{"title":"三方程模型中的倒收益曲线","authors":"Leila Davis, Thomas R. Michl","doi":"10.1057/s41302-024-00264-7","DOIUrl":null,"url":null,"abstract":"<p>The power of an inverted yield curve to predict recessions is widely discussed in the financial press, yet most undergraduate textbooks provide little discussion of this stylized fact. This paper fills this gap by extending a 3-equation textbook model to include an accessible treatment of a term structure of interest rates formed by the one-period policy rate and a two-period rate that obeys the Fisher Equation. The Phillips curve features partially anchored adaptive expectations, while financial markets and the central bank have perfect foresight. Using this framework, we show that raising the policy rate in response to an inflation shock inverts the yield curve. Whether this inversion foreshadows a recession, however, depends on the bank’s monetary policy rule, which we illustrate using numerical examples. In particular, we show that, with anchoring and an output-gap averse central bank, inflation can stabilize and the yield curve can invert without an ensuing recession.</p>","PeriodicalId":45363,"journal":{"name":"Eastern Economic Journal","volume":"50 1","pages":""},"PeriodicalIF":0.5000,"publicationDate":"2024-02-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"The Inverted Yield Curve in a 3-Equation Model\",\"authors\":\"Leila Davis, Thomas R. Michl\",\"doi\":\"10.1057/s41302-024-00264-7\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The power of an inverted yield curve to predict recessions is widely discussed in the financial press, yet most undergraduate textbooks provide little discussion of this stylized fact. This paper fills this gap by extending a 3-equation textbook model to include an accessible treatment of a term structure of interest rates formed by the one-period policy rate and a two-period rate that obeys the Fisher Equation. The Phillips curve features partially anchored adaptive expectations, while financial markets and the central bank have perfect foresight. Using this framework, we show that raising the policy rate in response to an inflation shock inverts the yield curve. Whether this inversion foreshadows a recession, however, depends on the bank’s monetary policy rule, which we illustrate using numerical examples. In particular, we show that, with anchoring and an output-gap averse central bank, inflation can stabilize and the yield curve can invert without an ensuing recession.</p>\",\"PeriodicalId\":45363,\"journal\":{\"name\":\"Eastern Economic Journal\",\"volume\":\"50 1\",\"pages\":\"\"},\"PeriodicalIF\":0.5000,\"publicationDate\":\"2024-02-24\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Eastern Economic Journal\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41302-024-00264-7\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Eastern Economic Journal","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41302-024-00264-7","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

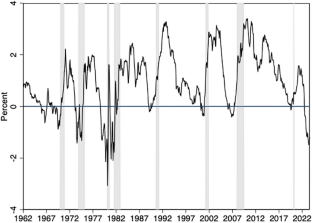

The power of an inverted yield curve to predict recessions is widely discussed in the financial press, yet most undergraduate textbooks provide little discussion of this stylized fact. This paper fills this gap by extending a 3-equation textbook model to include an accessible treatment of a term structure of interest rates formed by the one-period policy rate and a two-period rate that obeys the Fisher Equation. The Phillips curve features partially anchored adaptive expectations, while financial markets and the central bank have perfect foresight. Using this framework, we show that raising the policy rate in response to an inflation shock inverts the yield curve. Whether this inversion foreshadows a recession, however, depends on the bank’s monetary policy rule, which we illustrate using numerical examples. In particular, we show that, with anchoring and an output-gap averse central bank, inflation can stabilize and the yield curve can invert without an ensuing recession.

期刊介绍:

The Eastern Economic Journal, a quarterly publication of the Eastern Economic Association, was established in 1973. The EEJ publishes papers written from every perspective, in all areas of economics and is committed to free and open intellectual inquiry from diverse philosophical perspectives. It welcomes manuscripts that are methodological and philosophical as well as empirical and theoretical. Readability and general interest are major factors in publication decision.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们