Burak Alparslan Eroğlu, Deniz İkizlerli, Numan Ülkü

{"title":"应用混合频率 VAR 研究外国投资者交易和股市回报的共同动态性","authors":"Burak Alparslan Eroğlu, Deniz İkizlerli, Numan Ülkü","doi":"10.1007/s00181-023-02541-4","DOIUrl":null,"url":null,"abstract":"<p>We present the first application of the mixed-frequency VAR (MF-VAR) method in the market microstructure literature, studying the interaction between stock market returns and foreign investors’ trading. MF-VAR allows us to use daily investor trading data together with higher-frequency return series and uncover novel intraday patterns in the feedback trading behavior and the information content of trading. Using data from Korea, we find that foreign investors chase opening-hour returns, and their trading has the ability to forecast subsequent days' late-hour returns. This pattern suggests that foreign investors selectively respond to the information incorporated during opening hours. Over the years, foreign investors' response to intraday returns has become more prompt, and the predictive ability of their trading has disappeared. A specific test made feasible by the MF-VAR method does not support the global private information hypothesis.</p>","PeriodicalId":11642,"journal":{"name":"Empirical Economics","volume":"17 1","pages":""},"PeriodicalIF":1.9000,"publicationDate":"2024-02-20","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"A mixed-frequency VAR application to studying joint dynamics of foreign investor trading and stock market returns\",\"authors\":\"Burak Alparslan Eroğlu, Deniz İkizlerli, Numan Ülkü\",\"doi\":\"10.1007/s00181-023-02541-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We present the first application of the mixed-frequency VAR (MF-VAR) method in the market microstructure literature, studying the interaction between stock market returns and foreign investors’ trading. MF-VAR allows us to use daily investor trading data together with higher-frequency return series and uncover novel intraday patterns in the feedback trading behavior and the information content of trading. Using data from Korea, we find that foreign investors chase opening-hour returns, and their trading has the ability to forecast subsequent days' late-hour returns. This pattern suggests that foreign investors selectively respond to the information incorporated during opening hours. Over the years, foreign investors' response to intraday returns has become more prompt, and the predictive ability of their trading has disappeared. A specific test made feasible by the MF-VAR method does not support the global private information hypothesis.</p>\",\"PeriodicalId\":11642,\"journal\":{\"name\":\"Empirical Economics\",\"volume\":\"17 1\",\"pages\":\"\"},\"PeriodicalIF\":1.9000,\"publicationDate\":\"2024-02-20\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Empirical Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s00181-023-02541-4\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Empirical Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00181-023-02541-4","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

A mixed-frequency VAR application to studying joint dynamics of foreign investor trading and stock market returns

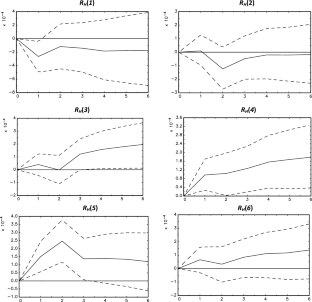

We present the first application of the mixed-frequency VAR (MF-VAR) method in the market microstructure literature, studying the interaction between stock market returns and foreign investors’ trading. MF-VAR allows us to use daily investor trading data together with higher-frequency return series and uncover novel intraday patterns in the feedback trading behavior and the information content of trading. Using data from Korea, we find that foreign investors chase opening-hour returns, and their trading has the ability to forecast subsequent days' late-hour returns. This pattern suggests that foreign investors selectively respond to the information incorporated during opening hours. Over the years, foreign investors' response to intraday returns has become more prompt, and the predictive ability of their trading has disappeared. A specific test made feasible by the MF-VAR method does not support the global private information hypothesis.

期刊介绍:

Empirical Economics publishes high quality papers using econometric or statistical methods to fill the gap between economic theory and observed data. Papers explore such topics as estimation of established relationships between economic variables, testing of hypotheses derived from economic theory, treatment effect estimation, policy evaluation, simulation, forecasting, as well as econometric methods and measurement. Empirical Economics emphasizes the replicability of empirical results. Replication studies of important results in the literature - both positive and negative results - may be published as short papers in Empirical Economics. Authors of all accepted papers and replications are required to submit all data and codes prior to publication (for more details, see: Instructions for Authors).The journal follows a single blind review procedure. In order to ensure the high quality of the journal and an efficient editorial process, a substantial number of submissions that have very poor chances of receiving positive reviews are routinely rejected without sending the papers for review.Officially cited as: Empir Econ

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们