{"title":"管理层的意外预测与未来股票回报","authors":"Norio Kitagawa, Akinobu Shuto","doi":"10.1111/jbfa.12785","DOIUrl":null,"url":null,"abstract":"<p>This study investigates the effect of managerial discretion regarding initial earnings forecasts on future stock returns for Japanese firms. We estimate the unexpected portion of initial management earnings forecasts (“unexpected forecasts”) based on the findings of fundamental analysis research and define it as a proxy for forecast management. Using this measure, we find that firms with higher unexpected forecasts are related to negative abnormal returns over the subsequent 12 months. By contrast, the expected portion of earnings forecasts is not related to future abnormal returns. These results suggest that the market tends to appropriately price the credible portion of management forecasts, while overpricing the less credible portion. Further analysis reveals that the relationship between unexpected forecasts and future returns is (1) distinct from accruals anomaly, notably (2) in the 6-month return window, (3) in the first half of the sample period (especially in 2005 and 2006), (4) in extreme unexpected forecast news and (5) in a poor information environment. This study extends the literature by focusing on a more desirable research setting in Japan, compared to other studies, to explore management forecasts and present new implications for the market pricing of management earnings forecasts.</p>","PeriodicalId":48106,"journal":{"name":"Journal of Business Finance & Accounting","volume":"51 9-10","pages":"2452-2489"},"PeriodicalIF":2.4000,"publicationDate":"2024-01-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12785","citationCount":"0","resultStr":"{\"title\":\"Unexpected management forecasts and future stock returns\",\"authors\":\"Norio Kitagawa, Akinobu Shuto\",\"doi\":\"10.1111/jbfa.12785\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study investigates the effect of managerial discretion regarding initial earnings forecasts on future stock returns for Japanese firms. We estimate the unexpected portion of initial management earnings forecasts (“unexpected forecasts”) based on the findings of fundamental analysis research and define it as a proxy for forecast management. Using this measure, we find that firms with higher unexpected forecasts are related to negative abnormal returns over the subsequent 12 months. By contrast, the expected portion of earnings forecasts is not related to future abnormal returns. These results suggest that the market tends to appropriately price the credible portion of management forecasts, while overpricing the less credible portion. Further analysis reveals that the relationship between unexpected forecasts and future returns is (1) distinct from accruals anomaly, notably (2) in the 6-month return window, (3) in the first half of the sample period (especially in 2005 and 2006), (4) in extreme unexpected forecast news and (5) in a poor information environment. This study extends the literature by focusing on a more desirable research setting in Japan, compared to other studies, to explore management forecasts and present new implications for the market pricing of management earnings forecasts.</p>\",\"PeriodicalId\":48106,\"journal\":{\"name\":\"Journal of Business Finance & Accounting\",\"volume\":\"51 9-10\",\"pages\":\"2452-2489\"},\"PeriodicalIF\":2.4000,\"publicationDate\":\"2024-01-31\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12785\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Business Finance & Accounting\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12785\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Business Finance & Accounting","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12785","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Unexpected management forecasts and future stock returns

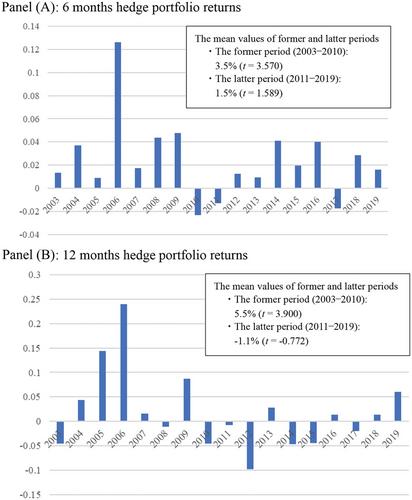

This study investigates the effect of managerial discretion regarding initial earnings forecasts on future stock returns for Japanese firms. We estimate the unexpected portion of initial management earnings forecasts (“unexpected forecasts”) based on the findings of fundamental analysis research and define it as a proxy for forecast management. Using this measure, we find that firms with higher unexpected forecasts are related to negative abnormal returns over the subsequent 12 months. By contrast, the expected portion of earnings forecasts is not related to future abnormal returns. These results suggest that the market tends to appropriately price the credible portion of management forecasts, while overpricing the less credible portion. Further analysis reveals that the relationship between unexpected forecasts and future returns is (1) distinct from accruals anomaly, notably (2) in the 6-month return window, (3) in the first half of the sample period (especially in 2005 and 2006), (4) in extreme unexpected forecast news and (5) in a poor information environment. This study extends the literature by focusing on a more desirable research setting in Japan, compared to other studies, to explore management forecasts and present new implications for the market pricing of management earnings forecasts.

期刊介绍:

Journal of Business Finance and Accounting exists to publish high quality research papers in accounting, corporate finance, corporate governance and their interfaces. The interfaces are relevant in many areas such as financial reporting and communication, valuation, financial performance measurement and managerial reward and control structures. A feature of JBFA is that it recognises that informational problems are pervasive in financial markets and business organisations, and that accounting plays an important role in resolving such problems. JBFA welcomes both theoretical and empirical contributions. Nonetheless, theoretical papers should yield novel testable implications, and empirical papers should be theoretically well-motivated. The Editors view accounting and finance as being closely related to economics and, as a consequence, papers submitted will often have theoretical motivations that are grounded in economics. JBFA, however, also seeks papers that complement economics-based theorising with theoretical developments originating in other social science disciplines or traditions. While many papers in JBFA use econometric or related empirical methods, the Editors also welcome contributions that use other empirical research methods. Although the scope of JBFA is broad, it is not a suitable outlet for highly abstract mathematical papers, or empirical papers with inadequate theoretical motivation. Also, papers that study asset pricing, or the operations of financial markets, should have direct implications for one or more of preparers, regulators, users of financial statements, and corporate financial decision makers, or at least should have implications for the development of future research relevant to such users.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们