{"title":"审计公司任期披露与非专业投资者对审计师独立性的看法:合伙人轮换披露的缓解效应","authors":"Sarah Judge, Brian M. Goodson, Chad M. Stefaniak","doi":"10.1111/1911-3846.12936","DOIUrl":null,"url":null,"abstract":"<p>In 2017, the PCAOB began requiring audit firm tenure disclosure within the audit report for SEC registrant clients. Many commenters raised the concern that prominent disclosure of firm tenure would lead investors to inappropriately infer a negative relation between audit quality and long tenure. This is particularly troubling given that empirical evidence generally does not support this concern. In our first experiment, we predict and find that disclosing an audit firm's long tenure within the audit report increases investors' perceptions that the audit firm's independence was impaired while conducting the audit. However, we also identify an intervention that mitigates the effects of disclosing long tenure—an accompanying disclosure in the audit report of the firm's adherence to the SEC's mandatory partner rotation requirement. We find that such a disclosure moderates the effect of long tenure disclosure such that in the absence (presence) of a partner rotation disclosure, investors do (do not) perceive increased independence impairment when long firm tenure is disclosed. In a second experiment, we predict and find that long firm tenure disclosure reduces investors' preference to invest in an otherwise quantitatively optimal investment and that this relation is driven, in part, by perceptions of independence impairment. Again, this result is attenuated by partner rotation disclosure. Our results should be useful to regulators in understanding the effects of their disclosure mandate and to audit firms in understanding a practical way in which they might mitigate the implications of such effects.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"41 2","pages":"1284-1310"},"PeriodicalIF":3.8000,"publicationDate":"2024-01-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12936","citationCount":"0","resultStr":"{\"title\":\"Audit firm tenure disclosure and nonprofessional investors' perceptions of auditor independence: The mitigating effect of partner rotation disclosure\",\"authors\":\"Sarah Judge, Brian M. Goodson, Chad M. Stefaniak\",\"doi\":\"10.1111/1911-3846.12936\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In 2017, the PCAOB began requiring audit firm tenure disclosure within the audit report for SEC registrant clients. Many commenters raised the concern that prominent disclosure of firm tenure would lead investors to inappropriately infer a negative relation between audit quality and long tenure. This is particularly troubling given that empirical evidence generally does not support this concern. In our first experiment, we predict and find that disclosing an audit firm's long tenure within the audit report increases investors' perceptions that the audit firm's independence was impaired while conducting the audit. However, we also identify an intervention that mitigates the effects of disclosing long tenure—an accompanying disclosure in the audit report of the firm's adherence to the SEC's mandatory partner rotation requirement. We find that such a disclosure moderates the effect of long tenure disclosure such that in the absence (presence) of a partner rotation disclosure, investors do (do not) perceive increased independence impairment when long firm tenure is disclosed. In a second experiment, we predict and find that long firm tenure disclosure reduces investors' preference to invest in an otherwise quantitatively optimal investment and that this relation is driven, in part, by perceptions of independence impairment. Again, this result is attenuated by partner rotation disclosure. Our results should be useful to regulators in understanding the effects of their disclosure mandate and to audit firms in understanding a practical way in which they might mitigate the implications of such effects.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"41 2\",\"pages\":\"1284-1310\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2024-01-24\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12936\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12936\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12936","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Audit firm tenure disclosure and nonprofessional investors' perceptions of auditor independence: The mitigating effect of partner rotation disclosure

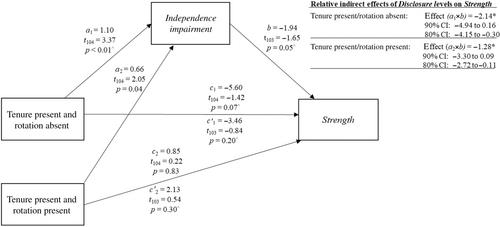

In 2017, the PCAOB began requiring audit firm tenure disclosure within the audit report for SEC registrant clients. Many commenters raised the concern that prominent disclosure of firm tenure would lead investors to inappropriately infer a negative relation between audit quality and long tenure. This is particularly troubling given that empirical evidence generally does not support this concern. In our first experiment, we predict and find that disclosing an audit firm's long tenure within the audit report increases investors' perceptions that the audit firm's independence was impaired while conducting the audit. However, we also identify an intervention that mitigates the effects of disclosing long tenure—an accompanying disclosure in the audit report of the firm's adherence to the SEC's mandatory partner rotation requirement. We find that such a disclosure moderates the effect of long tenure disclosure such that in the absence (presence) of a partner rotation disclosure, investors do (do not) perceive increased independence impairment when long firm tenure is disclosed. In a second experiment, we predict and find that long firm tenure disclosure reduces investors' preference to invest in an otherwise quantitatively optimal investment and that this relation is driven, in part, by perceptions of independence impairment. Again, this result is attenuated by partner rotation disclosure. Our results should be useful to regulators in understanding the effects of their disclosure mandate and to audit firms in understanding a practical way in which they might mitigate the implications of such effects.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们