{"title":"气候风险与商业抵押贷款拖欠","authors":"Rogier Holtermans, Matthew E. Kahn, Nils Kok","doi":"10.1111/jors.12681","DOIUrl":null,"url":null,"abstract":"<p>Natural disasters such as hurricanes, floods, heatwaves, and wildfires are projected to become more prevalent in the foreseeable future. Climate risk is, therefore, increasingly recognized as an important factor by policy makers, the investment community, and financial markets. Due to the immobility of assets, the commercial real estate industry is especially vulnerable to climate risk, and there is an increasing interest to understand the impact of climate risk on the value of commercial real estate. For commercial real estate lenders, changes in collateral value are only of partial importance. The ability of borrowers to meet their payment obligations is equally, if not more important. By combining historical data on two major climate-related disasters—Hurricanes Harvey and Sandy—with longitudinal information on commercial mortgage performance, this paper identifies the impact of climate risks on mortgage delinquency rates for commercial real estate mortgages. The results show that both Harvey and Sandy led to elevated levels of commercial mortgage delinquency, with significant heterogeneity based on the extent of damage in the Census block group. Information provided through FEMA 100-year floodplain maps partially mitigates the effects, an indication that lenders incorporate flood risk information in the underwriting process. An analysis of potential mechanisms indicates a decrease in property income during the 2-year period following the event for Hurricane Harvey, but no evidence of income effects for Sandy.</p>","PeriodicalId":48059,"journal":{"name":"Journal of Regional Science","volume":"64 4","pages":"994-1037"},"PeriodicalIF":2.7000,"publicationDate":"2024-01-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jors.12681","citationCount":"0","resultStr":"{\"title\":\"Climate risk and commercial mortgage delinquency\",\"authors\":\"Rogier Holtermans, Matthew E. Kahn, Nils Kok\",\"doi\":\"10.1111/jors.12681\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Natural disasters such as hurricanes, floods, heatwaves, and wildfires are projected to become more prevalent in the foreseeable future. Climate risk is, therefore, increasingly recognized as an important factor by policy makers, the investment community, and financial markets. Due to the immobility of assets, the commercial real estate industry is especially vulnerable to climate risk, and there is an increasing interest to understand the impact of climate risk on the value of commercial real estate. For commercial real estate lenders, changes in collateral value are only of partial importance. The ability of borrowers to meet their payment obligations is equally, if not more important. By combining historical data on two major climate-related disasters—Hurricanes Harvey and Sandy—with longitudinal information on commercial mortgage performance, this paper identifies the impact of climate risks on mortgage delinquency rates for commercial real estate mortgages. The results show that both Harvey and Sandy led to elevated levels of commercial mortgage delinquency, with significant heterogeneity based on the extent of damage in the Census block group. Information provided through FEMA 100-year floodplain maps partially mitigates the effects, an indication that lenders incorporate flood risk information in the underwriting process. An analysis of potential mechanisms indicates a decrease in property income during the 2-year period following the event for Hurricane Harvey, but no evidence of income effects for Sandy.</p>\",\"PeriodicalId\":48059,\"journal\":{\"name\":\"Journal of Regional Science\",\"volume\":\"64 4\",\"pages\":\"994-1037\"},\"PeriodicalIF\":2.7000,\"publicationDate\":\"2024-01-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jors.12681\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Regional Science\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jors.12681\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Regional Science","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jors.12681","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

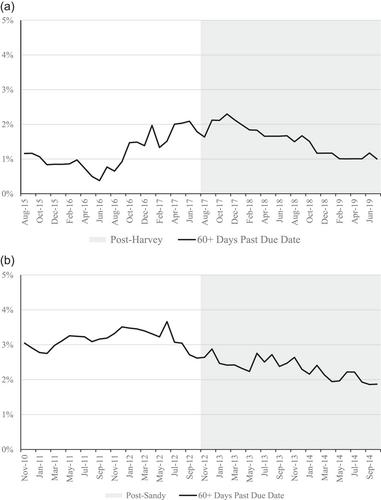

Natural disasters such as hurricanes, floods, heatwaves, and wildfires are projected to become more prevalent in the foreseeable future. Climate risk is, therefore, increasingly recognized as an important factor by policy makers, the investment community, and financial markets. Due to the immobility of assets, the commercial real estate industry is especially vulnerable to climate risk, and there is an increasing interest to understand the impact of climate risk on the value of commercial real estate. For commercial real estate lenders, changes in collateral value are only of partial importance. The ability of borrowers to meet their payment obligations is equally, if not more important. By combining historical data on two major climate-related disasters—Hurricanes Harvey and Sandy—with longitudinal information on commercial mortgage performance, this paper identifies the impact of climate risks on mortgage delinquency rates for commercial real estate mortgages. The results show that both Harvey and Sandy led to elevated levels of commercial mortgage delinquency, with significant heterogeneity based on the extent of damage in the Census block group. Information provided through FEMA 100-year floodplain maps partially mitigates the effects, an indication that lenders incorporate flood risk information in the underwriting process. An analysis of potential mechanisms indicates a decrease in property income during the 2-year period following the event for Hurricane Harvey, but no evidence of income effects for Sandy.

期刊介绍:

The Journal of Regional Science (JRS) publishes original analytical research at the intersection of economics and quantitative geography. Since 1958, the JRS has published leading contributions to urban and regional thought including rigorous methodological contributions and seminal theoretical pieces. The JRS is one of the most highly cited journals in urban and regional research, planning, geography, and the environment. The JRS publishes work that advances our understanding of the geographic dimensions of urban and regional economies, human settlements, and policies related to cities and regions.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们