. This strategy is particularly favorable for natural persons. By using a foreign upstream hybrid partnership, a substantial tax optimization of the current taxation of profits as well as the taxation of capital gains can be achieved. In addition, current and final losses may also be offset cross-border to a certain extent in the case of an exemption under treaty law. This tax structuring idea is presented by way of example and explained on the basis of the country constellation U.S./Germany.</p>\",\"PeriodicalId\":44561,\"journal\":{\"name\":\"Journal of Corporate Accounting and Finance\",\"volume\":\"35 2\",\"pages\":\"147-156\"},\"PeriodicalIF\":1.3000,\"publicationDate\":\"2023-11-27\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jcaf.22675\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Corporate Accounting and Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/jcaf.22675\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Corporate Accounting and Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jcaf.22675","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

A hybrid entity structure for tax optimization of foreign direct investment in the U.S.

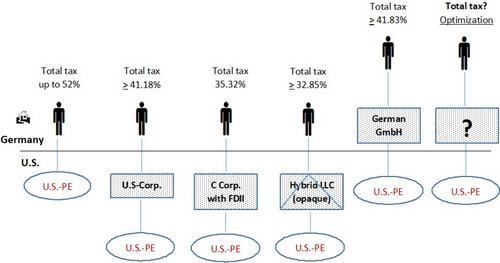

This article develops a new strategy for the (tax) optimization of foreign direct investments in the U.S. This strategy is particularly favorable for natural persons. By using a foreign upstream hybrid partnership, a substantial tax optimization of the current taxation of profits as well as the taxation of capital gains can be achieved. In addition, current and final losses may also be offset cross-border to a certain extent in the case of an exemption under treaty law. This tax structuring idea is presented by way of example and explained on the basis of the country constellation U.S./Germany.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们